3 Wiener processes

Here we review stochastic process that are useful in finance, especially in the Black-Scholes context. This section is based on Hull (2015), chapter 14.

3.1 The basic process

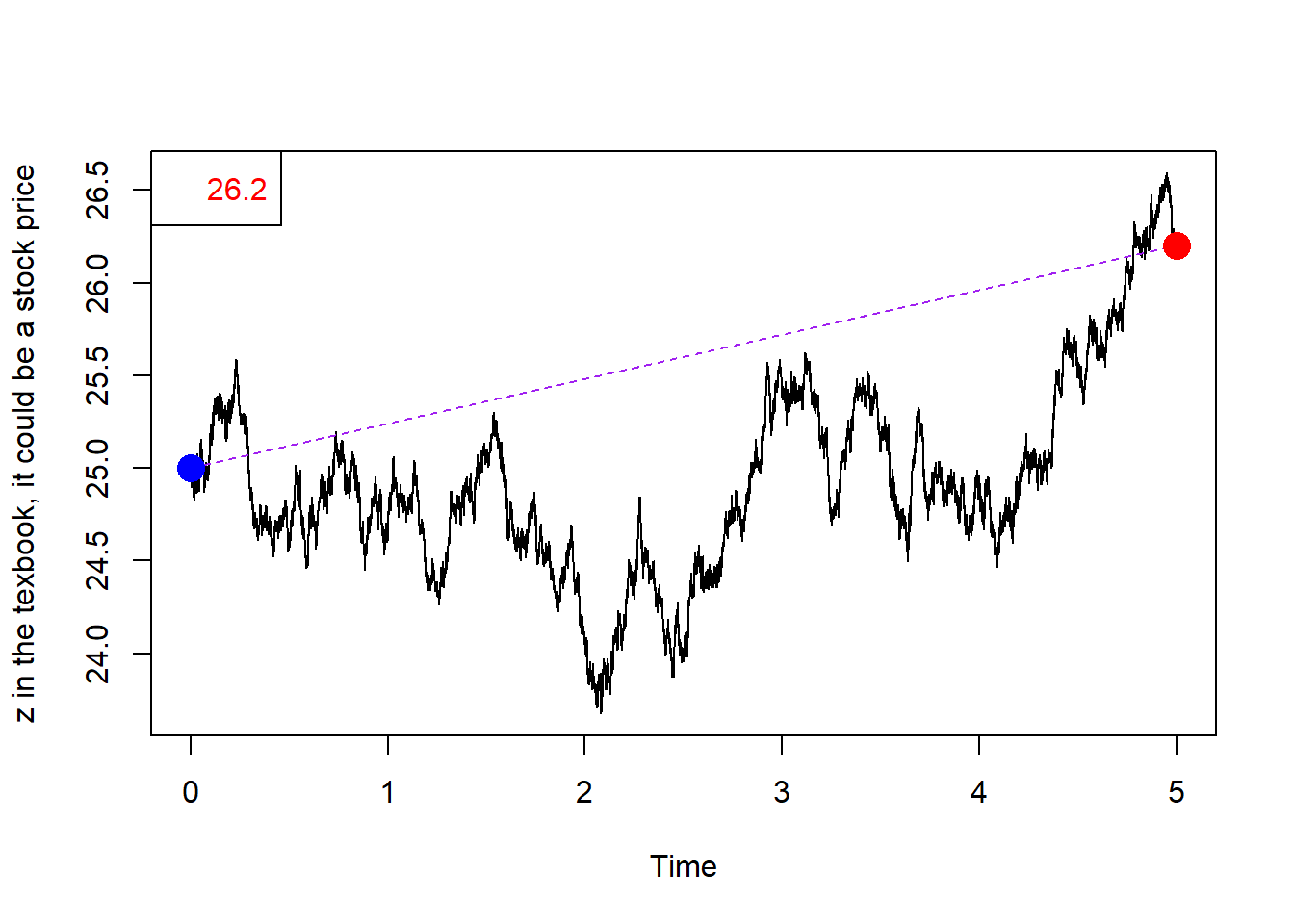

A simple Wiener process.

Graphically:

Code

plot(Time, z, type = "l",

ylab = "z in the texbook, it could be a stock price",

xlab = "Time")

lines(Time, seq(25, (25 + sum(delta_z)), length.out = N), lty = 2,

col = "purple")

points(Time[1], 25, col = "blue", cex = 2, pch = 16)

points(Time[N], z[N], col = "red", cex = 2, pch = 16)

legend("topleft", legend = c(round(z[N], 2)), bg = "white",

text.col = "red")

This is a 1,000 step version of four Wiener processes:

This is supposed to mimic (at some extent) the evolution of a stock price.

