As in the previous chapter, the problem is to forecast one monthly time series: Beer, Wine, and Distilled Alcoholic Beverages Sales, following the original Matt Dancho example. The data comes from FRED, the Federal Reserve Economic Data database. The series belongs to the non-durable goods category; it includes U.S. merchant wholesalers, excluding manufacturers’ sales branches and offices. The observations run from 2010-01-01 to 2022-10-31. The goal is to estimate models with information available before 2022 and evaluate their forecasts over the 10 available months of 2022.

For the full database details see: https://fred.stlouisfed.org/series/S4248SM144NCEN

First load the R packages.

Code

# Load libraries.library(fpp3)library(timetk) # Toolkit for working with time series in R.library(tidyquant) # Loads tidyverse, financial packages, and data tools.library(dplyr) # Database manipulation.library(ggplot2) # Plots.library(tibble) # Tables.library(kableExtra) # Tables.library(knitr)library(sweep) # Broom-style tidiers for the forecast package.library(forecast) # Forecasting models and predictions package.library(seasonal)library(lubridate)library(rpart) # Lightweight regression trees.library(nnet) # Lightweight neural networks.

Code

# This comes from 01-forecasting-with-fpp3.qmd.mape_updated <-readRDS("mape_updated.rds")

We can conveniently download the data directly from the FRED API in one line of code.

Code

# Beer, Wine, Distilled Alcoholic Beverages, in Millions USD.beer <-tq_get("S4248SM144NCEN", get ="economic.data",from ="2010-01-01", to ="2022-10-31")if (!is.data.frame(beer) ||!all(c("date", "price") %in%names(beer))) { fred_beer <-read.csv("https://fred.stlouisfed.org/graph/fredgraph.csv?id=S4248SM144NCEN",stringsAsFactors =FALSE ) beer <- fred_beer %>%transmute(date =as.Date(observation_date),price =as.numeric(S4248SM144NCEN) ) %>%filter(date >=as.Date("2010-01-01"), date <=as.Date("2022-10-31")) %>%filter(!is.na(price))}if (!is.data.frame(beer) ||!all(c("date", "price") %in%names(beer))) {stop("The FRED beer sales series could not be loaded as a data frame.")}

The first rows show the structure of the data set. By default the value column is named price, although these are sales figures in monetary terms. According to the main FRED reference, these are in millions of dollars and are reported before seasonal adjustment.

The column name now identifies the variable as sales.

2.1 Supervised forecasting workflow

In this chapter, machine learning is used as a forecasting tool. The goal is narrowly defined: forecast a monthly time series by turning calendar and trend information into predictors. In time series forecasting, the supervised learning idea is to transform an ordered sequence into a modeling table: build a table of predictors called \(X\), keep the variable we want to forecast as \(y\), estimate a model on the training data, tune it with validation data, and evaluate it once on the test data.

This chapter uses the same forecasting problem as before with an explicit supervised forecasting workflow. The chapter writes the model comparison directly: we create the predictors, choose the candidate model families, tune the few hyperparameters by hand, and evaluate the final models on a holdout period. The models are smaller, faster to render in Quarto, easier to explain, and easier to debug. The workflow is also close to what students need to understand:

create time-based features;

split the data without shuffling the time order;

fit several explicit models;

choose hyperparameters with the validation set;

evaluate the chosen models on a test set held apart from fitting and tuning.

We will compare three transparent machine-learning forecasting alternatives:

a multivariate linear regression;

a regression tree;

a small neural network.

The first model is highly interpretable. The tree is nonlinear and can capture simple threshold behavior. The neural network is also nonlinear. We keep it small so the model remains pedagogical and reproducible.

Mathematically, this chapter changes the forecasting problem from a univariate time-series model into a supervised forecasting regression problem. The first chapter used models built directly from the history of the series. This chapter turns each month into one row of a modeling table:

Row element

Meaning

sales

The value we want to forecast.

index.num

A numeric time trend.

year

A coarse trend variable and split variable.

month.lbl

Monthly seasonality.

Then each supervised forecasting model estimates a rule

\[

\text{sales} = f(\text{trend and month variables}) + \text{error}.

\]

The three alternatives below differ in how flexible we allow the rule to be. Linear regression uses an additive straight-line rule. The regression tree uses if-then splits. The neural network uses a small nonlinear rule. The transparency principle is simple: we can see the columns, we can see the candidate model families, and the test set is reserved for the final evaluation.

The data split has three different jobs:

Sample

Dates

Job in the workflow

Training

2010-2020

Estimate model parameters.

Validation

2021

Choose hyperparameters such as tree complexity or neural-network size.

Test

January-October 2022

Evaluate the selected models once.

2.2 The data

We need an additional data set. The validation data set is used for model selection: it helps us choose hyperparameters before touching the final test period. The new data sets are the following.

