This chapter studies asset pricing as an applied econometric problem. The goal is to connect factor-model logic, mathematical notation, R code, and empirical interpretation in one continuous workflow. The chapter starts with the economic question, builds the data and test assets, estimates time-series regressions, uses cross-sectional regressions to price factor exposures, and then rewrites the same pricing problem with stochastic discount factor GMM. The emphasis is on making each equation operational: what it means, why it is estimated, how it appears in the code, and how its results should be read.

4.1 Asset pricing as an econometric problem

Asset pricing econometrics asks a precise empirical question: can a small set of systematic risk factors explain why some assets or portfolios earn higher average excess returns than others? The answer is estimated from data, but the data work has to stay connected to the economic model. A coefficient is useful only when the reader can say what it measures, how the code estimated it, and what its value implies for the model.

This chapter follows the regression-based logic used in empirical asset pricing (Cochrane 2005). The same idea appears in three connected forms. Time-series regressions estimate each asset’s exposure to common factors. Cross-sectional regressions ask whether those exposures explain average excess returns across test assets. Stochastic discount factor moments express the same restriction as a pricing condition: after discounting by the model, excess returns should have zero remaining average payoff.

The empirical examples use one mutual fund and the 25 Fama-French size-value portfolios as test assets. The risk factors are the market excess return, size, value, momentum, profitability, and investment factors from the Kenneth French Data Library. The chapter downloads the data during execution and fixes the sample end at 2020-12-31 so the empirical window is reproducible.

The central object is an excess return:

\[

R_{i,t}^e

=

R_{i,t}-R_{f,t},

\]

where \(R_{i,t}\) is the return on asset \(i\) in month \(t\) and \(R_{f,t}\) is the risk-free return. A factor model explains \(R_{i,t}^e\) using common sources of variation. The CAPM uses one factor, the market excess return (Sharpe 1964; Lintner 1965; Mossin 1966). The Fama-French three-factor model adds size and value factors (Fama and French 1992, 1993). Momentum and the five-factor model extend the factor set (Carhart 1997; Fama and French 2015).

The chapter should be read as a sequence of empirical questions. The data tables verify samples, dates, and units. The factor figures show what the explanatory portfolios look like before they become regressors. The time-series regressions translate co-movement into alphas and betas. The cross-sectional regressions then ask whether those estimated exposures, or equivalent return-factor moments, explain average excess returns across the 25 portfolios. The final diagnostic reads the remaining pricing errors by size and value characteristics. Each table and figure therefore has a specific role: audit the data, describe the factors, estimate exposures, diagnose the first pass, test the asset-pricing restriction, or interpret what the model leaves unexplained.

The main vocabulary is:

Concept

Symbol

Reading in the chapter

Test asset

\(i\)

An asset or portfolio whose average excess return the model tries to explain.

Excess return

\(R_{i,t}^e\)

The asset return after subtracting the risk-free rate.

Factor

\(f_{j,t}\)

A common return series used to represent a source of systematic risk.

Beta

\(\beta_{i,j}\)

The exposure of asset \(i\) to factor \(j\), estimated from a time-series regression.

Alpha

\(\alpha_i\)

The average excess return left over after the factor exposures are used.

Price of risk

\(\lambda_j\)

The cross-sectional reward attached to one unit of exposure to factor \(j\).

Pricing error

\(\eta_i\) or \(\alpha_i\)

The part of average return that the model leaves unexplained in the relevant test.

Stochastic discount factor

\(m_t\)

A random discount factor that prices excess returns through moment restrictions.

The chapter uses these concepts in a fixed order. First define excess returns. Then estimate betas and alphas from time-series regressions. Then estimate prices of risk from a cross-section of average returns. Finally inspect pricing errors to see where the model still struggles.

This ordering is useful because asset pricing notation can compress several ideas into one equation. The economic question, the statistical object, and the code object should be separated before they are joined again:

Question

Mathematical object

Code object

Interpretation

What is being explained?

\(\bar{R}_i^e\)

ERe_percent

Average excess return of each test asset.

What is the proposed source of explanation?

\(\mathbf{f}_t\)

Mkt_RF, SMB3, HML, Mom, RMW, CMA

Common factor returns.

How exposed is each asset?

\(\boldsymbol{\beta}_i\)

Time-series lm() coefficients

Sensitivity of asset returns to factor returns.

What does the model leave behind?

\(\alpha_i\) or \(\eta_i\)

Intercepts and fitted-value gaps

Pricing errors.

How is risk priced across assets?

\(\boldsymbol{\lambda}\)

Cross-sectional lm() coefficients

Reward attached to factor exposure.

How does the SDF view express the same restriction?

\(E(m_tR_{i,t}^e)=0\)

Return-factor moments

Discounted excess returns should average to zero.

The word “pricing” should also be read carefully. In this chapter, pricing means testing whether a model can explain average excess returns. For an excess return, the initial cost is zero because the investment is financed at the risk-free rate. A correct model should assign zero value to that excess-return payoff after applying the relevant risk adjustment. That is why alphas, fitted-value gaps, and SDF moments all become ways of measuring pricing errors.

4.2 Data, downloads, and sample construction

The factor data and the 25 size-value portfolio returns are downloaded from the Kenneth French Data Library (French 2026). The individual test asset example uses the Fidelity Contrafund ticker FCNTX downloaded with tidyquant. All returns are converted from percentages to decimal units during estimation. Percent units are used only when a table or graph is meant for interpretation.

The code keeps the data in decimal form. For example, a monthly return of 0.01 means one percent. This convention prevents unit mistakes when returns are added, multiplied, or used in regressions.

The first data audit shows the opening and closing observations of the main data objects. These checks verify dates, decimal units, and column names before any model is estimated.

Code

factor_windows |>mutate(across(c(start, end), as.character)) |>kable(caption ="Sample windows of the downloaded Fama-French data files.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Sample windows of the downloaded Fama-French data files.

source

start

end

months

Fama-French 3 factors

1926-07-31

2020-12-31

1134

Momentum factor

1927-01-31

2020-12-31

1128

Fama-French 5 factors

1963-07-31

2020-12-31

690

25 size-value portfolios

1926-07-31

2020-12-31

1134

Code

first_last_rows(ff3_momentum) |>select(date, Mkt_RF, SMB3, HML, Mom, RF) |>kable(caption ="First and last observations of the joined FF3 and momentum sample.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last observations of the joined FF3 and momentum sample.

date

Mkt_RF

SMB3

HML

Mom

RF

1927-01-31

-0.0005

-0.0032

0.0458

0.0057

0.0025

1927-02-28

0.0417

0.0007

0.0272

-0.0151

0.0026

1927-03-31

0.0014

-0.0177

-0.0238

0.0352

0.0030

2020-10-31

-0.0208

0.0434

0.0425

-0.0310

0.0001

2020-11-30

0.1245

0.0581

0.0209

-0.1260

0.0001

2020-12-31

0.0463

0.0501

-0.0168

-0.0227

0.0001

Code

first_last_rows(ff5) |>kable(caption ="First and last observations of the Fama-French five-factor data.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last observations of the Fama-French five-factor data.

date

Mkt_RF

SMB

HML

RMW

CMA

RF

1963-07-31

-0.0039

-0.0048

-0.0081

0.0064

-0.0115

0.0027

1963-08-31

0.0508

-0.0080

0.0170

0.0040

-0.0038

0.0025

1963-09-30

-0.0157

-0.0043

0.0000

-0.0078

0.0015

0.0027

2020-10-31

-0.0208

0.0467

0.0425

-0.0077

-0.0057

0.0001

2020-11-30

0.1244

0.0712

0.0209

-0.0225

0.0128

0.0001

2020-12-31

0.0463

0.0493

-0.0168

-0.0197

-0.0006

0.0001

Code

first_last_rows(portfolios_25) |>select(date, `SMALL LoBM`, `SMALL HiBM`, `BIG LoBM`, `BIG HiBM`) |>kable(caption ="First and last observations of selected 25-portfolio corner returns.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last observations of selected 25-portfolio corner returns.

date

SMALL LoBM

SMALL HiBM

BIG LoBM

BIG HiBM

1926-07-31

0.058276

0.019583

0.033248

0.005623

1926-08-31

-0.020206

0.085104

0.010169

0.077576

1926-09-30

-0.048291

0.008586

-0.012951

-0.024284

2020-10-31

-0.026753

0.012595

-0.045743

0.009898

2020-11-30

0.257600

0.245286

0.107281

0.219976

2020-12-31

0.125156

0.074510

0.053002

0.080558

These tables are a data audit. The window table shows which raw files can be used over which dates. The joined FF3-momentum table then shows the actual intersection used when the model includes momentum, so every displayed column has an observed value for the same month. The first and last rows also confirm that the factor files and the portfolio file are monthly series, expressed in decimal units, and aligned on month-end dates. The selected corner portfolios already hint at the empirical structure used later: small growth, small value, big growth, and big value are the extreme cells of the size-value grid.

4.3 Excess returns and factor notation

The notation in this chapter has three indices in the background. The subscript \(i\) identifies the asset or portfolio. The subscript \(t\) identifies the month. The subscript attached to a beta, such as \(M\), \(S\), or \(H\), identifies the factor. For example, \(\beta_{i,H}\) is the value-factor exposure of asset \(i\), estimated from monthly observations over time.

Each model has an observed left-hand side and estimated right-hand-side coefficients. The observed variable is always an excess return, \(R_{i,t}^e\). The factors are also observed return series. The unknown objects are the intercept and the betas. The regression estimates those unknowns by choosing the line, or plane, that best summarizes the historical relation between the asset’s excess return and the factor returns.

The CAPM time-series regression for asset \(i\) is

where \(MKT_t\) is the market excess return. The intercept \(\alpha_i\) is the average excess return that remains after controlling for market exposure. In a well-specified asset pricing model, alphas should be economically small.

The CAPM is therefore a one-factor claim. It says that market exposure is the relevant systematic risk for expected returns. The regression version asks how strongly each asset moves with the market. The asset-pricing version asks whether that market exposure is enough to account for the asset’s average excess return.

Value factor: high book-to-market minus low book-to-market.

\(MOM_t\)

Momentum factor: recent winners minus recent losers.

\(RMW_t\)

Profitability factor: robust minus weak profitability.

\(CMA_t\)

Investment factor: conservative minus aggressive investment.

Each factor is constructed as a portfolio return. This point is central for the interpretation of betas. A positive loading on \(SMB_t\) means that the asset tends to behave like the small-minus-big portfolio. A positive loading on \(HML_t\) means that the asset tends to behave like the high-book-to-market minus low-book-to-market portfolio. The factor return series already encode the small and value portfolio strategies used in the regression.

The five-factor model replaces the three-factor specification with

The code names these variables as Mkt_RF, SMB3, HML, Mom, SMB5, RMW, and CMA. The distinction between SMB3 and SMB5 is intentional: the size factor in the three-factor data and the size factor in the five-factor data are constructed from different portfolio sorts.

The notation and the code follow the same structure. In the equation, \(R_{i,t}^e\) is the dependent variable and the factors are regressors. In R, Re is the dependent variable and the factor columns appear on the right side of the formula. For example, Re ~ Mkt_RF + SMB3 + HML is the code version of the Fama-French three-factor regression.

4.4 Factor portfolios through time

Before estimating asset pricing regressions, it is useful to inspect the factor returns themselves. The next calculation computes annualized return, annualized volatility, and a simple return-to-risk ratio.

This descriptive step has a practical purpose. A factor is a return series, so it can be read like a portfolio before it is used as a regressor. The annualized table summarizes reward and risk. The cumulative plots show the path by which those rewards are earned over time. The density plots show the distribution of monthly outcomes. The risk-return plots then compress those summaries into a single visual comparison. Together, these checks tell the reader what economic objects enter the regressions.

Annualized performance of the three Fama-French factors and momentum.

factor

months

annualized_return

annualized_volatility

return_per_unit_risk

SMB3

1128

0.0189

0.1097

0.1719

HML

1128

0.0330

0.1220

0.2708

Mkt_RF

1128

0.0662

0.1858

0.3561

Mom

1128

0.0623

0.1637

0.3802

The annualized table turns each factor into an object that can be compared like a portfolio. The return column shows the long-run reward, the volatility column shows the risk of the factor strategy, and the return-per-risk column gives a compact scale for ranking factor performance before looking at individual assets.

The three-factor file is inspected first by itself. This mirrors the original workflow: read the Fama-French factors, check their time path, and then add momentum as an extension.