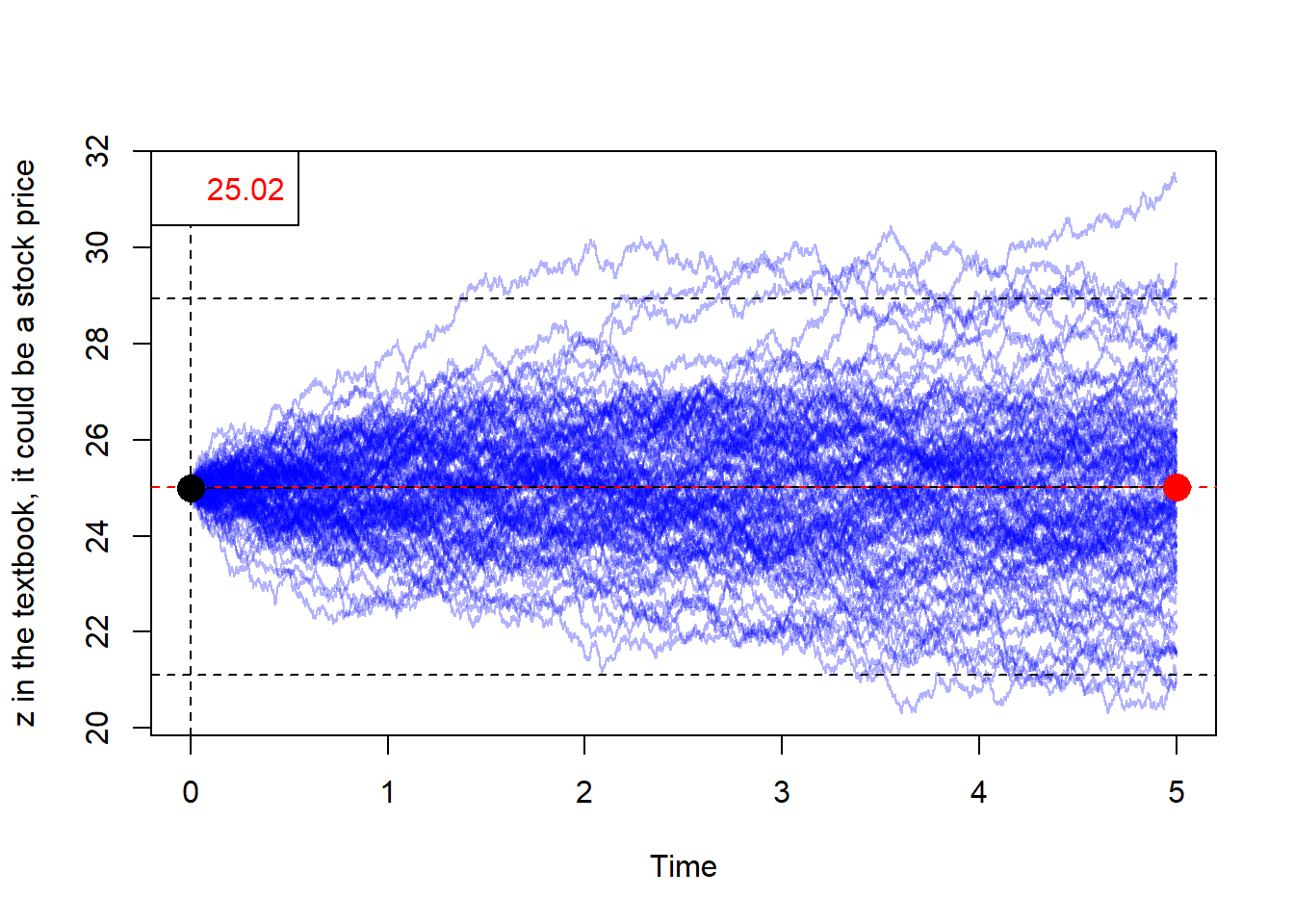

Now, we propose to produce 100 processes.

Code

# 100 Wiener processes.

set.seed(365633)

mat.delta_z <- matrix(rnorm(100 * N, mean = 0, sd = 1) * sqrt(dt), 100, N)

mat.z1 <- 25 + t(apply(mat.delta_z, 1, cumsum))

mat.z <- t(cbind(matrix(25, 100), mat.z1))

Time2 <- c(0, Time)

pred <- mean(mat.z[(N + 1), ])

# 95% range.

rangetop <- pred + qnorm(0.975) * var(mat.z[(N + 1), ])^0.5

rangedown <- pred - qnorm(0.975) * var(mat.z[(N + 1), ])^0.5Graphically.

Code

matplot(Time2, mat.z, type = "l", lty = 1, col = rgb(0, 0, 1, 0.3),

ylab = "z in the textbook, it could be a stock price",

xlab = "Time")

abline(h = pred, lty = 2, col = "red")

abline(v = 0, lty = 2)

lines(Time2, seq(25, pred, length.out = N + 1), lty = 2)

points(Time2[N + 1], pred, col = "red", cex = 2, pch = 16)

points(0, 25, col = "black", cex = 2, pch = 16)

legend("topleft", legend = c(round(pred, 2)), bg = "white",

text.col = "red")

abline(h = rangetop, lty = 2)

abline(h = rangedown, lty = 2)

Let’s check how many simulated terminal values fall outside this 95% prediction range.

This means that 5 paths are outside this simulated 95% prediction range.

Min. 1st Qu. Median Mean 3rd Qu. Max.

20.97 23.79 24.96 25.02 26.06 31.38 A potential problem is that \(z\) values can be negative. This is problematic when we are interested to model stock prices.

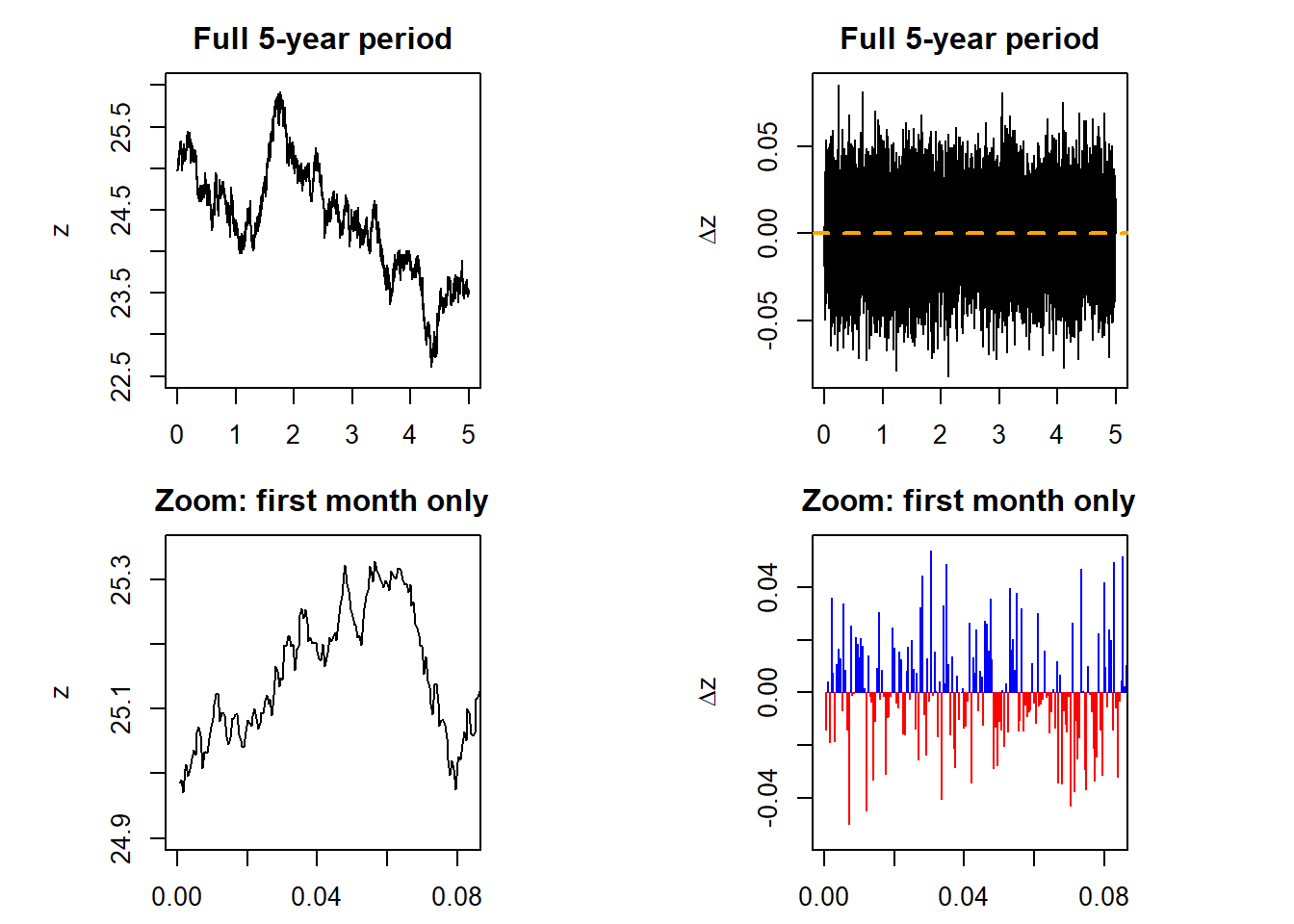

Let’s explore deeper the stochastic process below.