Code

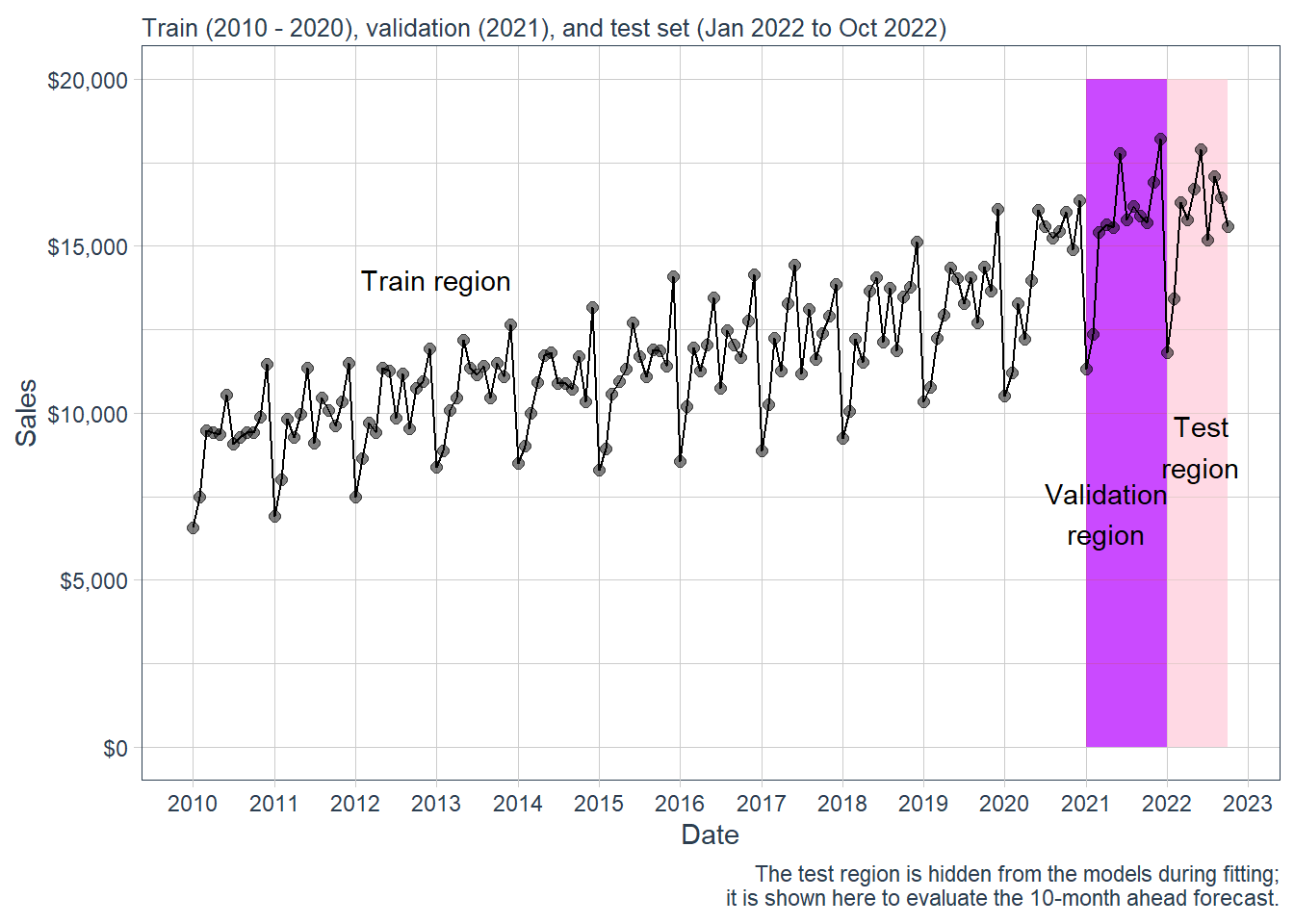

beer %>%ggplot(aes(date, sales)) +annotate("text", x =ymd("2013-01-01"), y =14000,color ="black", label ="Train region") +geom_rect(xmin =as.numeric(ymd("2021-01-01")),xmax =as.numeric(ymd("2021-12-31")), ymin =0, ymax =20000,alpha =0.01, fill ="purple") +annotate("text", x =ymd("2021-04-01"), y =7000,color ="black", label ="Validation\nregion") +geom_rect(xmin =as.numeric(ymd("2022-01-01")),xmax =as.numeric(ymd("2022-09-30")), ymin =0, ymax =20000,alpha =0.02, fill ="pink") +annotate("text", x =ymd("2022-06-01"), y =9000,color ="black", label ="Test\nregion") +geom_line(col ="black") +geom_point(col ="black", alpha =0.5, size =2) +theme_tq() +scale_x_date(date_breaks ="1 year", date_labels ="%Y") +labs(subtitle ="Train (2010 - 2020), validation (2021), and test set (Jan 2022 to Oct 2022)",x ="Date", y ="Sales",caption ="The test region is hidden from the models during fitting; it is shown here to evaluate the 10-month ahead forecast.") +scale_y_continuous(labels = scales::dollar)

Figure 2.1: Beer sales: train, validation and test sets.