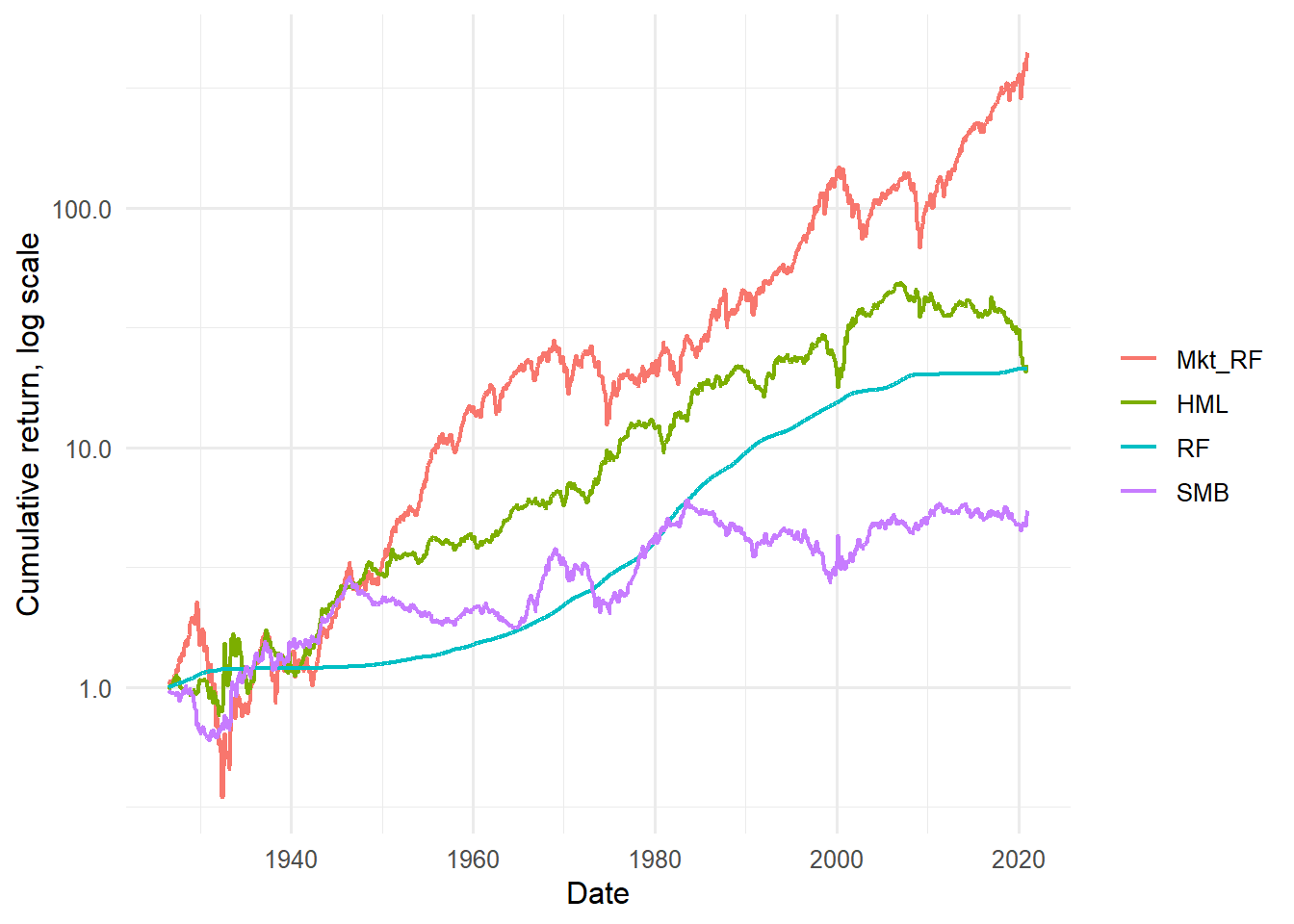

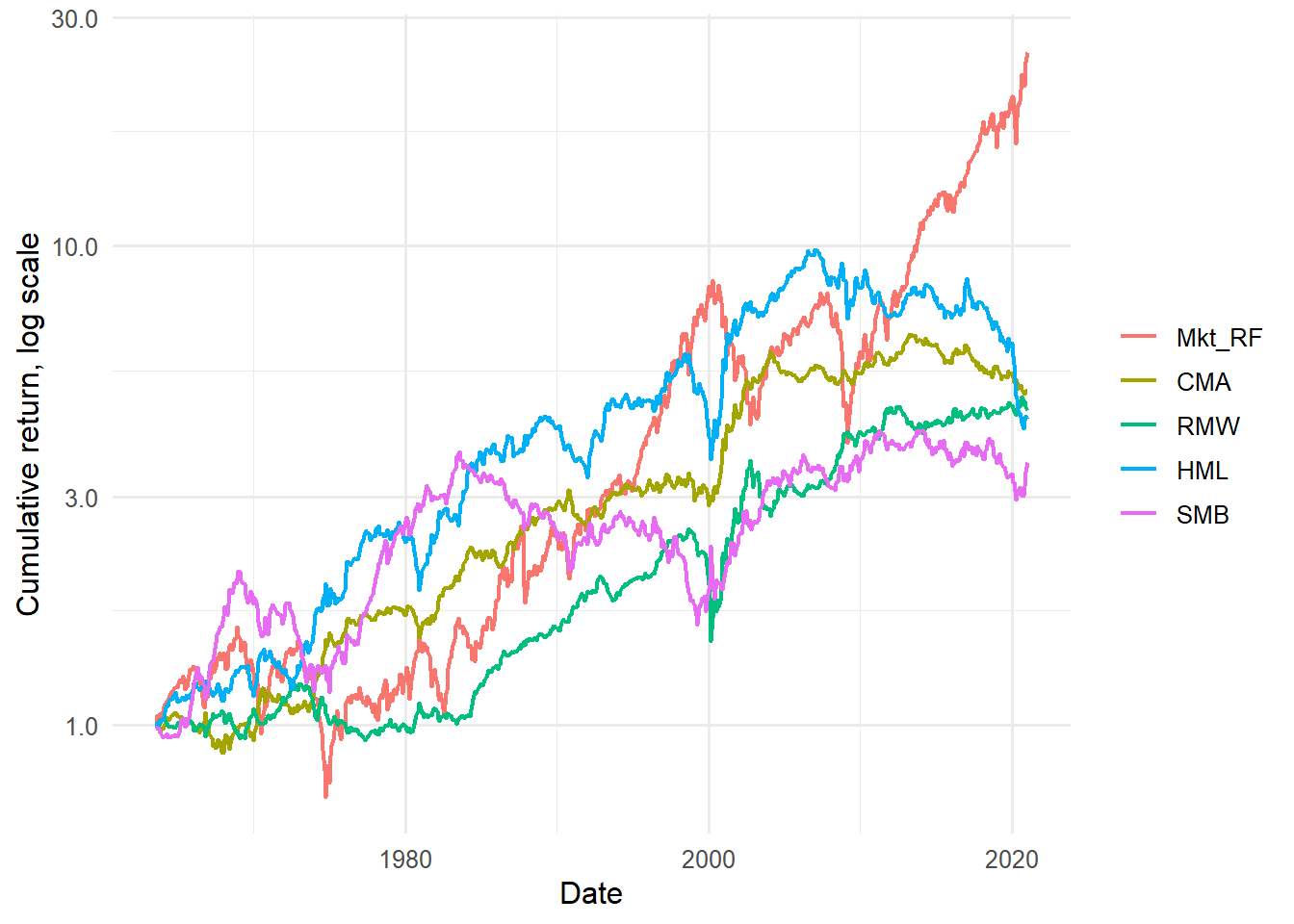

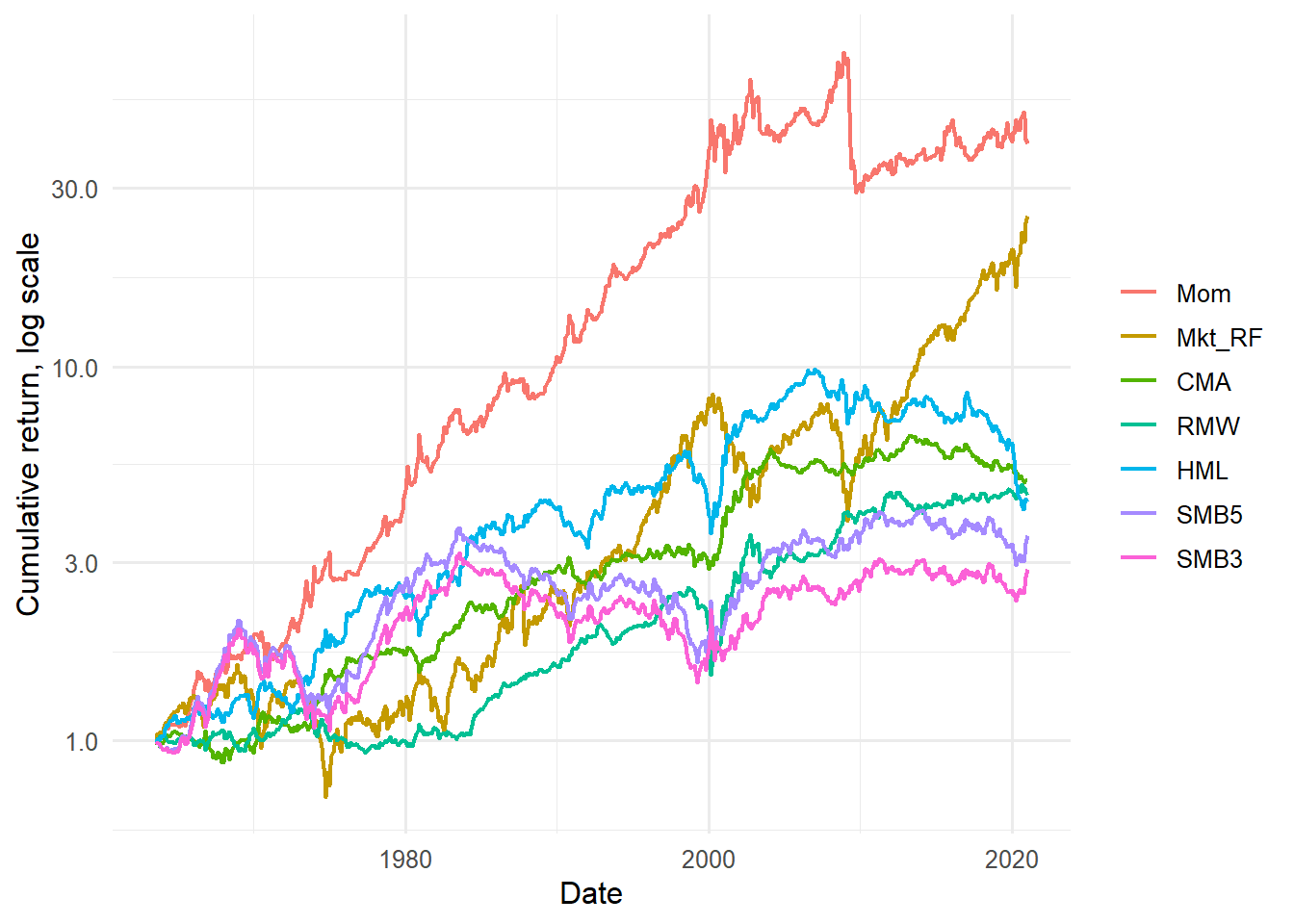

Figure 4.1: Cumulative returns of the Fama-French three factors.

The cumulative-return plot emphasizes that factor premia are earned through time, with long expansions and reversals. A factor can have a positive average return and still experience long drawdowns, so the time path is part of the economic story.