Code

set.seed(1)

delta_z <- rnorm(N, 0, 1) * dt^0.5

z <- 25 + cumsum(delta_z)

### A stochastic process

par(mfrow = c(2, 2), mai = c(0.4, 0.4, 0.4, 0.4))

par(pty = "s")

plot(Time, z, type = "l", xlim = c(0, TT), ylim = c(22.5, 26),

main = "Full 5-year period", ylab = "z", xlab = "Time")

plot(Time, delta_z, type = "h", xlim = c(0, TT),

main = "Full 5-year period",

ylab = expression(paste(Delta,z)), xlab = "Time")

abline(h = 0, lty = 2, col = "orange", lwd = 2)

plot(Time, z, type = "l", xlim = c(0, 1/12), ylim = c(24.9, 25.35),

main = "Zoom: first month only", xlab = "Time")

plot(Time, delta_z, type = "h", xlim = c(0, 1/12),

col = ifelse(delta_z < 0, "red", "blue"), ylim = c(-0.055, 0.055),

main = "Zoom: first month only",

ylab = expression(paste(Delta,z)), xlab = "Time")

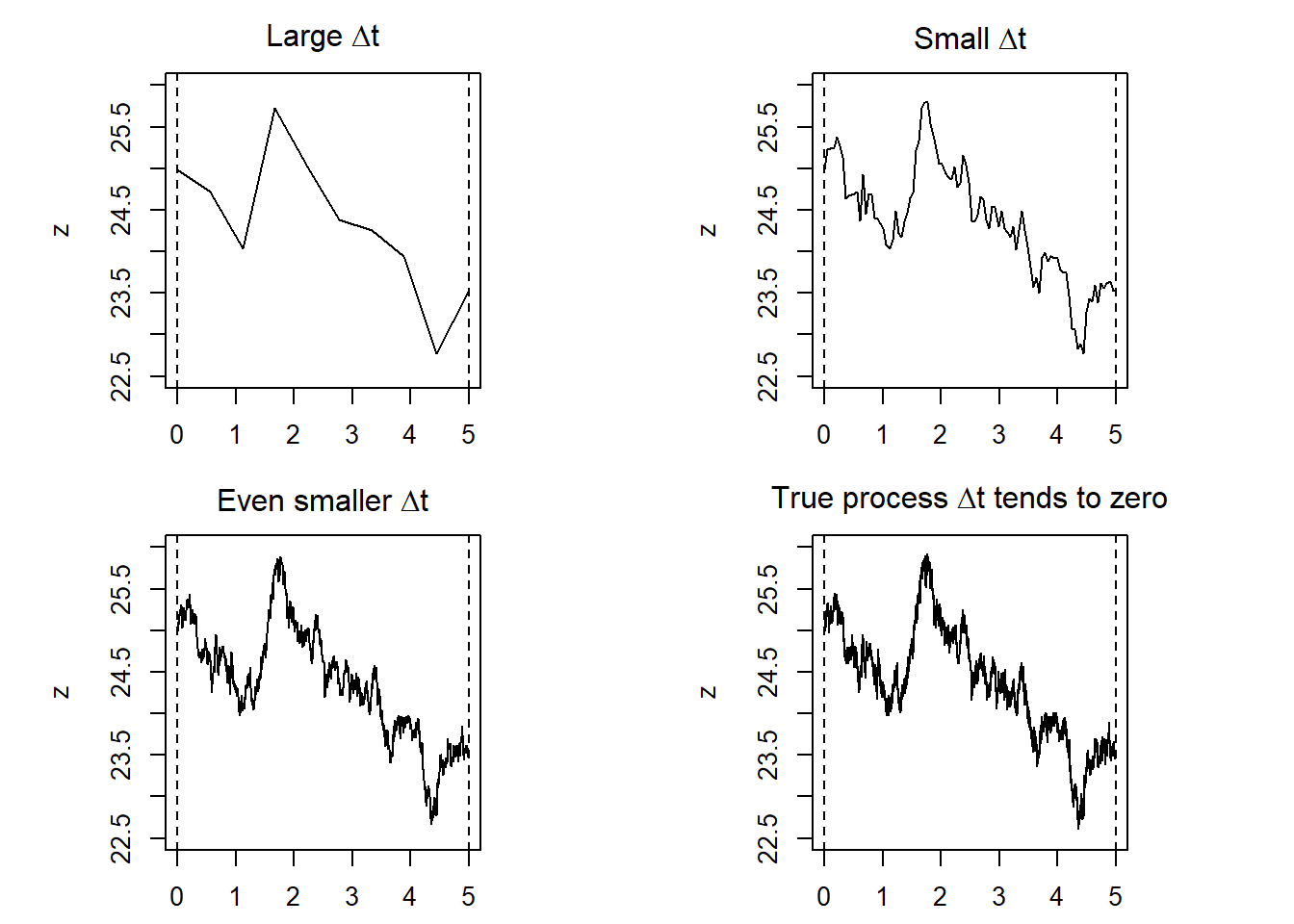

These processes are driven by a random component. The lower panel is revealing because we can see how the random component goes from positive to negative without any pattern, it is entirely random. Now, let’s explore the role of \(\Delta t\).

Code

par(mfrow = c(2, 2), mai = c(0.4, 0.4, 0.4, 0.4))

par(pty = "s")

plot(Time[(seq(from = 1, to = N, length.out = 10))],

z[(seq(from = 1, to = N, length.out = 10))], type = "l",

ylim = c(22.5, 26), main = expression(paste("Large ",Delta,t)),

ylab = "z")

abline(v = 0, lty = 2)

abline(v = 5, lty = 2)

plot(Time[(seq(from = 1, to = N, length.out = 100))],

z[(seq(from = 1, to = N, length.out = 100))], type = "l",

ylim = c(22.5, 26), ylab = "z",

main = expression(paste("Small ",Delta,t)))

abline(v = 0, lty = 2)

abline(v = 5 , lty = 2)

plot(Time[(seq(from = 1, to = N, length.out = 1000))],

z[(seq(from = 1, to = N, length.out = 1000))], type = "l",

ylim = c(22.5, 26), ylab = "z",

main = expression(paste("Even smaller ",Delta,t)))

abline(v = 0, lty = 2)

abline(v = 5 , lty = 2)

plot(Time, z, type = "l", ylim = c(22.5, 26), # length 10,000

main = expression(paste("True process ",Delta,t, " ",

"tends ","to ","zero")))

abline(v = 0, lty = 2)

abline(v = 5, lty = 2)

The \(\Delta t\) value determines how frequent are the changes in \(z\).

A few properties of stochastic processes.

3.2 The generalized Wiener process

Now let’s analyze the case of the generalized Wiener process.