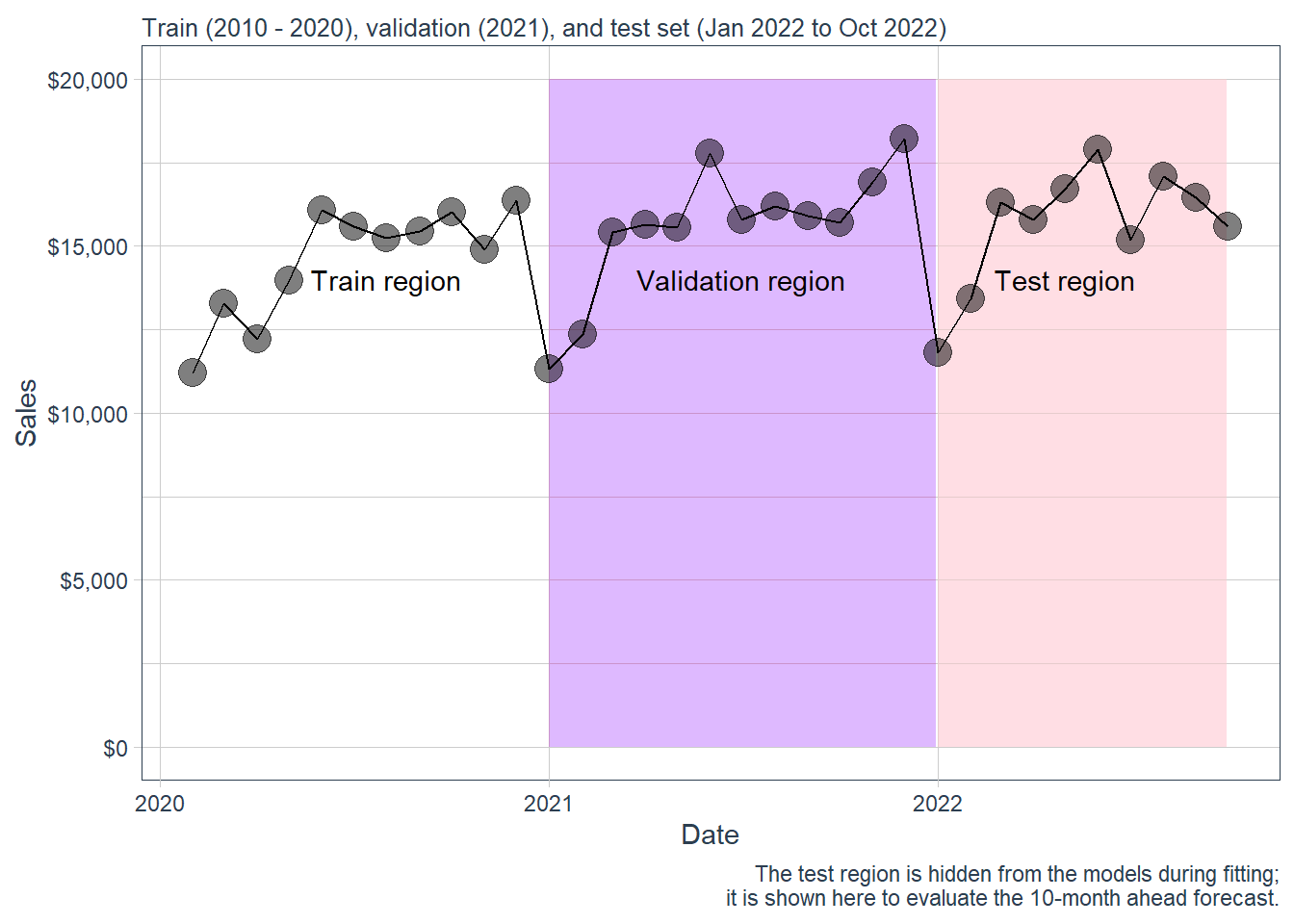

And the corresponding zoom version.

Code

beer %>%filter(date >as.Date("2020-01-01")) %>%ggplot(aes(date, sales)) +annotate("text", x =ymd("2020-08-01"), y =14000,color ="black", label ="Train region") +geom_rect(xmin =as.numeric(ymd("2021-01-01")),xmax =as.numeric(ymd("2021-12-31")), ymin =0, ymax =20000,alpha =0.01, fill ="purple") +annotate("text", x =ymd("2021-07-01"), y =14000,color ="black", label ="Validation region") +geom_rect(xmin =as.numeric(ymd("2022-01-01")),xmax =as.numeric(ymd("2022-09-30")), ymin =0, ymax =20000,alpha =0.02, fill ="pink") +annotate("text", x =ymd("2022-05-01"), y =14000,color ="black", label ="Test region") +geom_line(col ="black") +geom_point(col ="black", alpha =0.5, size =5) +theme_tq() +scale_x_date(date_breaks ="1 year", date_labels ="%Y") +labs(subtitle ="Train (2010 - 2020), validation (2021), and test set (Jan 2022 to Oct 2022)",x ="Date", y ="Sales",caption ="The test region is hidden from the models during fitting; it is shown here to evaluate the 10-month ahead forecast.") +scale_y_continuous(labels = scales::dollar)

Figure 2.2: Zoom. Beer sales: train, validation and test sets.

The tk_augment_timeseries_signature() function expands the timestamp information column-wise into a forecasting feature set. The original data set has a date, a symbol, and the sales variable. The augmented data includes calendar information such as year, month, quarter, semester and other time features. Only some of them will be useful for the final models. The full list still helps us inspect the forecasting problem as a supervised forecasting problem.

The full signature is useful for inspection. For this monthly data set, it is broader than necessary. Many columns describe hours, seconds, weekdays, or day-of-month details. They are meaningful for hourly or daily data. In this monthly problem, they mostly encode calendar artifacts. We keep a smaller set:

sales, the target variable;

index.num, a numeric time index for the trend;

year, a coarse trend variable that also makes the split readable;

month.lbl, a factor for monthly seasonality.

This modeling decision keeps the target variable intact and makes the supervised forecasting matrix easier to explain. It also reduces dependence on irrelevant timestamp fragments.

The retained features define the design matrix used by the models. Because month.lbl is a categorical variable, R expands it internally into 0/1 dummy variables. For example, define

\[

D_{t,\text{Feb}} =

\begin{cases}

1, & \text{month } t \text{ is February},\\

0, & \text{otherwise.}

\end{cases}

\]

The same idea is repeated for March through December. Conceptually, the row for month \(t\) is

January is absorbed into the intercept by default. The important forecasting point is that every predictor in \(x_t\) is known before the sales value \(y_t\) is observed. Future dates, years, and months are known in advance, so these predictors keep the future sales value unavailable to the model.