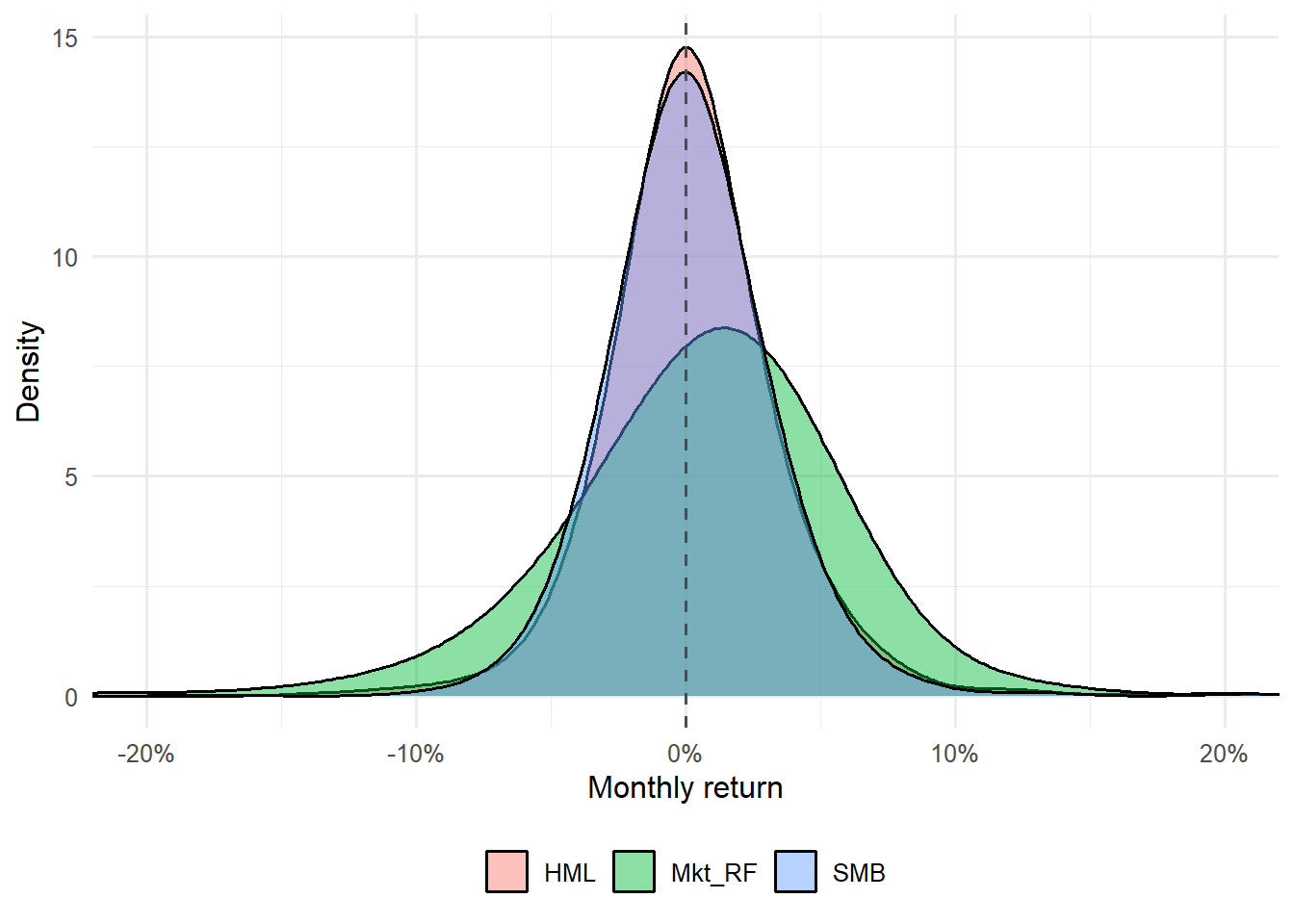

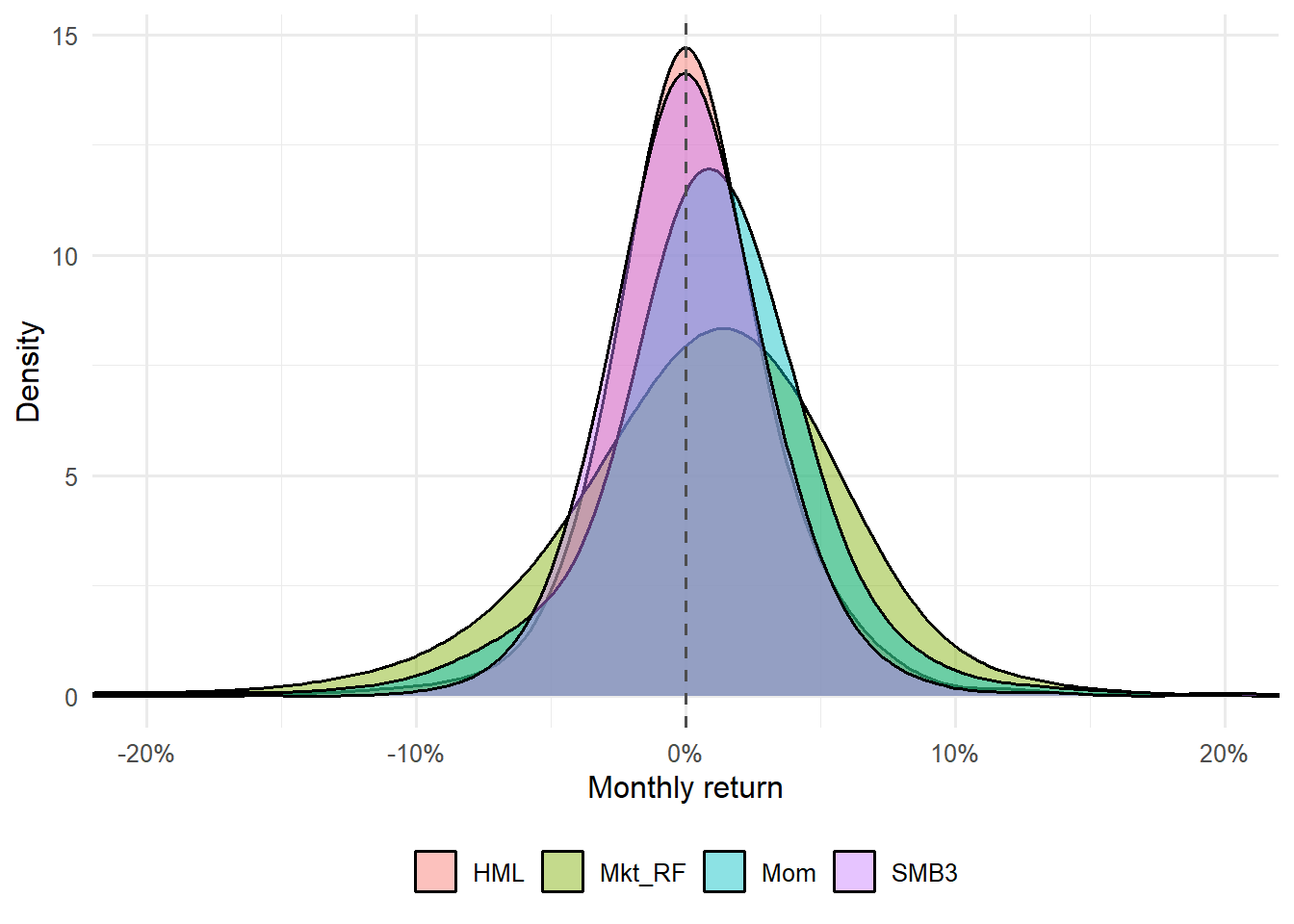

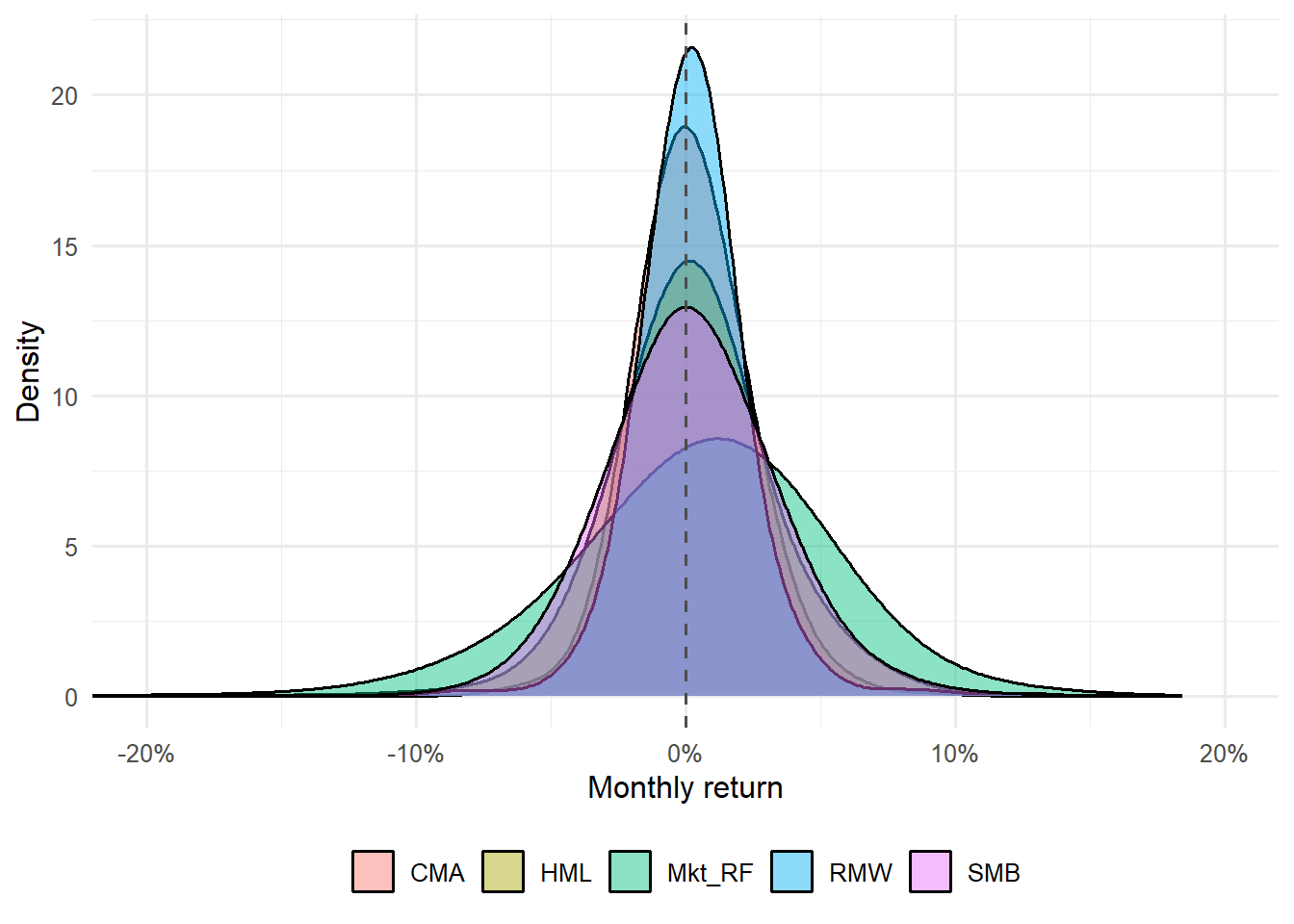

Figure 4.2: Distribution of monthly returns for the Fama-French three factors.

The density plot complements the cumulative plot. It shows where monthly returns are concentrated and how far negative or positive observations can extend. This helps students read factor performance as both a distribution of monthly outcomes and an annualized average.

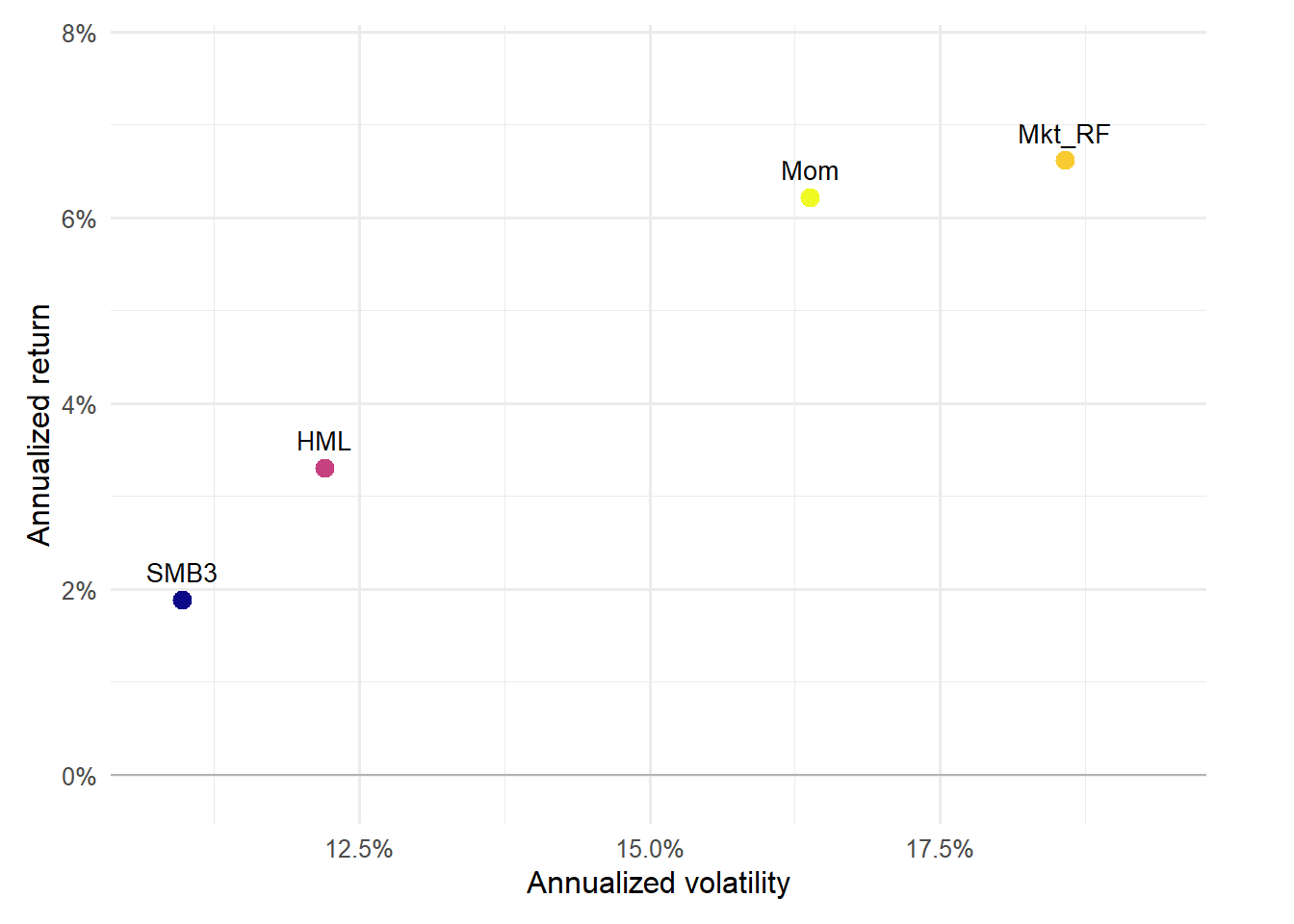

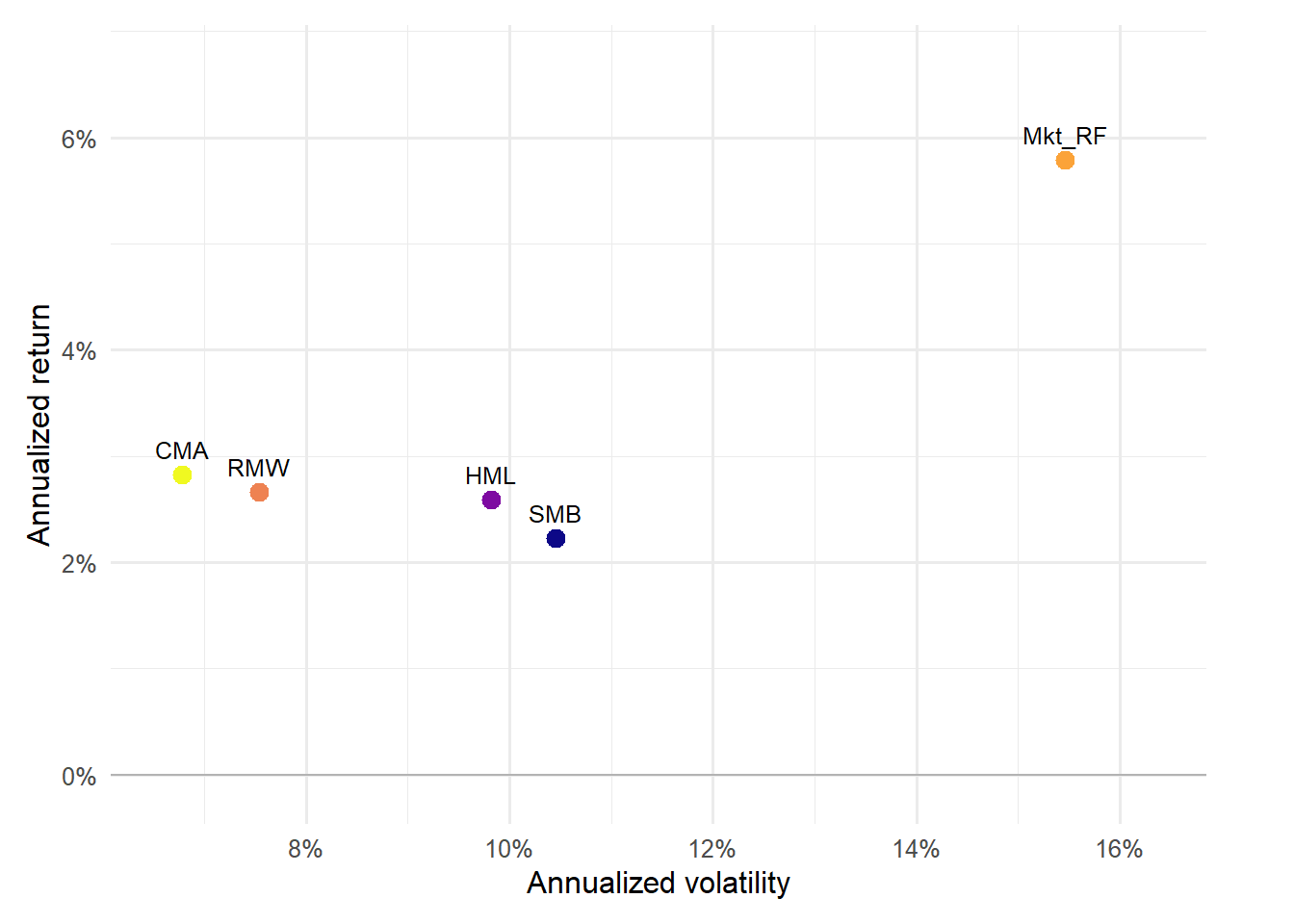

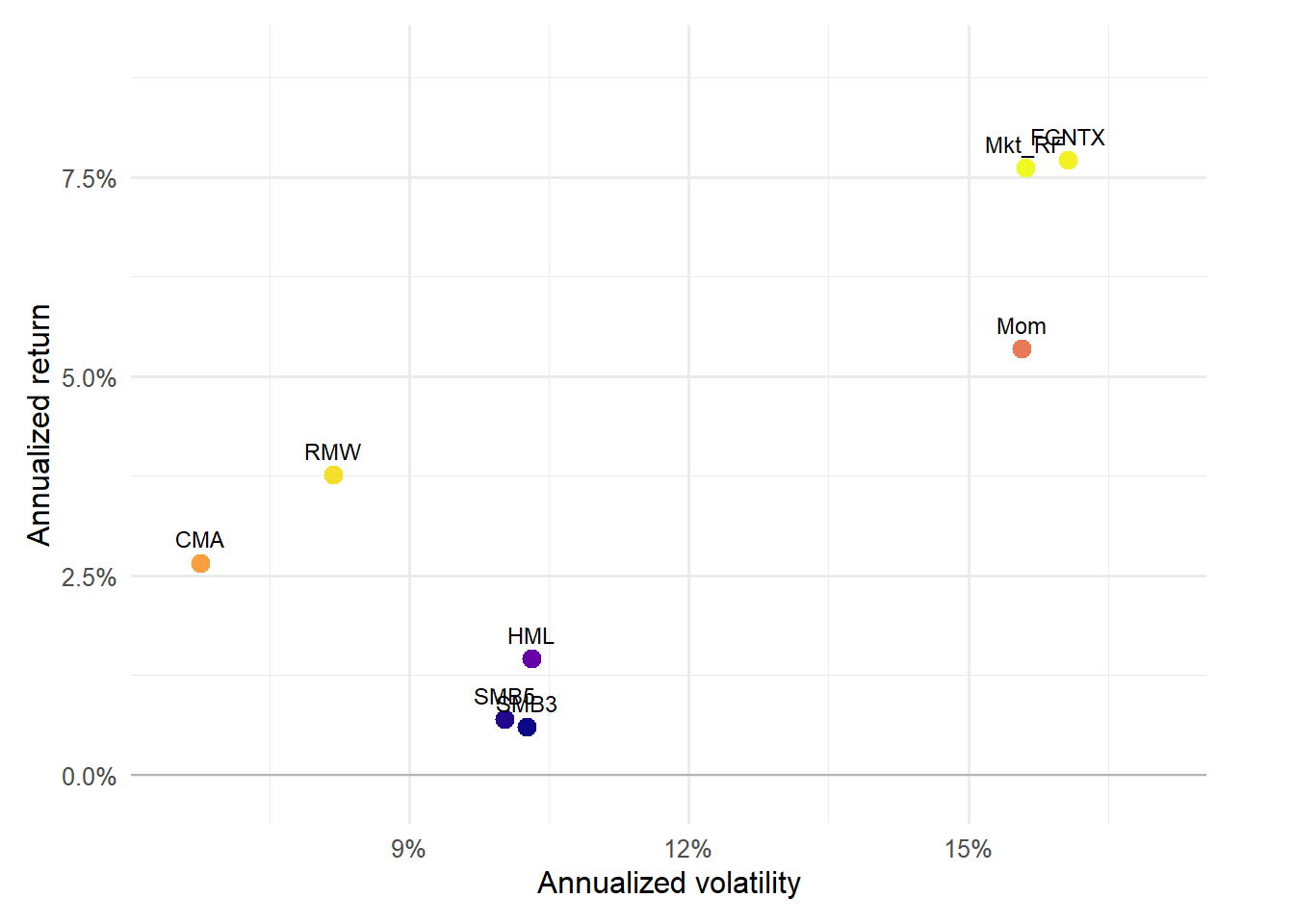

Figure 4.3: Risk-return profile of the factor portfolios.

The risk-return profile compresses the table into one visual comparison. Points higher on the vertical axis have larger annualized returns, while points farther right have higher annualized volatility. Labels make clear which factor drives each position, so the graph can be read as a map of factor rewards and risks.