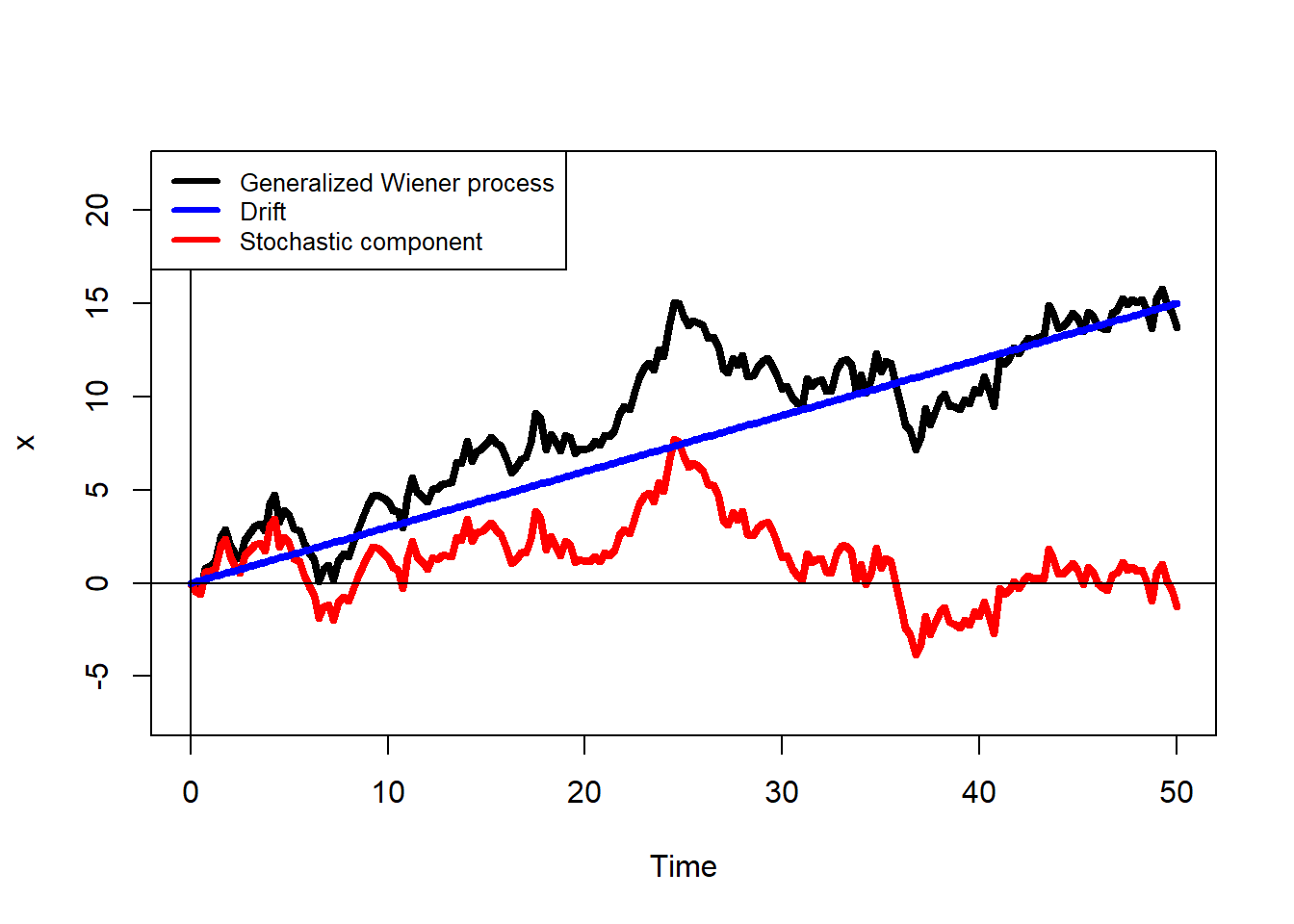

\(\Delta x = a \Delta t + b \epsilon \sqrt{\Delta t}\). Assume \(a=0.3\) and \(b=1.5\):

Graphically:

Code

plot(Time, x, type = "l", lwd = 4, ylim = c(-7, 22))

lines(Time, z, col = "red", lwd = 4)

lines(Time, 0.3 * Time, col = "blue", lwd = 4)

abline(0, 0)

abline(v = 0)

legend("topleft", legend = c("Generalized Wiener process",

"Drift", "Stochastic component"),

col = c("black", "blue", "red"), lwd = 3,

bg = "white", cex = 0.8)

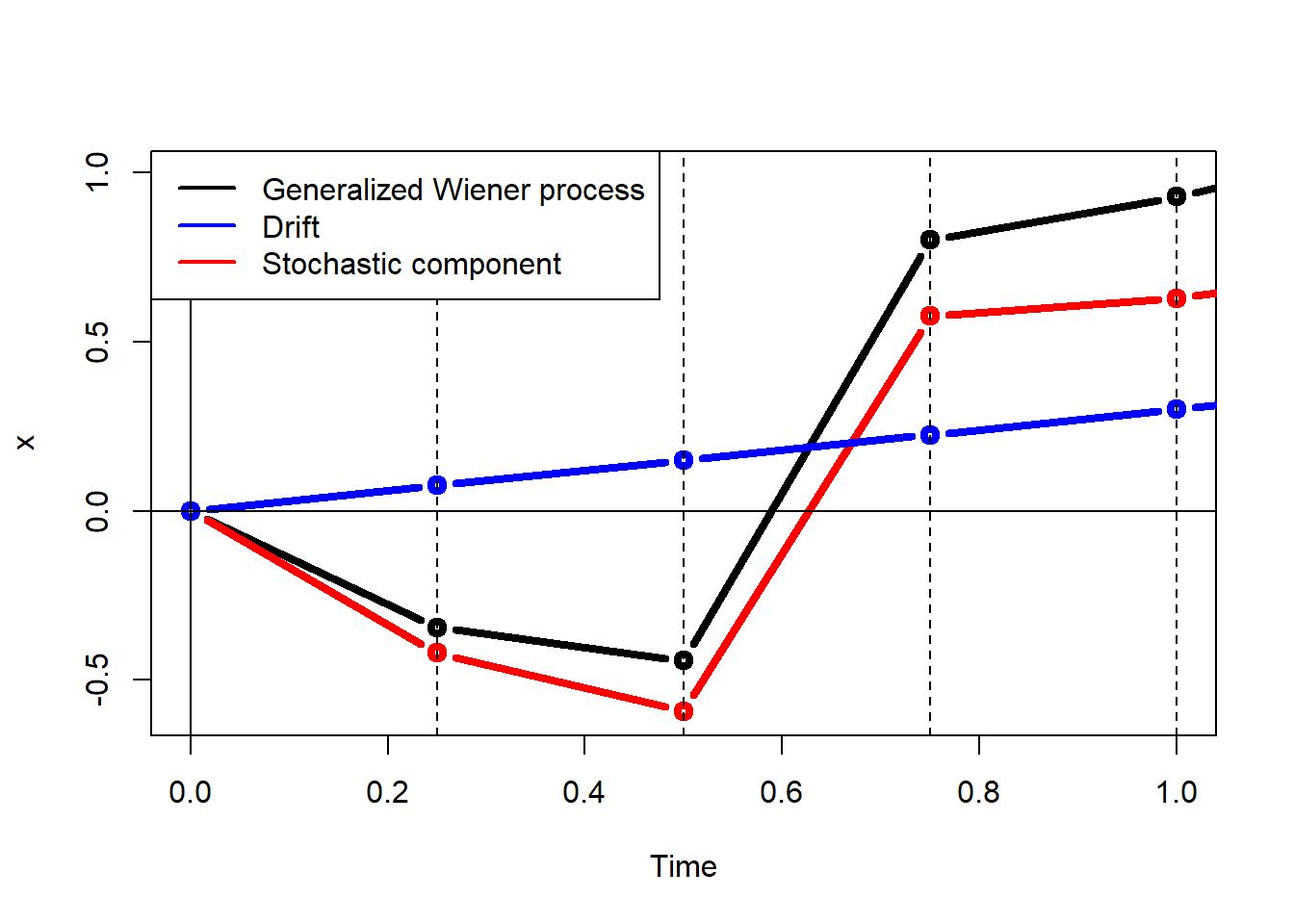

Here, the generalized Wiener process \(\Delta x\) is decomposed into the drift \(a \Delta t\) and the stochastic component \(b \epsilon \sqrt{\Delta t}\). A zoom of the same plot.