Code

selected_ml_columns <-c("sales", "index.num", "year", "month.lbl")feature_decisions <-tibble(variable =colnames(beer_aug)) %>%mutate(decision =case_when( variable =="sales"~"Target", variable %in% selected_ml_columns ~"Keep",TRUE~"Drop" ),reason =case_when( variable =="sales"~"Value we want to forecast.", variable =="index.num"~"Numeric trend over time.", variable =="year"~"Coarse trend and readable split variable.", variable =="month.lbl"~"Monthly seasonal factor.", variable =="date"~"Raw Date object; useful for plots; excluded as a direct predictor here.", variable =="symbol"~"Constant because there is only one series.", variable %in%c("hour", "minute", "second", "hour12", "am.pm") ~"Intraday information; irrelevant for monthly observations.", variable %in%c("day", "wday", "wday.xts", "wday.lbl", "mday","qday", "yday", "mweek", "week", "week.iso","week2", "week3", "week4", "mday7") ~"Daily or weekly calendar artifact for monthly data.",TRUE~"Redundant with the retained trend or monthly seasonality variables." ) )kable(feature_decisions,caption ="Feature-selection decision for the time-series signature.",row.names =FALSE) %>%kable_styling(latex_options ="HOLD_position")

Feature-selection decision for the time-series signature.

variable

decision

reason

symbol

Drop

Constant because there is only one series.

date

Drop

Raw Date object; useful for plots; excluded as a direct predictor here.

sales

Target

Value we want to forecast.

index.num

Keep

Numeric trend over time.

diff

Drop

Redundant with the retained trend or monthly seasonality variables.

year

Keep

Coarse trend and readable split variable.

year.iso

Drop

Redundant with the retained trend or monthly seasonality variables.

half

Drop

Redundant with the retained trend or monthly seasonality variables.

quarter

Drop

Redundant with the retained trend or monthly seasonality variables.

month

Drop

Redundant with the retained trend or monthly seasonality variables.

month.xts

Drop

Redundant with the retained trend or monthly seasonality variables.

month.lbl

Keep

Monthly seasonal factor.

day

Drop

Daily or weekly calendar artifact for monthly data.

hour

Drop

Intraday information; irrelevant for monthly observations.

minute

Drop

Intraday information; irrelevant for monthly observations.

second

Drop

Intraday information; irrelevant for monthly observations.

hour12

Drop

Intraday information; irrelevant for monthly observations.

am.pm

Drop

Intraday information; irrelevant for monthly observations.

wday

Drop

Daily or weekly calendar artifact for monthly data.

wday.xts

Drop

Daily or weekly calendar artifact for monthly data.

wday.lbl

Drop

Daily or weekly calendar artifact for monthly data.

mday

Drop

Daily or weekly calendar artifact for monthly data.

qday

Drop

Daily or weekly calendar artifact for monthly data.

yday

Drop

Daily or weekly calendar artifact for monthly data.

mweek

Drop

Daily or weekly calendar artifact for monthly data.

week

Drop

Daily or weekly calendar artifact for monthly data.

week.iso

Drop

Daily or weekly calendar artifact for monthly data.

week2

Drop

Daily or weekly calendar artifact for monthly data.

week3

Drop

Daily or weekly calendar artifact for monthly data.

week4

Drop

Daily or weekly calendar artifact for monthly data.

mday7

Drop

Daily or weekly calendar artifact for monthly data.

We now build the actual modeling table from the selected variables and convert ordered factors into plain factors. The target variable sales remains unchanged; the code only prepares the predictor matrix.

# A tibble: 6 × 4

sales index.num year month.lbl

<int> <dbl> <int> <fct>

1 6558 1262304000 2010 enero

2 7481 1264982400 2010 febrero

3 9475 1267401600 2010 marzo

4 9424 1270080000 2010 abril

5 9351 1272672000 2010 mayo

6 10552 1275350400 2010 junio

We split the database into training, validation and test sets following the time ranges in the visualization above. The test set is the most recent data. It remains unavailable during model fitting and tuning.

The split can be read directly from the year column:

Sample

Rule in the code

Use

Training

year < 2021

Fit model parameters.

Validation

year == 2021

Choose hyperparameters.

Test

year == 2022

Evaluate the chosen models.

The validation set is used to choose hyperparameters. The test set is used only after the choices have been made.

Our goal is to forecast the first 10 months of 2022.

2.3 Validation workflow

The following support functions keep the comparison compact. They calculate the same error measures for every model: mean error, root mean squared error, mean absolute error, mean absolute percentage error, and mean percentage error.

For a validation or test sample of size \(n\), with predictions \(\hat{y}_t\), the main metrics are:

The linear regression has no hyperparameters. It is our transparent baseline. If this model works well, that is useful information: sometimes a simple model is enough when trend and seasonality are strong.

Here, \(D_{t,j}\) is a monthly dummy variable: it equals 1 when observation \(t\) belongs to month \(j\), and 0 otherwise. January is the baseline month because it is absorbed by the intercept. The coefficients have a direct interpretation: the trend variables explain long-run movement, and the monthly dummy variables explain seasonality relative to January. The code lm(sales ~ .) means: regress sales on all remaining columns in the modeling table.

The regression tree has a complexity parameter, cp. A smaller value allows a larger tree; a larger value prunes the tree more aggressively. We estimate a small grid and choose the value that minimizes validation RMSE.

A regression tree asks a sequence of yes/no questions about the predictors. For example: is the month December? is the time index above a certain value? After following those questions to a final group, the forecast is the average sales value among the training observations in that group:

\[

\text{tree forecast}

=

\text{average sales in the final group}.

\]

The cp parameter controls the cost of adding more splits. A useful way to read it is as a penalty on tree complexity: larger cp values prune more splits, and smaller cp values allow more splits.

Small cp values allow more regions and can overfit. Large cp values produce simpler trees and can underfit. We choose cp using the validation set. The test set remains reserved for the final evaluation.

The neural network also receives a small manual search. We tune two hyperparameters: size, the number of hidden units, and decay, a penalty that discourages overly large weights. Because the variables have different scales, we standardize the model matrix before fitting.

The neural network uses the same predictors as the linear regression and tree. The difference is the way it combines them. It first standardizes the inputs, then creates a small number of hidden units, and finally combines those hidden units into one forecast. The size hyperparameter controls how many hidden units are used. The decay hyperparameter discourages very large weights, so the fitted rule stays smoother.