Cumulative factor returns show that factors are portfolios through time. The line for each factor is the wealth path from investing one dollar in that long-short factor portfolio:

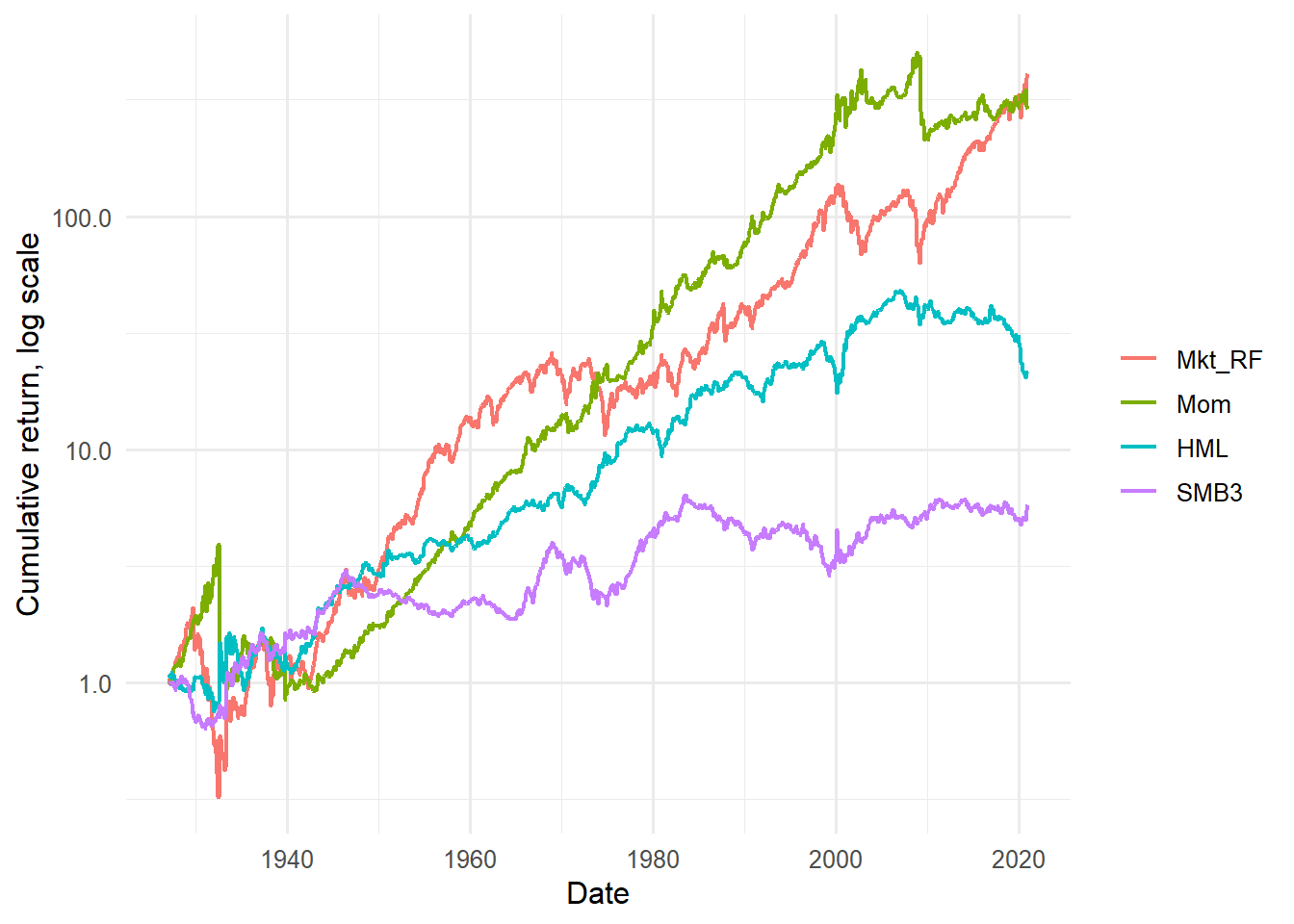

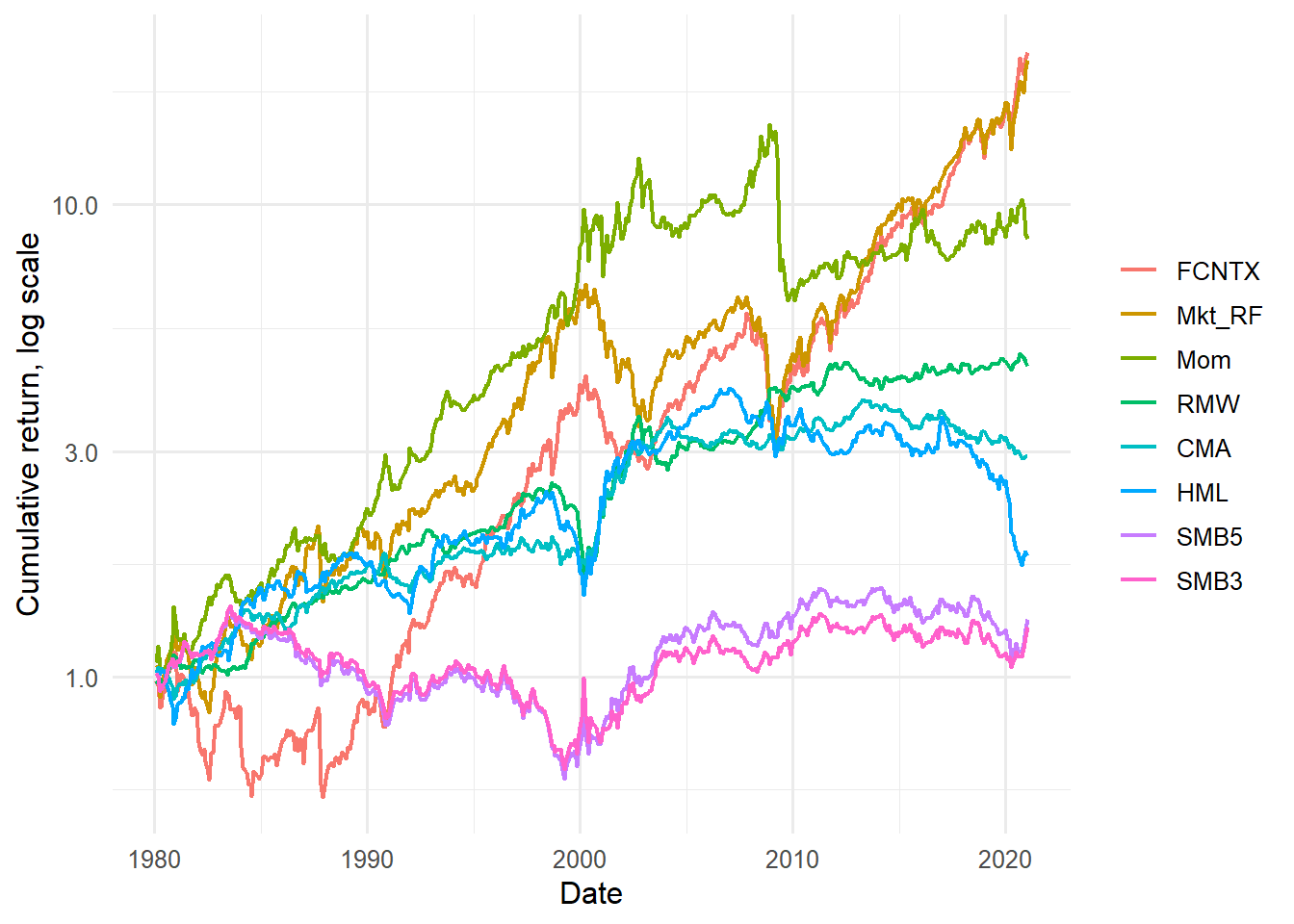

Figure 4.4: Cumulative returns of Fama-French factors and momentum.

Adding momentum changes the visual comparison because the set of candidate factor portfolios is now broader. The purpose of the figure is to show how the market, size, value, and momentum factor histories differ before any asset pricing regression uses them as explanatory variables.

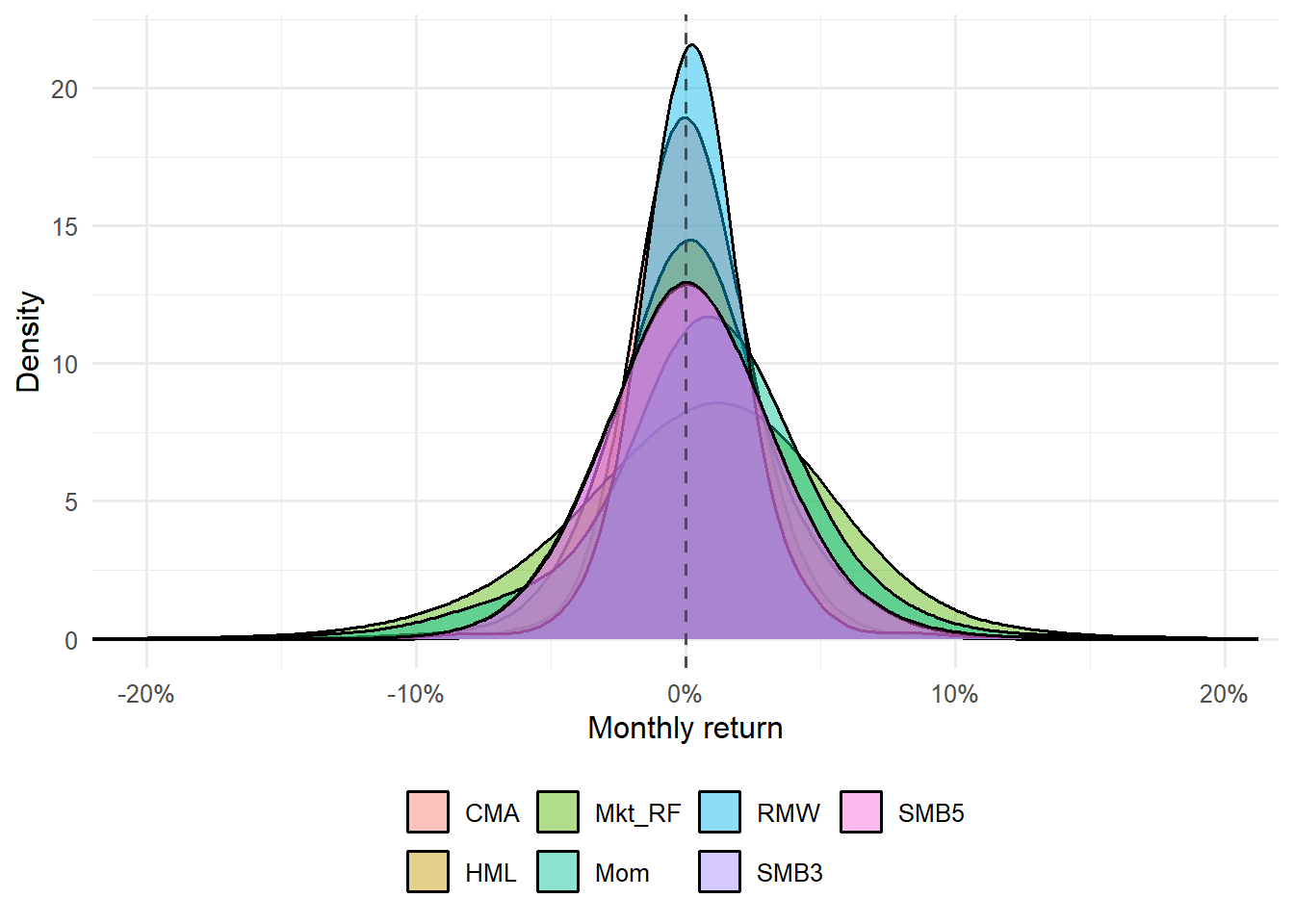

The distribution of monthly factor returns is another diagnostic. Momentum and value can have long episodes of strong performance and sharp reversals, so a factor’s average return should always be read together with its volatility and tail behavior.

Figure 4.5: Distribution of monthly factor returns.

The monthly distributions also show why factor regressions can be sensitive to large episodes. A factor with a similar average return can have a different tail profile, and that affects how individual assets load on it in a regression.

The same workflow can be applied to the five-factor data. The shorter sample starts in 1963, because the profitability and investment factors are available from that point in the downloaded file.

Code

ff5_perf <-annualized_performance(ff5, c("Mkt_RF", "SMB", "HML", "RMW", "CMA"))ff5_perf |>mutate(across(c(annualized_return, annualized_volatility, return_per_unit_risk), ~round(.x, 4))) |>kable(caption ="Annualized performance of the Fama-French five factors.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Annualized performance of the Fama-French five factors.

factor

months

annualized_return

annualized_volatility

return_per_unit_risk

SMB

690

0.0222

0.1046

0.2128

HML

690

0.0259

0.0982

0.2636

RMW

690

0.0266

0.0754

0.3534

Mkt_RF

690

0.0578

0.1547

0.3740

CMA

690

0.0283

0.0678

0.4169

The five-factor table prepares the reader for a different factor set and a shorter historical window. Profitability and investment are interpreted as additional dimensions of systematic risk, so their return and volatility should be inspected before they are added to any regression.

The workflow also inspects the five-factor sample and the combined factor set with momentum. The samples differ: the five-factor data start later, and the SMB factor in the five-factor file is a different constructed series from the SMB factor in the three-factor file. The chapter keeps the variable names SMB3 and SMB5 to make that distinction visible in the code.

Annualized performance of the combined factor set.

factor

months

annualized_return

annualized_volatility

return_per_unit_risk

SMB3

690

0.0186

0.1048

0.1772

SMB5

690

0.0222

0.1046

0.2128

HML

690

0.0259

0.0982

0.2636

RMW

690

0.0266

0.0754

0.3534

Mkt_RF

690

0.0578

0.1547

0.3740

CMA

690

0.0283

0.0678

0.4169

Mom

690

0.0663

0.1458

0.4545

The combined table is mainly a bookkeeping and comparison device. It gathers all factor candidates used later in the chapter and makes the sample change visible. A model with more factors is easier to estimate mechanically, but the reader still needs to know which factor histories are being compared.

Figure 4.6: Risk-return profile of the Fama-French five factors.

The five-factor risk-return graph shows whether the added profitability and investment factors occupy distinct positions relative to market, size, and value. If two factors have similar risk-return profiles, the regression may still distinguish them through covariance with asset returns.