Code

# Figure 14.2 Zoom

plot(Time, x, type = "b", ylim = c(-0.6, 1), xlim = c(0, 1), lwd = 4)

lines(Time, z, col = "red", lwd = 4, type = "b")

lines(Time, 0.3 * Time, col = "blue", lwd = 4, type = "b")

abline(0, 0)

abline(v = 0)

abline(v = dt, lty = 2)

abline(v = dt * 2, lty = 2)

abline(v = dt * 3, lty = 2)

abline(v = dt * 4, lty = 2)

#points(dt, 0, pch = 1, col = "blue", lwd = 2)

#points(dt * 2, 0, pch = 1, col = "blue", lwd = 2)

#points(dt * 3, 0, pch = 1, col = "blue", lwd = 2)

#points(dt * 4, 0, pch = 1, col = "blue", lwd = 2)

legend("topleft", legend = c("Generalized Wiener process",

"Drift", "Stochastic component"),

col = c("black", "blue", "red"), lty = 1,

bg = "white", lwd = 2)

This is a nice visual representation of: generalized = drift + Wiener.

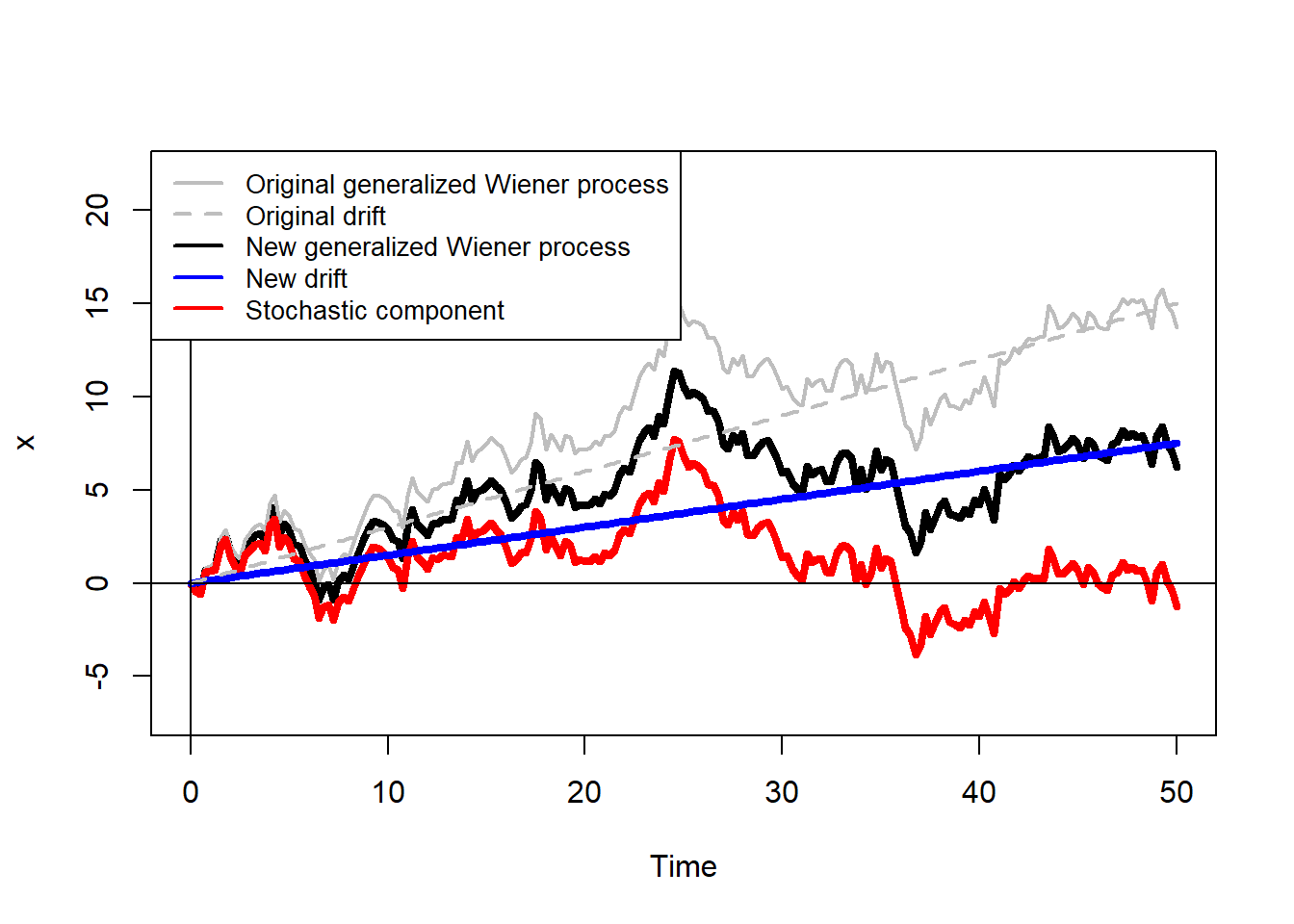

See how the process changes when we consider a lower value of \(a\).

Code

set.seed(123)

delta_xlow <- (0.15 * dt) + delta_z

xlow <- c(0, cumsum(delta_xlow))

# Now plot.

plot(Time, xlow, type = "l", ylim = c(-7, 22), lwd = 4, ylab = "x")

lines(Time, x, lwd = 2, col = "grey")

lines(Time, z, lwd = 4, col = "red")

lines(Time, 0.15 * Time, lwd = 4, col = "blue")

lines(Time, 0.3 * Time, lty = 2, lwd = 2, col = "grey")

abline(0, 0)

abline(v = 0)

legend("topleft", legend = c("Original generalized Wiener process",

"Original drift", "New generalized Wiener process", "New drift",

"Stochastic component"), lty = c(1, 2, 1, 1, 1),

bg = "white", lwd = 2,

col = c("grey", "grey", "black", "blue", "red"), cex = 0.85)