Its inputs remain the same explicit features used by the linear regression and the tree. The extra flexibility comes from the hidden layer and the nonlinear activation function.

The support functions below do five mechanical tasks:

Step

What the code does

Why it is important

1

Build the model matrix from the formula.

Convert factors such as month into numeric columns.

2

Standardize the predictors.

Put all inputs on comparable scales.

3

Standardize the target variable.

Help the neural network optimize more smoothly.

4

Fit the network with nnet().

Estimate the weights in the hidden and output layers.

The validation leaderboard summarizes the model selection step. The final forecasting performance is evaluated later with the test set.

For each model family, we choose the setting with the smallest validation RMSE. For the tree, the setting is cp. For the neural network, the setting is the pair (size, decay). Linear regression has no tuning grid, so it enters the leaderboard once.

Validation leaderboard for machine-learning forecasting models.

model

family

setting

me

rmse

mae

mape

mpe

Neural network

Neural network

size = 3, decay = 0

488.20

1138.07

836.93

5.63

2.87

Neural network

Neural network

size = 3, decay = 0.01

792.02

1179.28

954.10

5.94

4.90

Neural network

Neural network

size = 1, decay = 0

1060.20

1195.32

1060.20

6.72

6.72

Neural network

Neural network

size = 1, decay = 0.001

1150.18

1266.56

1150.18

7.30

7.30

Neural network

Neural network

size = 5, decay = 0.01

794.89

1313.70

1087.58

6.97

5.10

Neural network

Neural network

size = 1, decay = 0.01

1236.29

1346.37

1236.29

7.81

7.81

Neural network

Neural network

size = 5, decay = 0

392.53

1370.39

1185.47

7.59

2.22

Neural network

Neural network

size = 3, decay = 0.001

1098.68

1410.56

1149.21

7.10

6.66

Linear regression

Linear regression

selected calendar features

1367.15

1550.66

1372.10

8.40

8.36

Neural network

Neural network

size = 5, decay = 0.001

-92.34

1640.64

1223.46

7.69

-0.80

Regression tree

Regression tree

cp = 0.001

1352.94

1788.57

1382.30

8.78

8.60

Regression tree

Regression tree

cp = 0.005

1445.38

1859.65

1474.74

9.57

9.38

Regression tree

Regression tree

cp = 0.01

1445.38

1859.65

1474.74

9.57

9.38

Regression tree

Regression tree

cp = 0.02

1400.90

1948.70

1400.90

8.83

8.83

Regression tree

Regression tree

cp = 0.05

1400.90

1948.70

1400.90

8.83

8.83

2.4 Test forecasts

Now we refit the chosen model specifications using the training and validation data together, from 2010 through 2021. Then we forecast the 2022 test set. This is a standard practice: validation is used to make modeling decisions, and after that decision is made we can use all pre-test information to estimate the final model.

The final fitted function uses all observations from 2010 through 2021 and the hyperparameters selected in validation. The test forecasts are obtained by applying that final fitted rule to the 2022 rows.

This ordering prevents methodological leakage: the test sales values never enter coefficient estimation, cp selection, neural-network size selection, or neural-network decay selection.

The table below shows the 10-month forecast errors.

Code

ml_errors <-bind_rows(forecast_error_tbl("ML forecast: linear regression", pred_lm_test),forecast_error_tbl("ML forecast: regression tree", pred_tree_test),forecast_error_tbl("ML forecast: neural network", pred_nnet_test))kable(ml_errors,caption ="Detailed test performance for machine-learning forecasting models.",digits =3,row.names =FALSE) %>%kable_styling(latex_options ="HOLD_position")

Detailed test performance for machine-learning forecasting models.

model

date

actual

pred

error

error_pct

ML forecast: linear regression

2022-01-01

11801

12048.17

-247.168

-0.021

ML forecast: linear regression

2022-02-01

13435

12948.50

486.498

0.036

ML forecast: linear regression

2022-03-01

16292

14619.16

1672.844

0.103

ML forecast: linear regression

2022-04-01

15772

14477.24

1294.761

0.082

ML forecast: linear regression

2022-05-01

16714

15601.41

1112.594

0.067

ML forecast: linear regression

2022-06-01

17899

16443.74

1455.261

0.081

ML forecast: linear regression

2022-07-01

15193

14908.49

284.511

0.019

ML forecast: linear regression

2022-08-01

17069

15625.41

1443.594

0.085

ML forecast: linear regression

2022-09-01

16443

15013.07

1429.927

0.087

ML forecast: linear regression

2022-10-01

15585

15577.07

7.927

0.001

ML forecast: regression tree

2022-01-01

11801

11084.83

716.167

0.061

ML forecast: regression tree

2022-02-01

13435

11084.83

2350.167

0.175

ML forecast: regression tree

2022-03-01

16292

16173.25

118.750

0.007

ML forecast: regression tree

2022-04-01

15772

16173.25

-401.250

-0.025

ML forecast: regression tree

2022-05-01

16714

16173.25

540.750

0.032

ML forecast: regression tree

2022-06-01

17899

17100.25

798.750

0.045

ML forecast: regression tree

2022-07-01

15193

16173.25

-980.250

-0.065

ML forecast: regression tree

2022-08-01

17069

16173.25

895.750

0.052

ML forecast: regression tree

2022-09-01

16443

16173.25

269.750

0.016

ML forecast: regression tree

2022-10-01

15585

16173.25

-588.250

-0.038

ML forecast: neural network

2022-01-01

11801

11289.04

511.964

0.043

ML forecast: neural network

2022-02-01

13435

12925.93

509.073

0.038

ML forecast: neural network

2022-03-01

16292

16326.27

-34.270

-0.002

ML forecast: neural network

2022-04-01

15772

16363.52

-591.524

-0.038

ML forecast: neural network

2022-05-01

16714

16184.65

529.346

0.032

ML forecast: neural network

2022-06-01

17899

17725.16

173.840

0.010

ML forecast: neural network

2022-07-01

15193

17594.15

-2401.155

-0.158

ML forecast: neural network

2022-08-01

17069

16734.07

334.930

0.020

ML forecast: neural network

2022-09-01

16443

17511.51

-1068.509

-0.065

ML forecast: neural network

2022-10-01

15585

16931.42

-1346.422

-0.086

The same information is clearer in a plot. The black line is the actual series. The colored lines are the machine-learning forecasts for the 2022 test period.