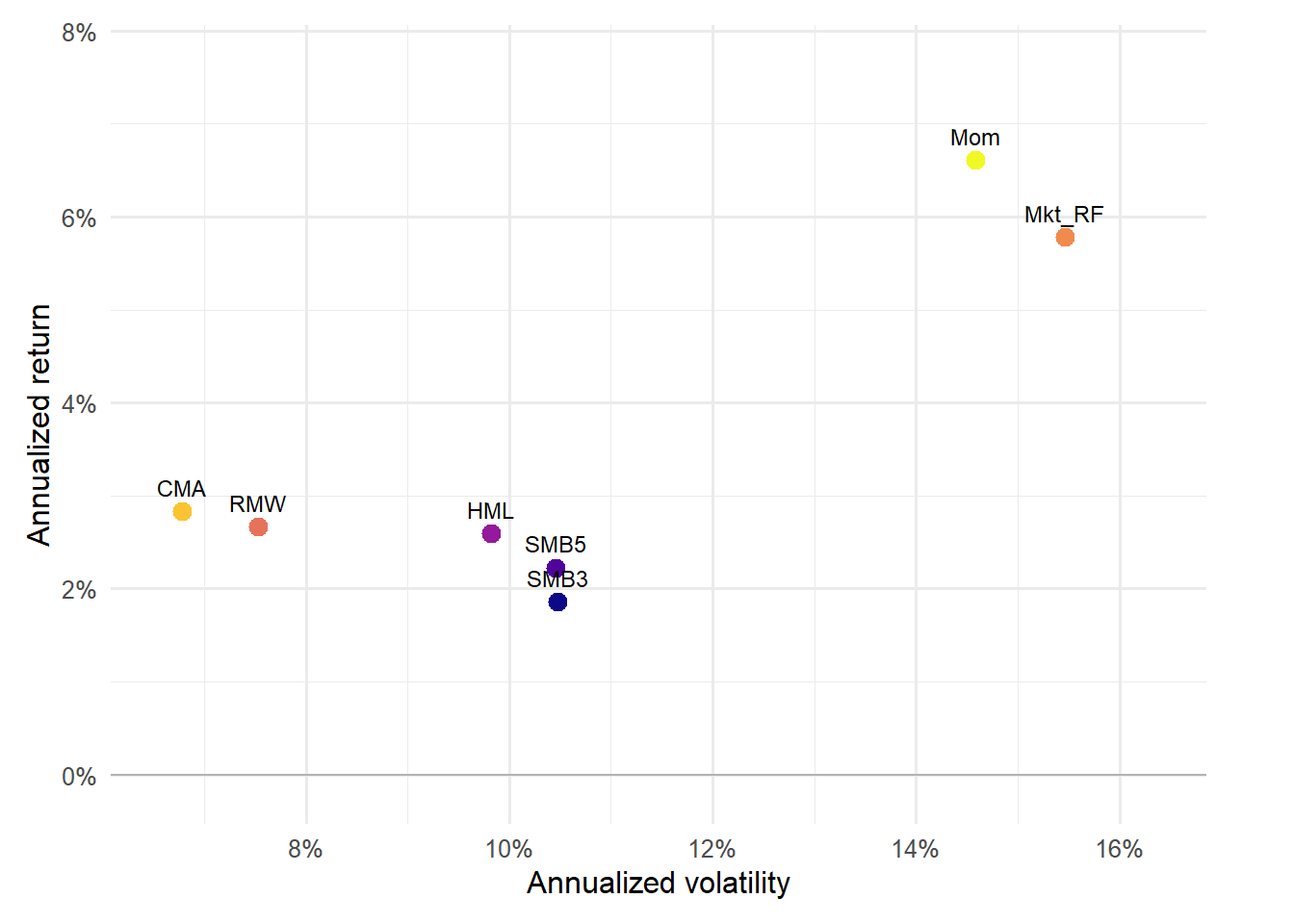

Figure 4.7: Risk-return profile of all factors used in the chapter.

The all-factor graph is the broadest factor map in the chapter. It summarizes the candidate explanatory variables before the chapter turns to test assets, where these factor histories become regressors.

Figure 4.8: Cumulative returns of the Fama-French five factors.

The cumulative five-factor plot lets the reader compare the newer factors in their available sample. The shorter window should be kept in mind when comparing these paths with the earlier three-factor histories.

Figure 4.9: Cumulative returns of all factors used in the chapter.

The cumulative all-factor figure is useful for seeing which factors dominate visually and which have more modest paths. This is a descriptive step; the regression step later asks whether these paths help explain asset returns.

Figure 4.10: Distribution of monthly returns for the Fama-French five factors.

The five-factor density plot shows how each factor behaves month by month. Students should read it together with the cumulative plot: the same factor can look attractive cumulatively while still having large monthly downside episodes.

Figure 4.11: Distribution of monthly returns for all factors used in the chapter.

The final factor-density plot closes the descriptive block. At this point, the reader has seen factor returns as tables, cumulative paths, risk-return points, and monthly distributions. The next step is to use those factor returns to explain the behavior of test assets.

4.5 Test assets and the size-value portfolios

The chapter uses two kinds of test assets. The first is FCNTX, a single mutual fund. The second is the 25 Fama-French size-value portfolios. The single asset is useful for seeing one regression closely. The 25 portfolios are useful for testing whether the model explains a structured cross-section of returns.

This table is the first bridge between an individual asset and the factor data. The column returns is the raw FCNTX return, while Re subtracts the risk-free rate. The regression will use Re as the dependent variable and factor returns as explanatory variables, so this joined table is the dataset for the first asset-pricing exercise.

The single-asset exercise checks the data before estimating the regression. The price table verifies the adjusted series used to compute returns. The return table verifies the monthly transformation. The joined table verifies that the excess return and factors are aligned at month end. Reading the three tables in order shows exactly how a price series becomes the dependent variable in the CAPM regression.

Code

first_last_rows(fund_prices) |>select(symbol, date, adjusted) |>kable(caption ="First and last FCNTX adjusted-price observations.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last FCNTX adjusted-price observations.

symbol

date

adjusted

FCNTX

1980-01-02

0.106178

FCNTX

1980-01-03

0.104777

FCNTX

1980-01-04

0.106365

FCNTX

2020-12-28

11.760650

FCNTX

2020-12-29

11.760650

FCNTX

2020-12-30

11.739573

Code

first_last_rows(fund_returns) |>kable(caption ="First and last FCNTX monthly raw returns.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last FCNTX monthly raw returns.

symbol

date

returns

FCNTX

1980-01-31

-0.009675

FCNTX

1980-02-29

-0.016874

FCNTX

1980-03-31

-0.089431

FCNTX

2020-10-30

-0.031775

FCNTX

2020-11-30

0.083591

FCNTX

2020-12-30

0.027920

Code

first_last_rows(fund_factors) |>select(symbol, date, returns, Re, Mkt_RF, SMB3, HML, Mom, SMB5, RMW, CMA, RF) |>kable(caption ="First and last FCNTX excess returns joined to all factors.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last FCNTX excess returns joined to all factors.

symbol

date

returns

Re

Mkt_RF

SMB3

HML

Mom

SMB5

RMW

CMA

RF

FCNTX

1980-01-31

-0.009675

-0.017675

0.0550

0.0162

0.0185

0.0745

0.0188

-0.0184

0.0189

0.0080

FCNTX

1980-02-29

-0.016874

-0.025774

-0.0123

-0.0186

0.0059

0.0789

-0.0162

-0.0095

0.0292

0.0089

FCNTX

1980-03-31

-0.089431

-0.101531

-0.1290

-0.0670

-0.0096

-0.0959

-0.0697

0.0182

-0.0105

0.0121

FCNTX

2020-10-31

-0.031775

-0.031875

-0.0208

0.0434

0.0425

-0.0310

0.0467

-0.0077

-0.0057

0.0001

FCNTX

2020-11-30

0.083591

0.083491

0.1245

0.0581

0.0209

-0.1260

0.0712

-0.0225

0.0128

0.0001

FCNTX

2020-12-31

0.027920

0.027820

0.0463

0.0501

-0.0168

-0.0227

0.0493

-0.0197

-0.0006

0.0001

Code

first_last_rows(portfolio_factor_data) |>select(date, symbol, returns, Re, Mkt_RF, SMB3, HML, Mom) |>kable(caption ="First and last 25-portfolio excess-return rows joined to FF3 and momentum.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last 25-portfolio excess-return rows joined to FF3 and momentum.

date

symbol

returns

Re

Mkt_RF

SMB3

HML

Mom

1927-01-31

SMALL LoBM

0.010954

0.008454

-0.0005

-0.0032

0.0458

0.0057

1927-01-31

ME1 BM2

-0.081352

-0.083852

-0.0005

-0.0032

0.0458

0.0057

1927-01-31

ME1 BM3

-0.048280

-0.050780

-0.0005

-0.0032

0.0458

0.0057

2020-12-31

ME5 BM3

0.034491

0.034391

0.0463

0.0501

-0.0168

-0.0227

2020-12-31

ME5 BM4

0.032226

0.032126

0.0463

0.0501

-0.0168

-0.0227

2020-12-31

BIG HiBM

0.080558

0.080458

0.0463

0.0501

-0.0168

-0.0227

Code

first_last_rows(portfolio_all_factor_data) |>select(date, symbol, returns, Re, Mkt_RF, SMB3, HML, Mom, SMB5, RMW, CMA) |>kable(caption ="First and last 25-portfolio excess-return rows joined to the expanded factor set.",digits =6,row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

First and last 25-portfolio excess-return rows joined to the expanded factor set.

date

symbol

returns

Re

Mkt_RF

SMB3

HML

Mom

SMB5

RMW

CMA

1963-07-31

SMALL LoBM

0.011287

0.008587

-0.0039

-0.0057

-0.0081

0.0101

-0.0048

0.0064

-0.0115

1963-07-31

ME1 BM2

-0.003632

-0.006332

-0.0039

-0.0057

-0.0081

0.0101

-0.0048

0.0064

-0.0115

1963-07-31

ME1 BM3

0.007223

0.004523

-0.0039

-0.0057

-0.0081

0.0101

-0.0048

0.0064

-0.0115

2020-12-31

ME5 BM3

0.034491

0.034391

0.0463

0.0501

-0.0168

-0.0227

0.0493

-0.0197

-0.0006

2020-12-31

ME5 BM4

0.032226

0.032126

0.0463

0.0501

-0.0168

-0.0227

0.0493

-0.0197

-0.0006

2020-12-31

BIG HiBM

0.080558

0.080458

0.0463

0.0501

-0.0168

-0.0227

0.0493

-0.0197

-0.0006

The sequence of data checks has a simple logic. First, prices become monthly returns. Second, raw returns become excess returns. Third, each excess return is matched to factor returns for the same month. The 25-portfolio checks repeat the same process for many test assets at once.

Annualized performance of FCNTX excess returns and the factors.

factor

months

annualized_return

annualized_volatility

return_per_unit_risk

SMB3

492

0.0060

0.1026

0.0584

SMB5

492

0.0069

0.1002

0.0690

HML

492

0.0145

0.1031

0.1407

Mom

492

0.0537

0.1557

0.3451

CMA

492

0.0266

0.0676

0.3929

RMW

492

0.0376

0.0818

0.4599

FCNTX

492

0.0771

0.1607

0.4798

Mkt_RF

492

0.0762

0.1561

0.4879

The FCNTX performance table places the mutual fund and factor portfolios on the same scale. This helps answer a descriptive question before estimation: does the fund look more volatile, less volatile, or more rewarded per unit of risk than the factors used to explain it?

Figure 4.12: Risk-return profile of FCNTX excess returns and the factors.

The risk-return figure makes the same comparison visually. FCNTX appears as one point among the factor portfolios, which helps the reader see whether the fund is close to market-like behavior or whether it sits in a different region of the return-risk space.

Figure 4.13: Cumulative excess returns of FCNTX and the factor portfolios.

The cumulative plot turns the FCNTX comparison into a time-series story. A fund can have a similar average return to a factor while following a different path through time. That difference is exactly what the regression tries to summarize with an intercept, beta, and residual.

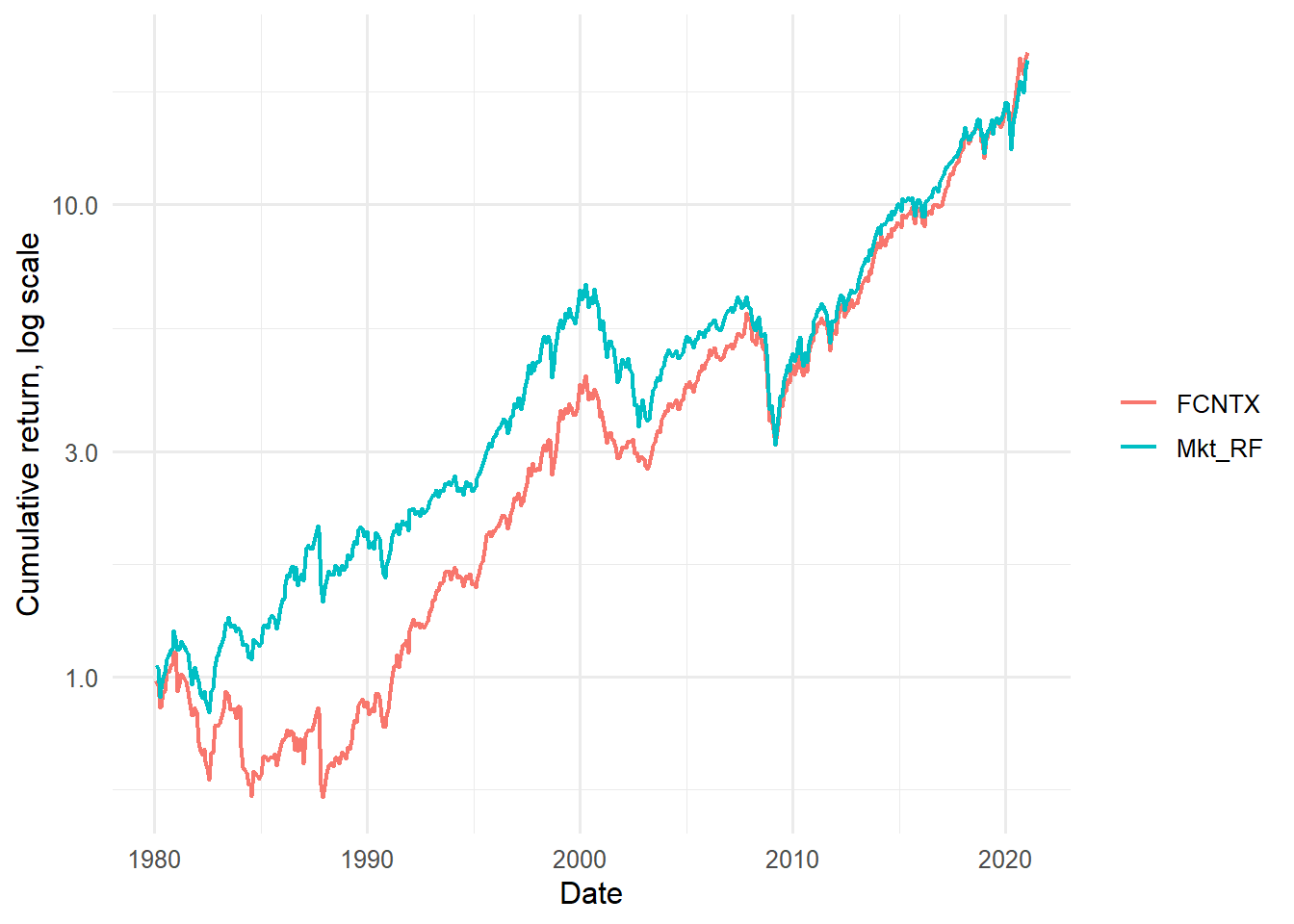

Figure 4.14: Cumulative excess returns of FCNTX and the market factor.

The market comparison isolates the CAPM idea. If FCNTX is mostly a market-risk asset, the FCNTX and market excess-return paths should move together in broad strokes. Differences between the paths foreshadow the residual component in the CAPM regression.