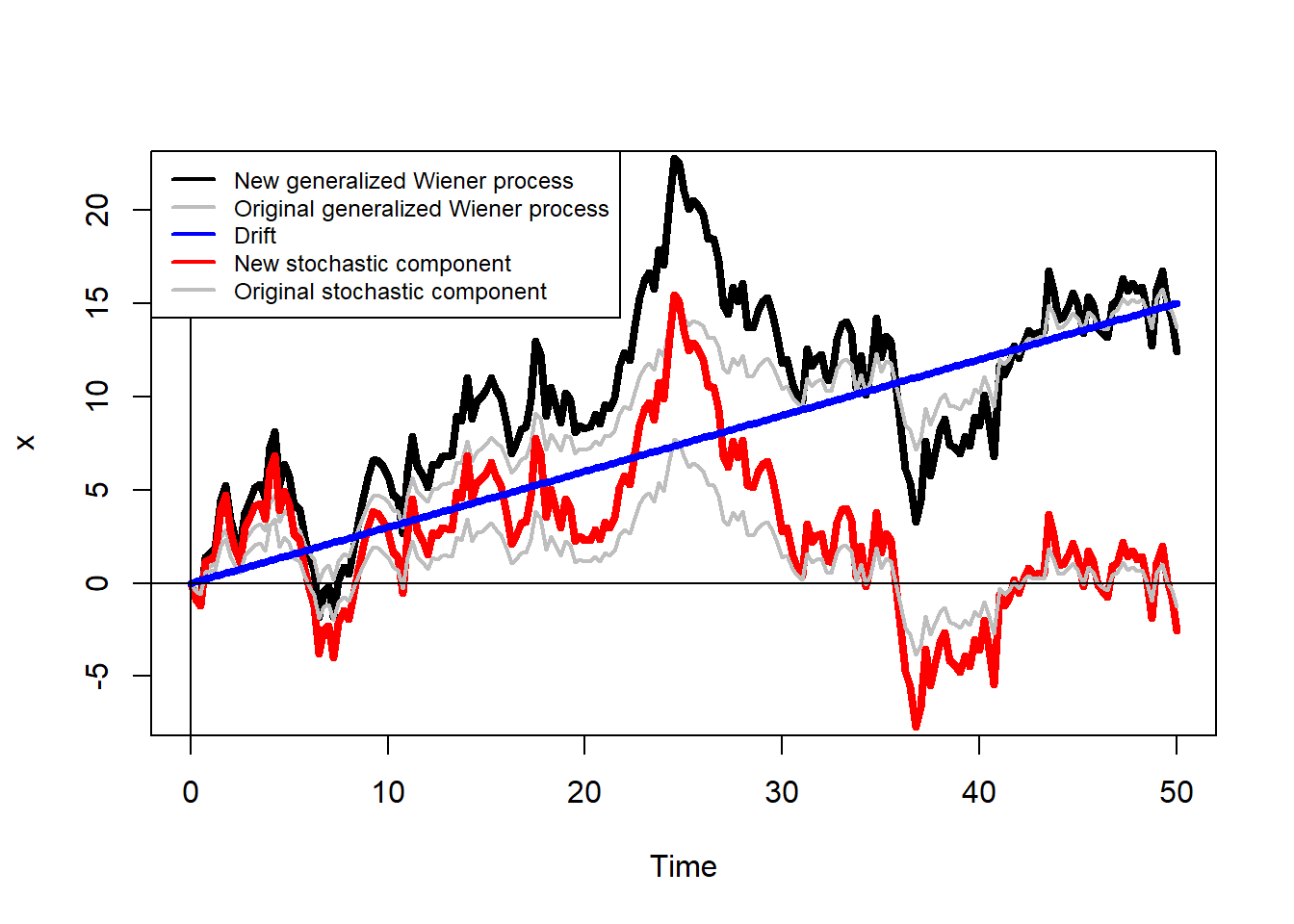

And a higher value of \(b\).

Code

set.seed(123)

delta_zhigh <- 3 * rnorm(N, 0, 1) * dt^0.5

delta_xhigh <- (0.3 * dt) + delta_zhigh

xhigh <- c(0, cumsum(delta_xhigh))

zhigh <- c(0, cumsum(delta_zhigh))

plot(Time, xhigh, type = "l", ylim = c(-7, 22), lwd = 4, ylab = "x")

lines(Time, x, lwd = 2, col = "grey")

lines(Time, zhigh, lwd = 4, col = "red")

lines(Time, z, lwd = 2, col = "grey")

lines(Time, 0.3 * Time, lwd = 4, col = "blue")

abline(0, 0)

abline(v = 0)

legend("topleft", legend = c("New generalized Wiener process",

"Original generalized Wiener process", "Drift" ,

"New stochastic component", "Original stochastic component"),

lty = 1, bg = "white", lwd = 2,

col = c("black", "grey", "blue", "red", "grey"), cex = 0.75)

Note the changes are now more pronounced.

This is a replication of Hull (2015), table 14.1. Simulation of stock price when \(\mu= 0.15\) and \(\sigma = 0.30\) during 1-week periods.

Code

# Table 14.1

set.seed(19256)

delta_S <- rep(0, 10)

S <- rep(100, 10)

epsilon <- rep(0, 10)

for(i in 1:10){

epsilon[i] <- rnorm(1, 0, 1)

delta_S[i] <- 0.15 * (1 / 52) * S[i] + 0.3 * ((1 / 52)^0.5) *

epsilon[i] * S[i]

S[i+1] <- S[i] + delta_S[i]

}

epsilon <- c(epsilon, NA)

delta_S <- c(delta_S, NA)

results <- data.frame(S, epsilon, delta_S)

results S epsilon delta_S

1 100.0000 0.8268625 3.7284174

2 103.7284 0.4957988 2.4387684

3 106.1672 -0.9313823 -3.8074983

4 102.3597 -0.1495925 -0.3417592

5 102.0179 0.7310239 3.3968957

6 105.4148 -0.6111472 -2.3761181

7 103.0387 1.2490868 5.6516490

8 108.6904 -0.6243389 -2.5096009

9 106.1808 0.6995349 3.3964067

10 109.5772 0.3612549 1.9629353

11 111.5401 NA NAIt is interesting to note that in Hull (2015) the final simulated price is $111.54 and here it is $111.5401. Is this a pure coincidence?