Test summary for machine-learning forecasting models.

model

me

rmse

mae

mape

mpe

ML forecast: neural network

-338.27

1000.75

750.10

4.91

-2.07

ML forecast: regression tree

372.03

965.60

765.98

5.16

2.61

ML forecast: linear regression

894.07

1110.76

943.51

5.81

5.39

A model can rank first by MAPE and rank differently by another metric. For that reason, it is useful to inspect multiple errors. RMSE penalizes large mistakes more heavily, while MAPE is easy to read as an average percentage error.

The table compares fitted forecasting functions under a common experimental design. Every model saw the same training data, the same validation data, the same predictors, and the same test months. A lower MAPE means that this particular fitted function was closer to the realized 2022 sales over this holdout period.

In the current render, the machine-learning neural network forecast is the best of the three supervised forecasting models, with MAPE around 4.91. The regression tree follows with MAPE around 5.16, and the linear regression has MAPE around 5.81. The differences are modest, so the interpretation should focus on the pattern: calendar and trend predictors carry useful information, and a small nonlinear model extracts a little more from those predictors in this test window.

We can also show the best individual point forecast for each model.

Code

point_forecast_ml <- ml_errors %>%group_by(model) %>%slice_min(abs(error_pct), n =1, with_ties =FALSE) %>%ungroup() %>%select(model, date, actual, pred, error, error_pct)kable(point_forecast_ml,caption ="Best point forecast for each machine-learning forecasting model.",digits =4,row.names =FALSE) %>%kable_styling(latex_options ="HOLD_position")

Best point forecast for each machine-learning forecasting model.

model

date

actual

pred

error

error_pct

ML forecast: linear regression

2022-10-01

15585

15577.07

7.9273

0.0005

ML forecast: neural network

2022-03-01

16292

16326.27

-34.2696

-0.0021

ML forecast: regression tree

2022-03-01

16292

16173.25

118.7500

0.0073

Choosing a model according to one specific point forecast would be fragile. Even so, it is useful to see where each model was most accurate.

# A tibble: 10 × 2

.model MAPE

<chr> <dbl>

1 fpp3: ETS(M,A,M) 3.77

2 fpp3: seasonal naïve 3.89

3 fpp3: ARIMA(4,1,1)(0,1,1)[12] 4.40

4 ML forecast: neural network 4.91

5 ML forecast: regression tree 5.16

6 ML forecast: linear regression 5.81

7 fpp3: NNAR(15,1,8)[12] 6.02

8 fpp3: naïve 18.1

9 fpp3: drift 20.9

10 fpp3: mean 23.5

2.5 ARIMA comparison

As in the original Matt Dancho example, we include a different ARIMA workflow using the forecast package and the auto.arima() function. This benchmark belongs to the classical time-series family and answers a different modeling question. The machine-learning forecasting models above estimate \(\text{sales}=f(\text{trend and month variables})+\text{error}\) using trend and calendar predictors. ARIMA models the dependence of the series on its own past.

The auto.arima() function automates the selection of the ARIMA orders. The automation is a statistical search over candidate values of \((p,d,q)(P,D,Q)_{12}\), followed by parameter estimation and information-criterion comparison.

The order notation is read as follows:

Order

Meaning

\(p\)

Number of recent lagged values used by the autoregressive part.

\(d\)

Number of ordinary differences.

\(q\)

Number of recent forecast errors used by the moving-average part.

\(P\)

Number of seasonal lagged values.

\(D\)

Number of seasonal differences.

\(Q\)

Number of seasonal forecast errors.

12

Monthly seasonal cycle.

Prepare the data.

The tk_ts() function coerces time series objects and tibbles with date or date-time columns to ts.

We can use the auto.arima() function from the forecast package to model the time series. The function tests a set of specifications and selects the one that performs best according to its internal statistical criterion.

The printed output is the selected mathematical specification. After this line, we are no longer speaking abstractly about auto.arima(); we are speaking about the particular ARIMA equation selected for this data set and this training window.

The sw_tidy() function returns the model coefficients in a tibble.

The sw_augment() function helps with model evaluation. We get the .actual, .fitted and .resid columns, which are useful in evaluating the model against the training data.

If the ARIMA model has captured the predictable autocorrelation, these residuals should have no obvious remaining time pattern. This is the same audit logic used in the fpp3 chapter.

Make a forecast using the forecast() function.