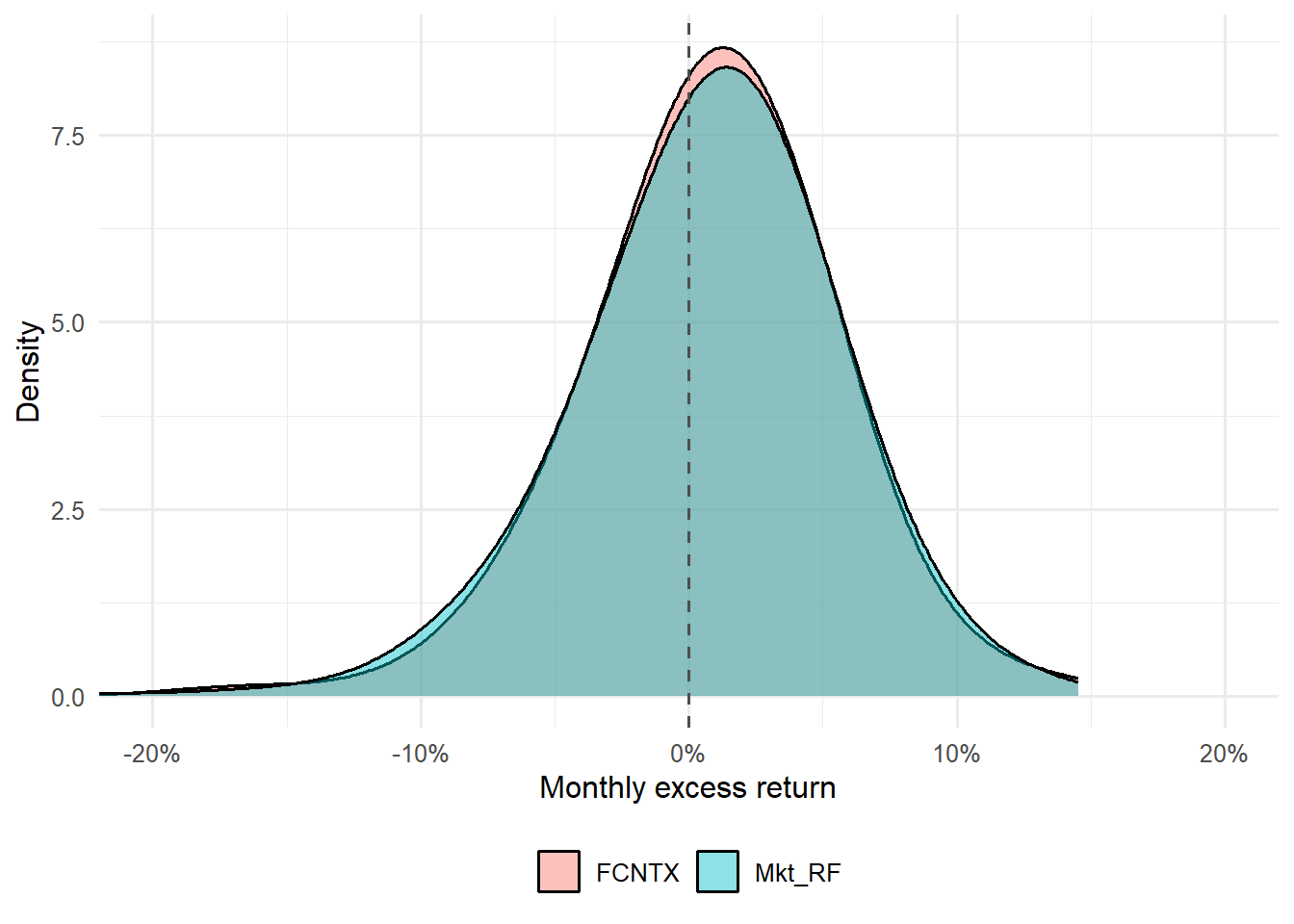

Figure 4.15: Distribution of monthly excess returns for FCNTX and the market factor.

The distribution plot adds another view of the same comparison. Overlap in the two densities suggests similar monthly-return behavior, while differences in spread or tails suggest that market exposure alone may leave unexplained variation.

The single-asset FCNTX example is useful because one regression can be read closely from beginning to end. The 25 Fama-French portfolios serve a different purpose: they create a structured cross-section. Each portfolio is formed by sorting firms by size and book-to-market, so the resulting grid gives the factor model a more demanding asset-pricing problem. The empirical task is now cross-sectional: explain systematic differences across size and value cells.

The same 25 portfolios can be read as investment portfolios through the usual risk-return lens. Annualized return, annualized volatility, and return per unit of risk show the economic content of the size-value grid. Each cell is a portfolio with its own average return and volatility.

Lowest and highest return-risk ratios among the 25 size-value portfolios.

symbol

annualized_return

annualized_volatility

return_per_unit_risk

SMALL LoBM

0.0294

0.4171

0.0705

ME1 BM2

0.0668

0.3380

0.1977

ME2 BM1

0.0795

0.2766

0.2876

BIG HiBM

0.1069

0.2957

0.3615

ME1 BM3

0.1143

0.3092

0.3697

ME5 BM3

0.1047

0.1944

0.5385

BIG LoBM

0.1006

0.1846

0.5447

ME3 BM2

0.1248

0.2253

0.5538

ME3 BM4

0.1345

0.2410

0.5582

ME3 BM3

0.1261

0.2247

0.5611

The table shows the extremes of the 25-portfolio risk-return ranking. This is a compact way to see that the size-value grid contains meaningful heterogeneity: some portfolios deliver much more return per unit of volatility than others.

Code

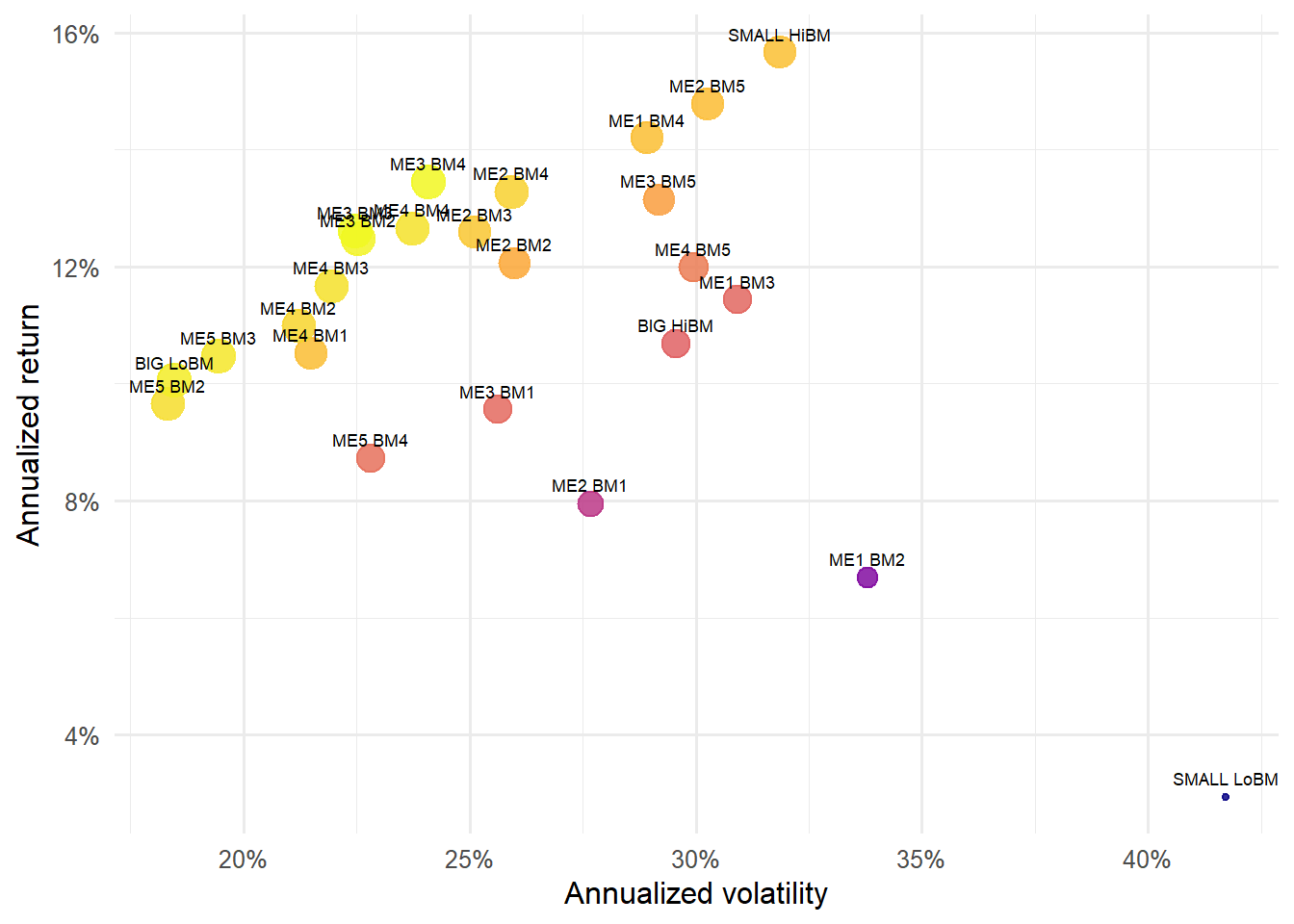

portfolio_perf |>ggplot(aes(annualized_volatility, annualized_return, color = return_per_unit_risk)) +geom_point(aes(size = return_per_unit_risk), alpha =0.85, show.legend =FALSE) +geom_text(aes(label = symbol), vjust =-0.9, size =2.4, color ="black") +labs(x ="Annualized volatility",y ="Annualized return",color ="Return per unit of risk" ) +scale_x_continuous(labels = scales::percent) +scale_y_continuous(labels = scales::percent) +scale_color_viridis_c(option ="C") +theme_minimal(base_size =12) +theme(legend.position ="bottom")

Figure 4.16: Risk-return profile of the 25 size-value portfolios.

The risk-return scatter makes the heterogeneity visible across all 25 portfolios. Dense labels are intentional here because each point is a named test asset. The graph prepares the reader for the asset-pricing question: can factor exposures explain why these portfolios occupy different locations?

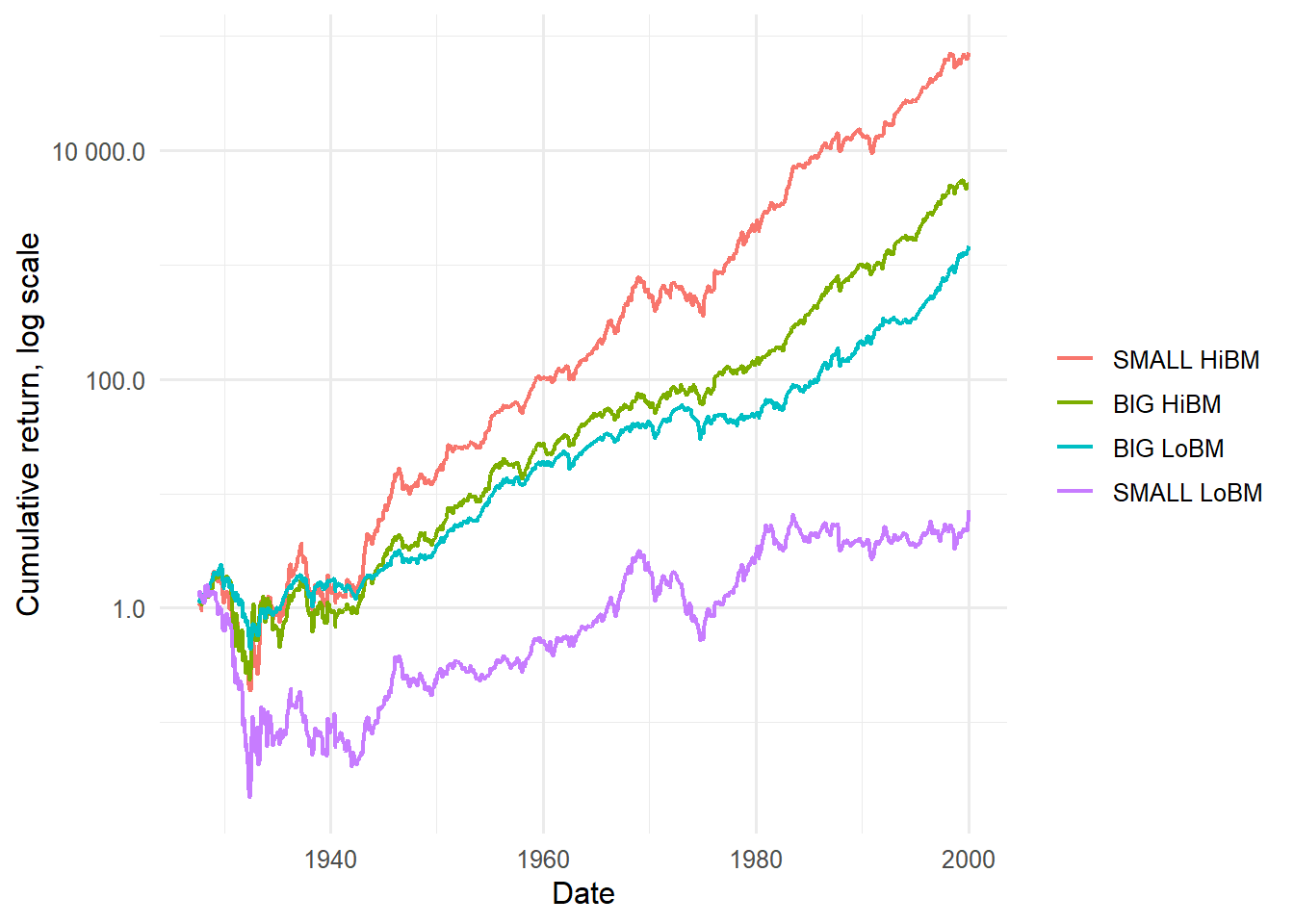

Kenneth French’s data library often illustrates the extreme size-value portfolios because they make the empirical pattern easy to see. The plot below keeps the four corner portfolios: small growth, small value, big growth, and big value.

Figure 4.17: Cumulative raw returns for the four corner size-value portfolios.

The four-corner cumulative plot focuses on the most interpretable cells of the grid. Comparing small versus big and low versus high book-to-market portfolios shows why the size-value sort became a standard test bed for factor models.

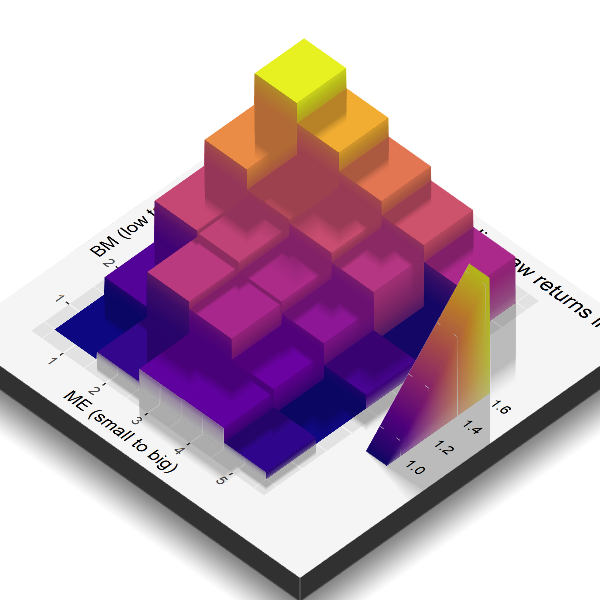

The rendered 3D surface gives a second view of the same size-value grid. The height and color of each cell represent the average monthly raw return of that portfolio.

Mean monthly raw returns behind the size-value surface.

ME

BM1 low

BM2

BM3

BM4

BM5 high

ME1 small

0.8830

0.9688

1.2728

1.4296

1.5976

ME2

0.9524

1.2231

1.2415

1.3062

1.5142

ME3

1.0306

1.1965

1.1989

1.2863

1.3704

ME4

1.0321

1.0570

1.1196

1.2225

1.3006

ME5 big

0.9443

0.9099

0.9878

0.9115

1.1976

The surface table gives the numeric values behind the rendered image. It is the same information in tabular form: rows move from small to big firms, columns move from low to high book-to-market firms, and each entry is the average monthly raw return in percent for that cell.

Figure 4.18: Rendered surface of the 25 size-value portfolio mean returns.

The rendered surface is a visual summary of the size-value pattern. Peaks mark cells with higher average monthly returns; lower blocks mark cells with lower average returns. The point of the figure is to make the cross-sectional pattern visible before the regression tries to explain it with factor exposures.

Animated rendered surface of the 25 size-value portfolio mean returns.

The animation rotates the same surface. It uses the same data and helps the reader see the three-dimensional structure of the 25 portfolio averages.