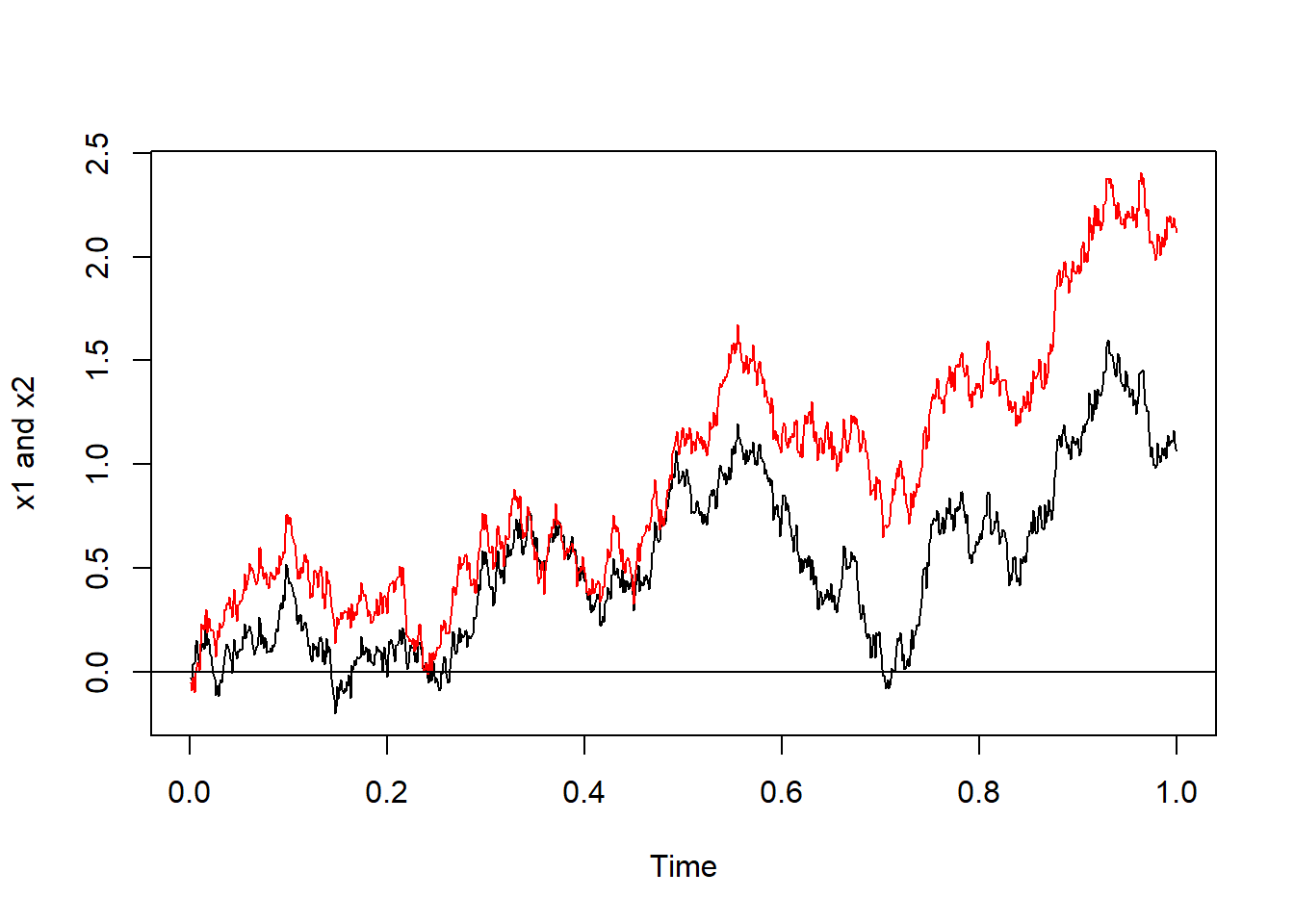

A correlated process.

\(\Delta x_1 = a_1 \Delta t + b_1 \epsilon_1 \sqrt{\Delta t}\),

\(\Delta x_2 = a_2 \Delta t + b_2 \epsilon_2 \sqrt{\Delta t}\).

Where: \(\epsilon_1 = u\), and \(\epsilon_2=\rho u + \sqrt{1-\rho^{2}}v\).

Code

# Section 14.5

rho <- 0.8

TT <- 1

steps <- 1000

dt <- TT / steps

Time <- seq(from = dt, to = TT, by = dt)

set.seed(123)

e1 <- rnorm(steps, 0, 1)

e2 <- rho * e1 + ((1 - rho^2)^0.5) * rnorm(steps, 0, 1)

delta_z1 <- 1.5 * e1 * dt^0.5

delta_z2 <- 1.5 * e2 * dt^0.5

delta_x1 <- (0.3 * dt) + delta_z1

delta_x2 <- (0.3 * dt) + delta_z2

x1 <- cumsum(delta_x1)

x2 <- cumsum(delta_x2)

x <- c(x1, x2)Assume \(a=0.3\), \(b=1.5\) and \(\rho=0.8\). Visually:

Code

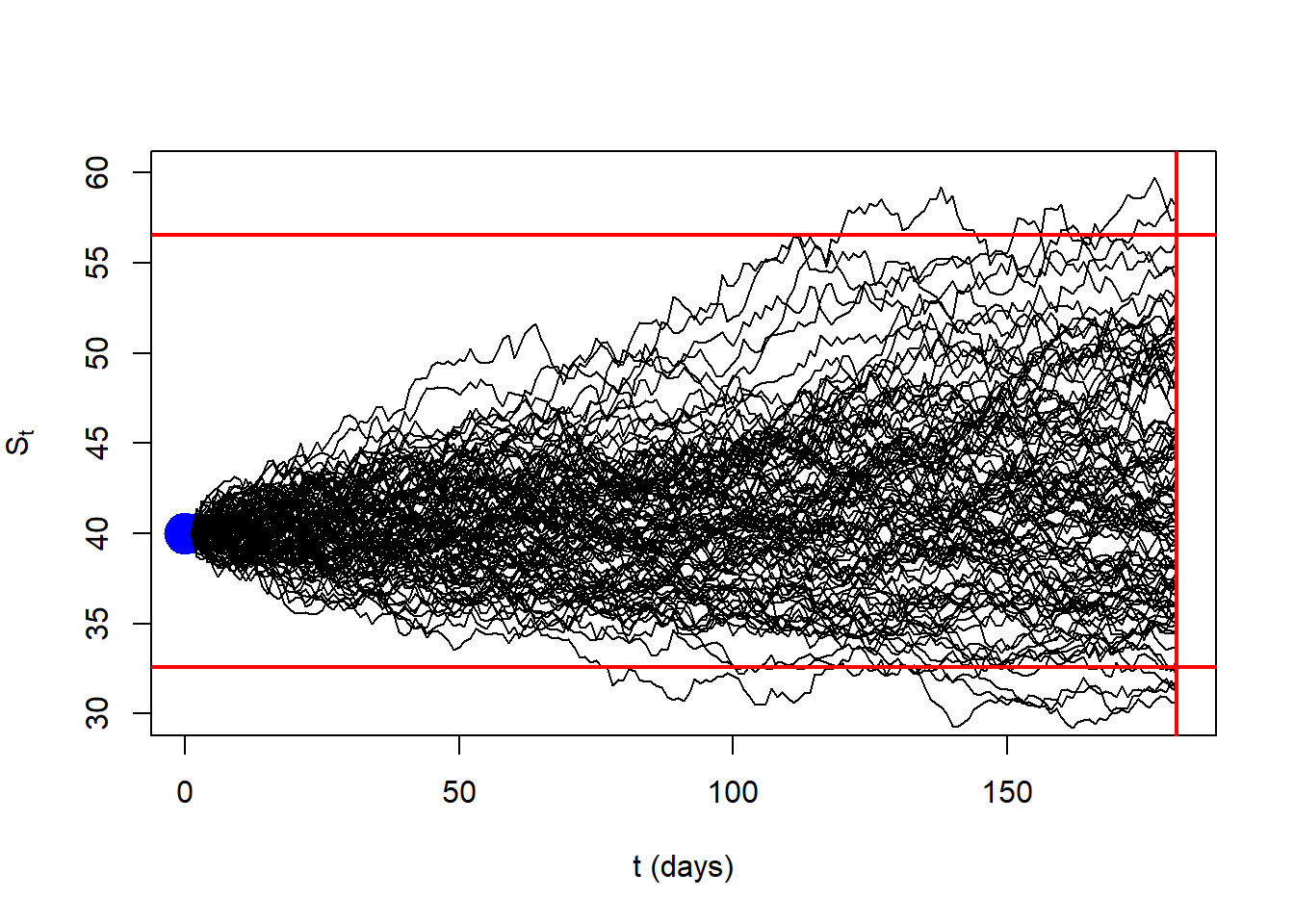

The model of stock price behavior implies that a stock’s price at time \(T\), given its price today, is lognormally distributed. The following is similar to example 15.1 in Hull (2015). In particular, consider a stock with an initial price of $40, an expected return of 16% per annum, and a volatility of 20% per annum.