Code

fcast_arima <-forecast(fit_arima, h =10)fcast_arima

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

Jan 2022 12958.70 12262.28 13655.11 11893.62 14023.77

Feb 2022 13978.00 13237.17 14718.84 12844.99 15111.01

Mar 2022 16341.49 15596.23 17086.75 15201.71 17481.27

Apr 2022 16704.29 15930.63 17477.96 15521.07 17887.52

May 2022 17095.58 16313.50 17877.65 15899.50 18291.66

Jun 2022 18163.88 17360.62 18967.14 16935.40 19392.36

Jul 2022 16011.91 15197.81 16826.02 14766.85 17256.98

Aug 2022 16996.29 16164.63 17827.95 15724.38 18268.21

Sep 2022 16153.24 15309.50 16996.97 14862.86 17443.61

Oct 2022 16437.31 15578.01 17296.60 15123.13 17751.48

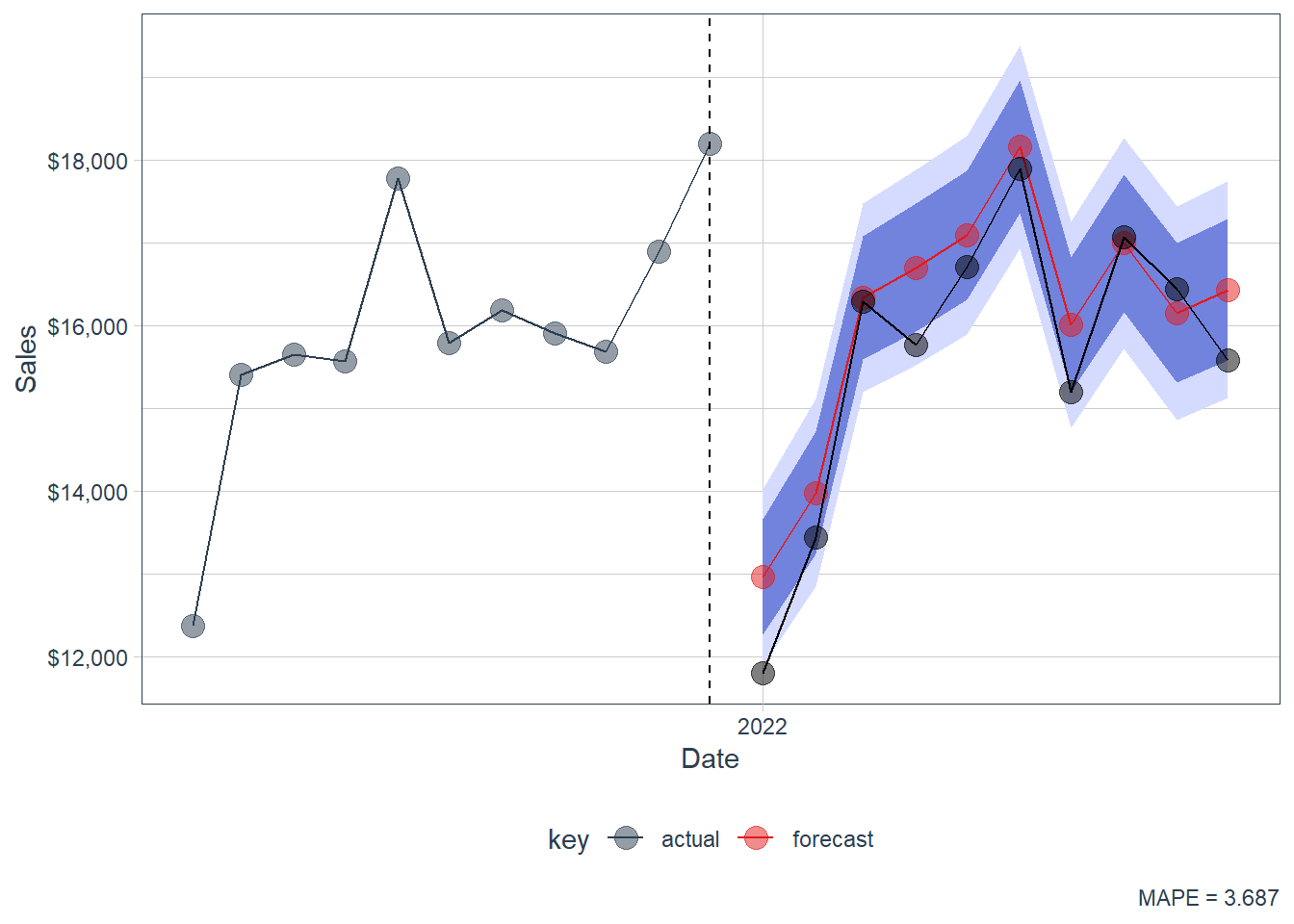

Notice that we have the entire forecast in a tibble. We can now more easily visualize the forecast.

Code

fcast_tbl %>%filter(index >as.Date("2021-01-01")) %>%ggplot(aes(x = index, y = sales, color = key)) +geom_ribbon(aes(ymin = lo.95, ymax = hi.95),fill ="#D5DBFF", color =NA, linewidth =0) +geom_ribbon(aes(ymin = lo.80, ymax = hi.80, fill = key),fill ="#596DD5", color =NA, linewidth =0, alpha =0.8) +geom_line() +geom_point(size =4, alpha =0.5) +geom_line(aes(x = date, y = sales), color ="black",data = actuals_tbl) +geom_point(aes(x = date, y = sales), color ="black", size =4,alpha =0.5, data = actuals_tbl) +geom_vline(xintercept =as.numeric(as.Date("2021-12-01")),linetype =2) +labs(x ="Date", y ="Sales",caption =paste("MAPE =",round(100*mean(abs(error_tbl_arima$error_pct)), 5))) +scale_x_date(date_breaks ="1 year", date_labels ="%Y") +scale_color_tq() +scale_fill_tq() +theme_tq() +scale_y_continuous(labels = scales::dollar)

Figure 2.5: Forecast. forecast::auto.arima.

The resulting forecast serves as a benchmark.

In this render, forecast::auto.arima has MAPE around 3.69. This makes it a strong benchmark: it beats the supervised machine-learning forecasts in this specific holdout period and lands close to the best models from the first chapter. That result is pedagogically useful because it shows that classical time-series structure can remain highly competitive when the series has strong trend, seasonality and autocorrelation.