4.6 Time-series asset pricing regressions

The time-series regression estimates factor exposures for each asset. It uses many months of returns for one asset at a time and asks how that asset moves with the factors. In matrix form, for asset \(i\) and \(K\) factors,

This equation has two roles. The slope vector \(\boldsymbol{\beta}_i\) measures exposure to systematic risk. A high market beta means that the asset tends to rise more in strong market months and fall more in weak market months. A high value beta means that the asset tends to move with the HML factor. The intercept \(\alpha_i\) measures the average excess return that remains after the factor exposures have been used.

The residual \(\varepsilon_{i,t}\) is a month-by-month error. It measures the difference between the observed excess return in month \(t\) and the fitted value from the regression. The alpha is different because it is constant over the sample. It measures an average level left after the factors are included. This distinction is useful: residuals diagnose short-run fit, while alphas diagnose average pricing.

In regression-based asset pricing, alpha is read as a pricing error when the factors are traded return portfolios. A model that prices the asset well should leave a small alpha, because the asset’s average excess return should be accounted for by its factor exposures. For one asset, the alpha tells us what the model leaves unexplained for that asset. For the 25 portfolios, the collection of alphas is more informative: a pattern of large positive and negative alphas would show that the model misses a systematic part of the cross-section.

The regression is therefore doing two jobs at once. Statistically, it is a least-squares fit of returns on factors. Economically, it is asking whether the factor model has removed the average return that should be explained by risk exposure. Cochrane’s regression tests use this second reading: the intercept is evidence about whether the model prices the asset.

The code below wraps that equation in a reusable function. The formula defines the right-hand side. The grouping variable symbol defines which asset receives its own regression.

The code follows the equation in four steps. First, group_by(symbol) separates the data by asset. Second, lm(formula, data = .x) estimates one time-series regression for that asset. Third, broom::tidy() extracts the estimated intercept and betas. Fourth, broom::augment() returns fitted values and residuals month by month. These four objects correspond directly to the mathematical notation: coefficients, fitted values, residuals, and model diagnostics.

fund_capm <-fit_factor_model(fund_factors, Re ~ Mkt_RF)tidy_factor_model(fund_capm) |>mutate(across(where(is.numeric), ~round(.x, 6))) |>kable(caption ="CAPM time-series regression for FCNTX.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

CAPM time-series regression for FCNTX.

symbol

term

estimate

std.error

statistic

p.value

FCNTX

(Intercept)

0.000766

0.000977

0.783864

0.433499

FCNTX

Mkt_RF

0.913506

0.021423

42.641842

0.000000

The CAPM table has two central entries. The market coefficient is the estimated market beta of FCNTX: it measures how much the fund’s excess return changes with the market excess return. The intercept is the fund’s average excess return after controlling for market exposure. A positive intercept means that FCNTX earned more, on average, than the CAPM would assign from its market beta over this sample. A negative intercept means that the market exposure assigns more average excess return than the fund actually earned.

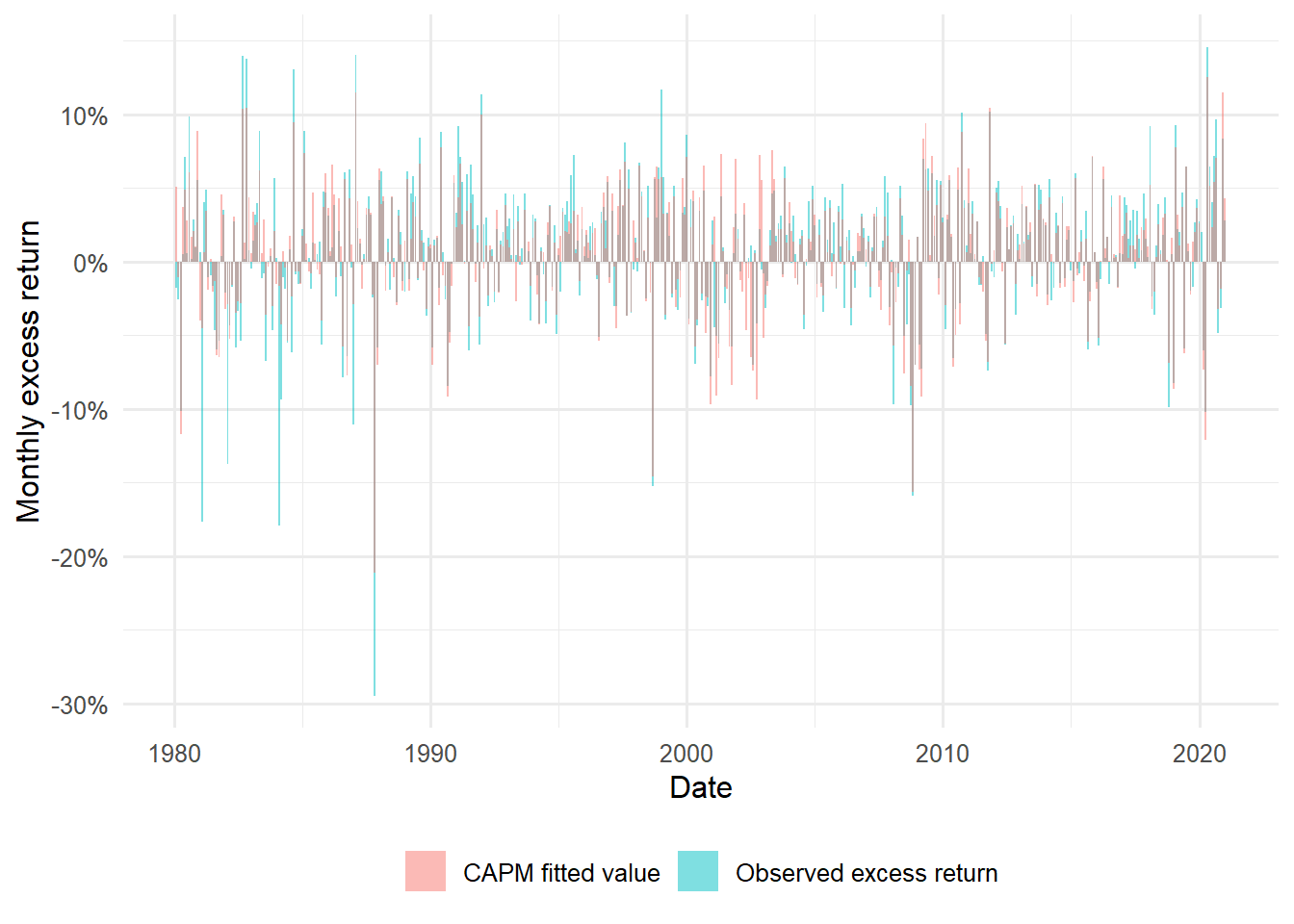

The fitted value is the model-implied excess return for each month:

augment_factor_model(fund_capm) |>ggplot(aes(date)) +geom_col(aes(y = Re, fill ="Observed excess return"), alpha =0.5) +geom_col(aes(y = .fitted, fill ="CAPM fitted value"), alpha =0.5) +labs(x ="Date", y ="Monthly excess return", fill =NULL) +scale_y_continuous(labels = scales::percent) +theme_minimal(base_size =12) +theme(legend.position ="bottom")

Figure 4.19: FCNTX excess returns and CAPM fitted values.

The fitted-value plot shows the CAPM as a month-by-month approximation. Months where the fitted bars and observed bars are close are months where market exposure explains much of the fund’s movement. Large gaps are residuals: the part of the FCNTX excess return left after the market factor is used.

The next graphs check whether the fitted values and residuals look reasonable. They are diagnostics for the time-series fit. They ask whether the CAPM regression is fitting the single asset in a stable way before the chapter moves to the 25-portfolio cross-section.

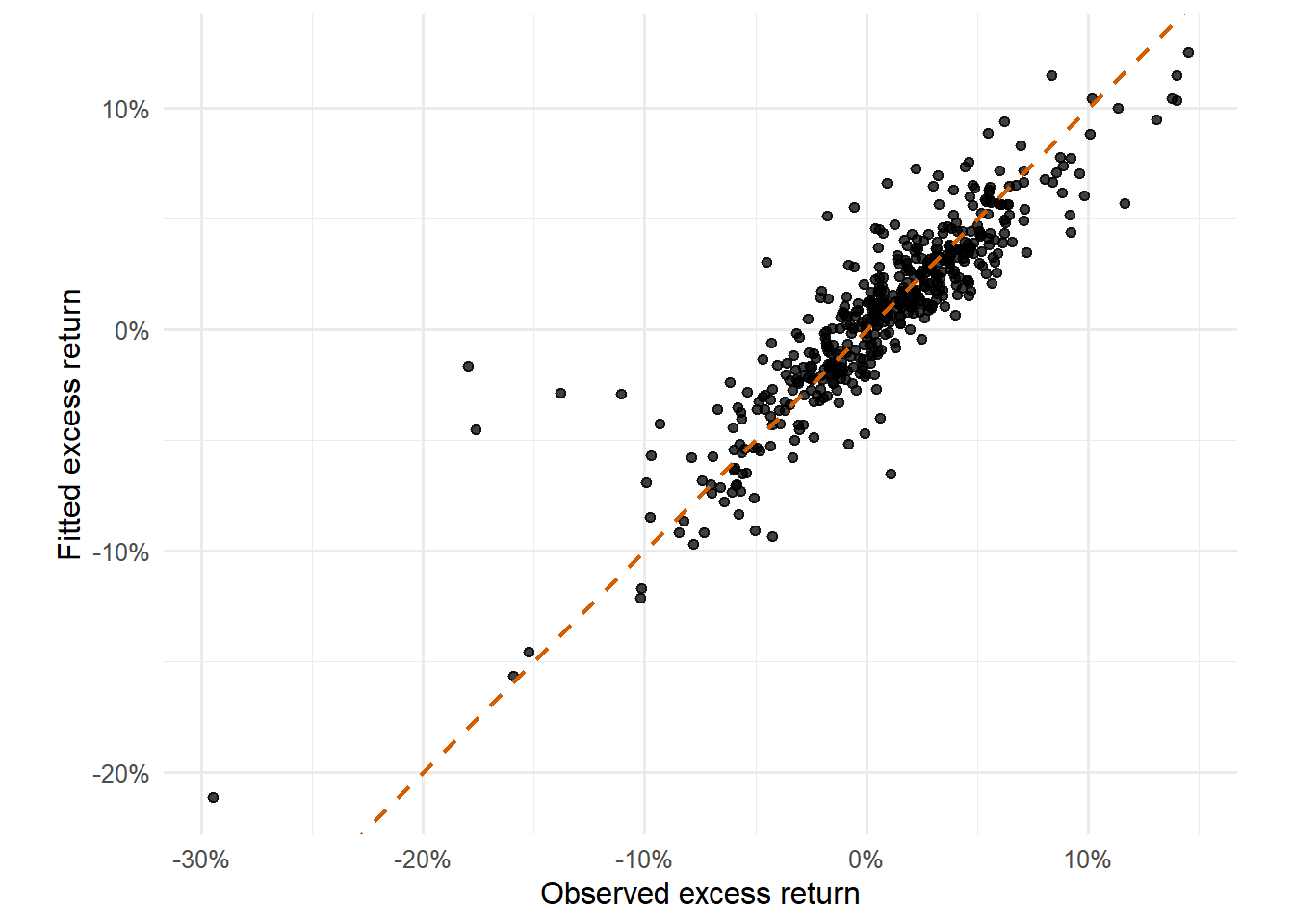

Figure 4.20: Observed and fitted FCNTX excess returns.

The observed-versus-fitted scatter compresses the time-series fit into one plane. Points near the 45-degree line indicate months where the CAPM fitted return is close to the observed FCNTX excess return. The spread around the line shows the size of month-level errors.

Code

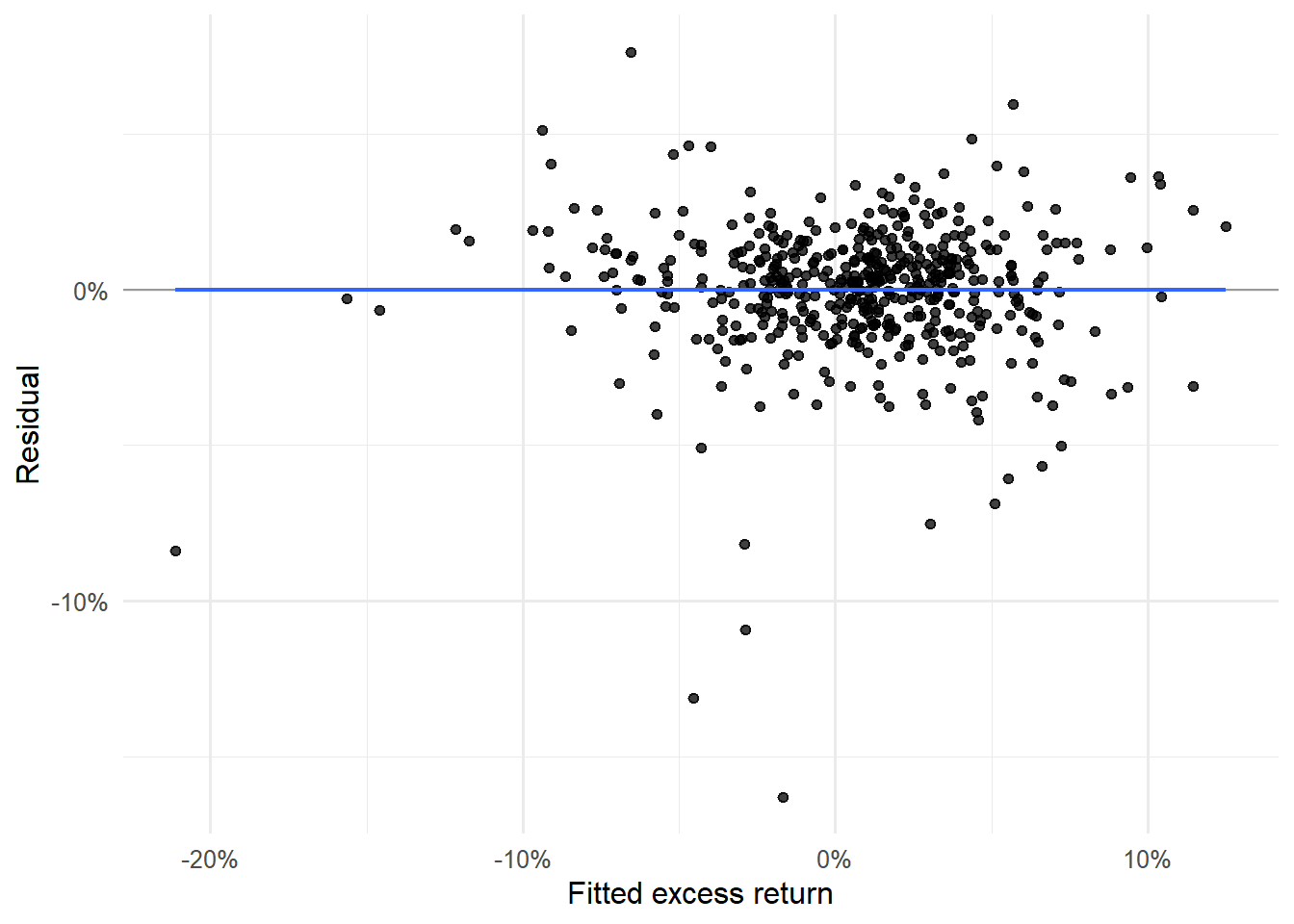

fund_capm_aug |>ggplot(aes(.fitted, .resid)) +geom_hline(yintercept =0, color ="gray60", linewidth =0.5) +geom_point(alpha =0.75) +geom_smooth(method ="lm", formula = y ~ x, se =FALSE, linewidth =0.8) +labs(x ="Fitted excess return", y ="Residual") +scale_x_continuous(labels = scales::percent) +scale_y_continuous(labels = scales::percent) +theme_minimal(base_size =12)

Figure 4.21: FCNTX residuals against fitted values.