\(\frac{\Delta S}{S} = a \Delta t + b \epsilon \sqrt{\Delta t}\),

\(\frac{\Delta S}{S} = 0.16 \Delta t + 0.2 \epsilon \sqrt{\Delta t}\),

Assume \(\Delta t = \frac{1}{365}\): \(\frac{\Delta S}{S} = 0.16 \frac{1}{365} + 0.2 \epsilon \sqrt{\frac{1}{365}}\),

Calculate the constants:

Finally: \(\Delta S = 0.0004383562 S + 0.01046848 S \epsilon\). The 100 simulated 6-months paths of the stock price \(S\) are:

Code

set.seed(10101010)

for(j in 1:100) {

delta_S <- NULL

S <- rep(40, 180) # Now it is 40 for all days, the loop fill this out.

epsilon <- NULL

for(i in 1:180) {

epsilon[i] <- rnorm(1, 0, 1)

delta_S[i] <- 0.16 * (1 / 365) * S[i] + 0.2 * ((1 / 365)^0.5) *

epsilon[i] * S[i]

S[i+1] <- S[i] + delta_S[i]

}

if (j==1) {

plot(S, type = "l", ylim = c(30, 60),

ylab = expression(paste(S[t])), xlab = "t (days)")

points(0, 40, pch = 19, col = "blue", cex = 3)

abline(h = 10, col = "red", lwd = 3)

}

lines(S)

}

abline(h = 32.55, lwd = 2, col = "red")

abline(h = 56.56, lwd = 2, col = "red")

abline(v = 181, lwd = 2, col = "red")

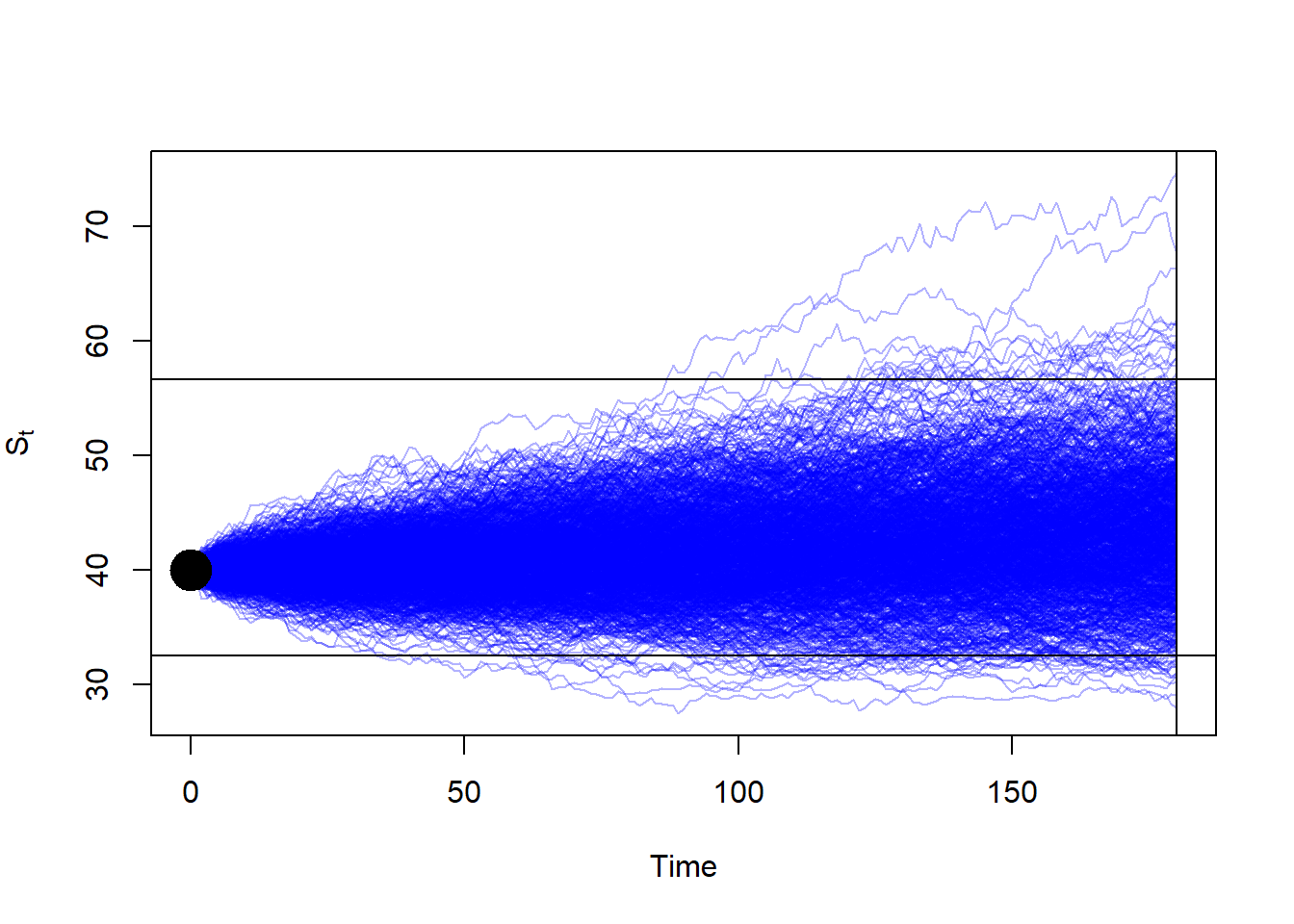

The code above can be problematic because we are not collecting all paths in an object. An alternative code is the following. Again, this is similar to example 15.1 in Hull (2015).

Code

S0 <- 40

nDays <- 360

mu <- 0.16

sig <- 0.2

TT <- 0.5

mean.logST <- log(S0)+(mu - (sig^2 / 2)) * TT

variance.logST <- sig^2 * TT

lower.ST <- exp(mean.logST + qnorm(0.025) * variance.logST^0.5)

upper.ST <- exp(mean.logST + qnorm(0.975) * variance.logST^0.5)

set.seed(3)

nSim <- 1000

nSteps <- nDays * TT

SP_sim <- matrix(0, nrow = nSteps + 1, ncol = nSim)

for(i in 1:nSim){

SVec <- rep(0, nSteps + 1)

SVec[1] <- S0

for(j in 2:(nSteps + 1)){

DeltaS <- mu * SVec[j - 1] * (1 / nDays) + sig * SVec[j - 1] *

rnorm(1) * (1 / nDays)^0.5

SVec[j] <- SVec[j - 1] + DeltaS

}

SP_sim[, i] <- SVec

}Now, let’s plot the results.

Code

Let’s verify that there is approximately a 95% probability that the stock price in 6 months will lie between the lower and upper bounds shown above.

[1] 0.967Code

[1] 32.51491[1] 56.6029Nice.

This is how a stock price evolves according to the Black-Scholes formula.