2.6 Summary of all results

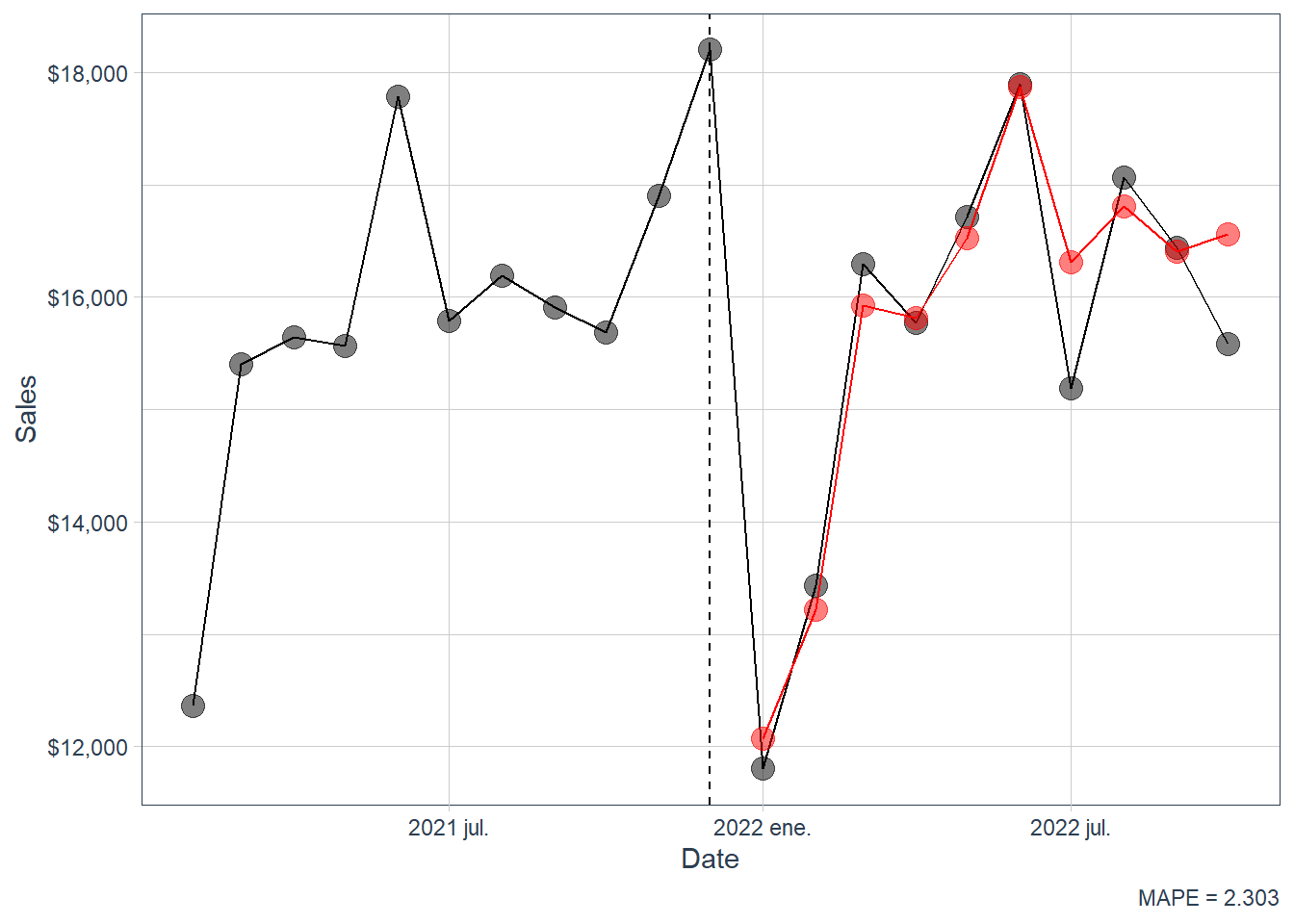

An interesting question is: What happens to the accuracy when you average the predictions of different methods? This question makes sense because model choice is often uncertain in forecasting. Taking the average can reduce extreme results, although it can also be harder to interpret because the final forecast comes from several techniques.

If there are \(M\) forecast models, the average forecast is

This ensemble rule is applied after the individual forecasts already exist. Its appeal is that different models can make different errors, so averaging may reduce model-specific noise. Its cost is interpretability: the final number no longer comes from one clear structural assumption.

In order to calculate the average forecast we need to load the forecasts from the previous section. In particular, we include the seasonal naive, NNAR(15,1,8)[12], ETS(M,A,M), and ARIMA(4,1,1)(0,1,1)[12]. We exclude the naive, drift and mean forecasts from this average.

Code

fpp3_fc <-readRDS("fpp3_fc.rds")

We add the machine-learning forecasts and the forecast::auto.arima forecast into the fpp3 forecast table.

# A tibble: 12 × 2

.model MAPE

<chr> <dbl>

1 Average forecast 2.30

2 forecast::auto.arima 3.69

3 fpp3: ETS(M,A,M) 3.77

4 fpp3: seasonal naïve 3.89

5 fpp3: ARIMA(4,1,1)(0,1,1)[12] 4.40

6 ML forecast: neural network 4.91

7 ML forecast: regression tree 5.16

8 ML forecast: linear regression 5.81

9 fpp3: NNAR(15,1,8)[12] 6.02

10 fpp3: naïve 18.1

11 fpp3: drift 20.9

12 fpp3: mean 23.5

The ranking is local to this data set and this holdout period. The main lesson is that a transparent workflow lets us see where the forecast comes from, how the model was selected, how long it takes to render, and how it performs when confronted with truly unseen data.

The average forecast is the best row in this render, with MAPE around 2.37. That result has a clear interpretation: the individual models make different errors, and averaging reduces part of that model-specific noise. The cost is interpretability because the final number comes from several forecasting rules. For teaching purposes, this is a valuable ending point: students can see that the best empirical forecast may come from combining models, while the individual models remain necessary for understanding what information the forecast is using.