The residuals-against-fitted graph checks whether errors change systematically with the fitted return. A visible slope or curved pattern would suggest that the single market factor is leaving structure in the residuals.

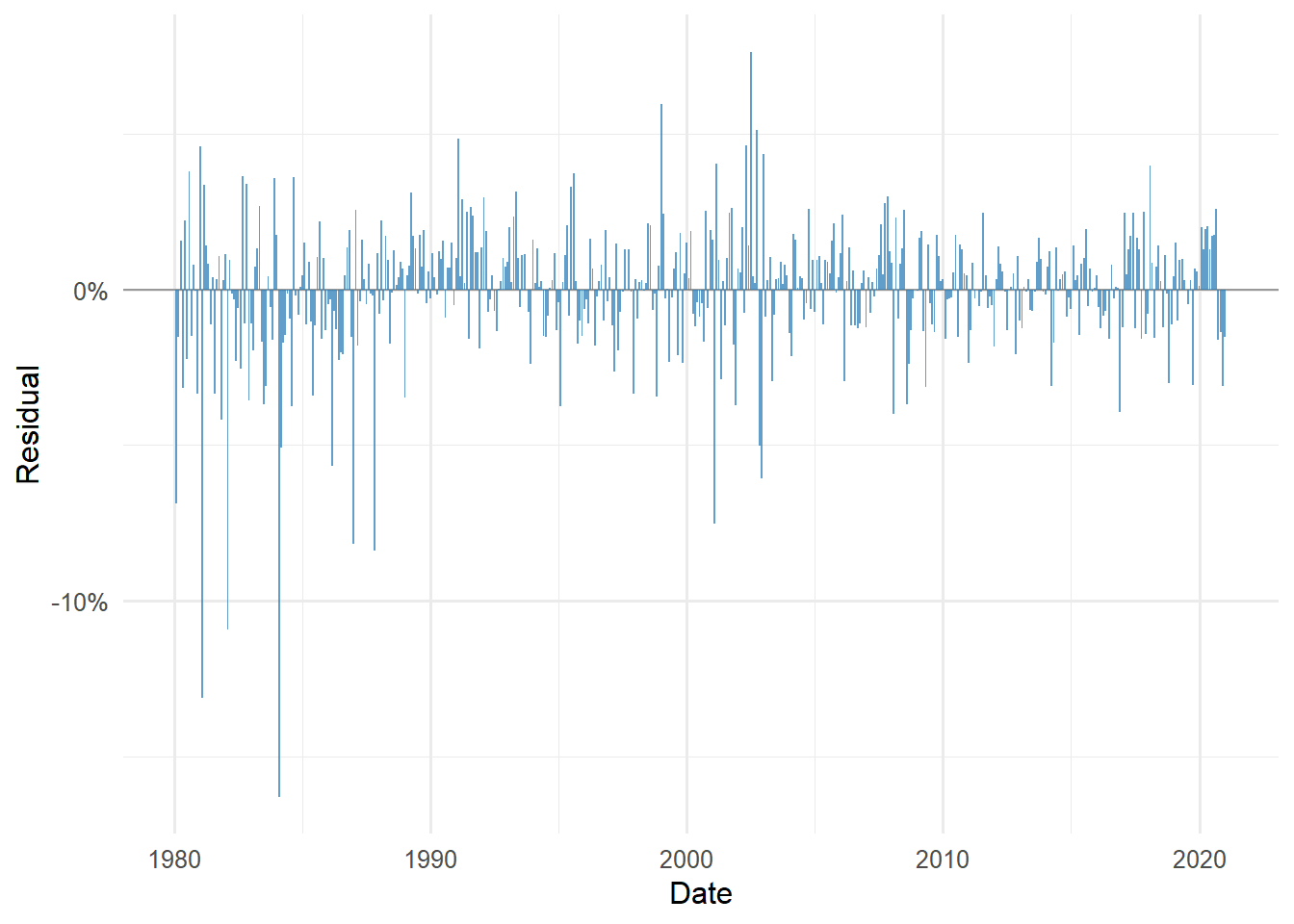

The residual time plot shows whether unexplained returns cluster in particular periods. Clusters are informative because they suggest that the model misses episodes where FCNTX behaves differently from the market factor.

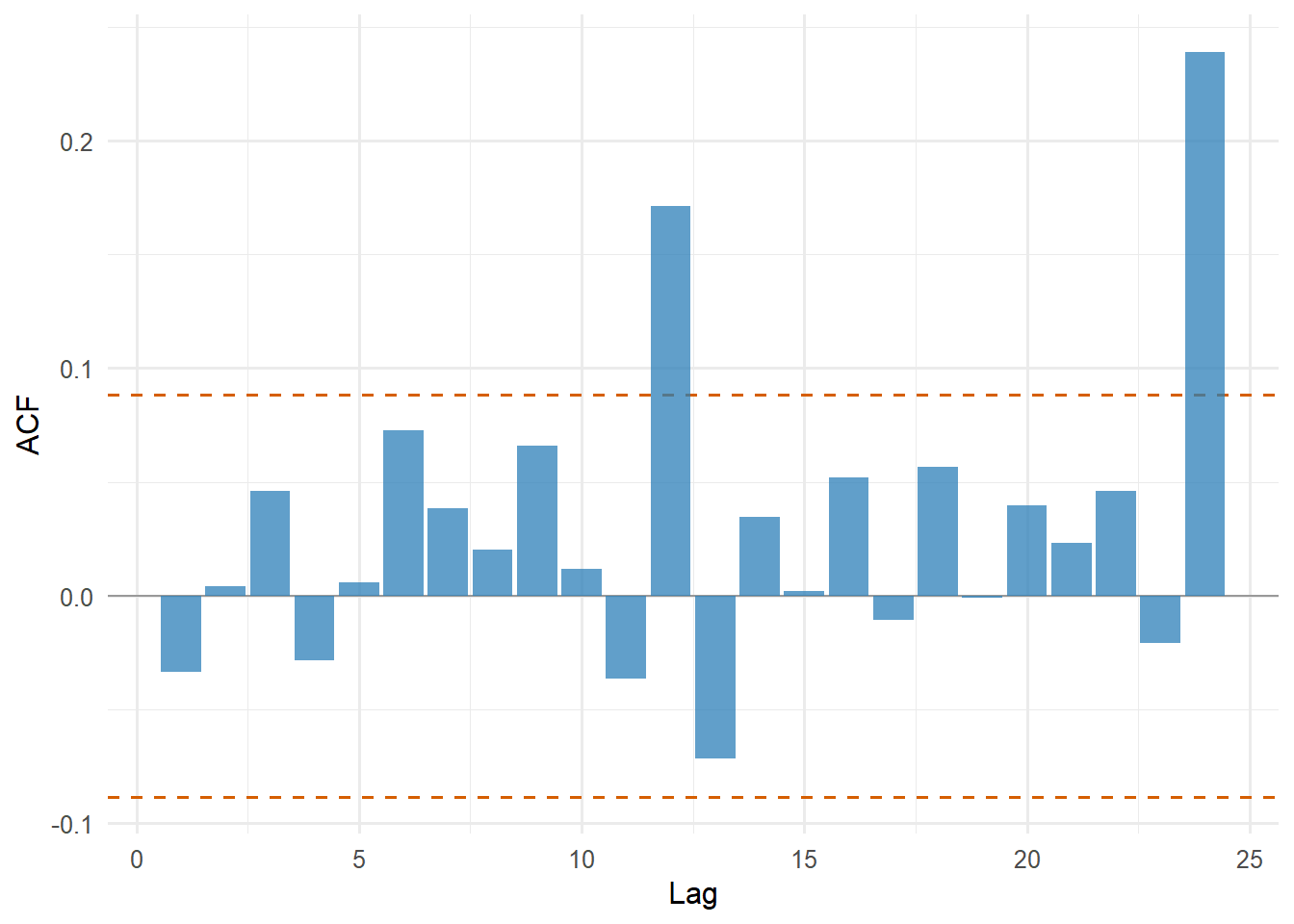

Figure 4.23: Autocorrelation function for FCNTX CAPM residuals.

The autocorrelation plot asks whether residuals are serially related. In a clean time-series regression, residuals should have little predictable structure across lags. Large bars would indicate persistence in the unexplained component.

Code

fund_capm_aug |>group_by(symbol) |>summarise(ljung_box_p_value =Box.test(.resid, lag =10, type ="Ljung-Box", fitdf =2)$p.value,box_pierce_p_value =Box.test(.resid, lag =10, type ="Box-Pierce", fitdf =2)$p.value,.groups ="drop" ) |>mutate(across(where(is.numeric), ~round(.x, 6))) |>kable(caption ="Residual autocorrelation checks for the FCNTX CAPM regression.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Residual autocorrelation checks for the FCNTX CAPM regression.

symbol

ljung_box_p_value

box_pierce_p_value

FCNTX

0.446514

0.459492

The Ljung-Box and Box-Pierce p-values formalize the residual-autocorrelation check. They summarize whether residual autocorrelation is large enough to be a statistical concern at the chosen lag.

For the 25 portfolios, the CAPM estimates 25 market betas:

Code

portfolio_capm <-fit_factor_model(portfolio_factor_data, Re ~ Mkt_RF)tidy_factor_model(portfolio_capm) |>filter(term =="Mkt_RF") |>arrange(estimate) |>slice(c(1:5, (n() -4):n())) |>mutate(across(where(is.numeric), ~round(.x, 6))) |>kable(caption ="Lowest and highest CAPM market betas among the 25 portfolios.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Lowest and highest CAPM market betas among the 25 portfolios.

symbol

term

estimate

std.error

statistic

p.value

ME5 BM2

Mkt_RF

0.948845

0.008293

114.41417

0

BIG LoBM

Mkt_RF

0.956923

0.008451

113.23358

0

ME5 BM3

Mkt_RF

0.973296

0.011799

82.48904

0

ME4 BM1

Mkt_RF

1.087596

0.012244

88.82592

0

ME4 BM2

Mkt_RF

1.092239

0.010432

104.69953

0

SMALL HiBM

Mkt_RF

1.378264

0.030716

44.87166

0

ME2 BM5

Mkt_RF

1.389511

0.025664

54.14304

0

ME1 BM2

Mkt_RF

1.404849

0.034684

40.50444

0

ME4 BM5

Mkt_RF

1.407824

0.023693

59.42046

0

SMALL LoBM

Mkt_RF

1.612572

0.046799

34.45776

0

The beta table shows the range of market exposures across the 25 portfolios. This range is important because cross-sectional asset pricing needs variation in exposures. If all portfolios had nearly identical market betas, market beta would have little power to explain differences in average returns.

Code

tidy_factor_model(portfolio_capm) |>arrange(symbol, term) |>mutate(across(where(is.numeric), ~round(.x, 6))) |>kable(caption ="CAPM coefficients for all 25 size-value portfolios.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

CAPM coefficients for all 25 size-value portfolios.

symbol

term

estimate

std.error

statistic

p.value

BIG HiBM

(Intercept)

0.000386

0.001466

0.263512

0.792204

BIG HiBM

Mkt_RF

1.311025

0.027131

48.322346

0.000000

BIG LoBM

(Intercept)

0.000235

0.000457

0.514319

0.607130

BIG LoBM

Mkt_RF

0.956923

0.008451

113.233577

0.000000

ME1 BM2

(Intercept)

-0.002389

0.001874

-1.274688

0.202683

ME1 BM2

Mkt_RF

1.404849

0.034684

40.504445

0.000000

ME1 BM3

(Intercept)

0.000817

0.001540

0.530487

0.595879

ME1 BM3

Mkt_RF

1.370093

0.028504

48.066185

0.000000

ME1 BM4

(Intercept)

0.003006

0.001452

2.070068

0.038674

ME1 BM4

Mkt_RF

1.276523

0.026874

47.499692

0.000000

ME2 BM1

(Intercept)

-0.001812

0.001266

-1.431260

0.152633

ME2 BM1

Mkt_RF

1.272654

0.023426

54.326724

0.000000

ME2 BM2

(Intercept)

0.001222

0.001082

1.129123

0.259087

ME2 BM2

Mkt_RF

1.233511

0.020020

61.613546

0.000000

ME2 BM3

(Intercept)

0.001573

0.001013

1.553653

0.120548

ME2 BM3

Mkt_RF

1.201998

0.018741

64.136138

0.000000

ME2 BM4

(Intercept)

0.002183

0.001097

1.989744

0.046861

ME2 BM4

Mkt_RF

1.222209

0.020303

60.199031

0.000000

ME2 BM5

(Intercept)

0.002979

0.001387

2.148093

0.031919

ME2 BM5

Mkt_RF

1.389511

0.025664

54.143036

0.000000

ME3 BM1

(Intercept)

-0.000804

0.000957

-0.840684

0.400704

ME3 BM1

Mkt_RF

1.251067

0.017708

70.650107

0.000000

ME3 BM2

(Intercept)

0.001550

0.000723

2.143617

0.032277

ME3 BM2

Mkt_RF

1.132414

0.013380

84.637675

0.000000

ME3 BM3

(Intercept)

0.001725

0.000745

2.315546

0.020762

ME3 BM3

Mkt_RF

1.123102

0.013787

81.459133

0.000000

ME3 BM4

(Intercept)

0.002106

0.000907

2.322279

0.020396

ME3 BM4

Mkt_RF

1.174158

0.016781

69.970866

0.000000

ME3 BM5

(Intercept)

0.001745

0.001260

1.384606

0.166447

ME3 BM5

Mkt_RF

1.366313

0.023325

58.577659

0.000000

ME4 BM1

(Intercept)

0.000217

0.000662

0.327664

0.743227

ME4 BM1

Mkt_RF

1.087596

0.012244

88.825923

0.000000

ME4 BM2

(Intercept)

0.000440

0.000564

0.780063

0.435518

ME4 BM2

Mkt_RF

1.092239

0.010432

104.699533

0.000000

ME4 BM3

(Intercept)

0.000989

0.000682

1.449711

0.147417

ME4 BM3

Mkt_RF

1.107003

0.012623

87.695115

0.000000

ME4 BM4

(Intercept)

0.001596

0.000863

1.850184

0.064549

ME4 BM4

Mkt_RF

1.164925

0.015966

72.964317

0.000000

ME4 BM5

(Intercept)

0.000763

0.001280

0.595705

0.551492

ME4 BM5

Mkt_RF

1.407824

0.023693

59.420458

0.000000

ME5 BM2

(Intercept)

-0.000152

0.000448

-0.339499

0.734297

ME5 BM2

Mkt_RF

0.948845

0.008293

114.414172

0.000000

ME5 BM3

(Intercept)

0.000567

0.000638

0.889874

0.373724

ME5 BM3

Mkt_RF

0.973296

0.011799

82.489044

0.000000

ME5 BM4

(Intercept)

-0.001169

0.000868

-1.347608

0.178056

ME5 BM4

Mkt_RF

1.106035

0.016059

68.872918

0.000000

SMALL HiBM

(Intercept)

0.003906

0.001660

2.353169

0.018785

SMALL HiBM

Mkt_RF

1.378264

0.030716

44.871658

0.000000

SMALL LoBM

(Intercept)

-0.004870

0.002529

-1.925603

0.054406

SMALL LoBM

Mkt_RF

1.612572

0.046799

34.457758

0.000000

The full coefficient table keeps the individual portfolio estimates visible. Each portfolio has its own intercept and market beta, so the CAPM is estimated as 25 separate time-series regressions, one for each test asset. The market beta column measures exposure. The intercept column should be read as the CAPM pricing error for each portfolio. If those intercepts are systematically high for one part of the size-value grid and low for another, the CAPM is missing a cross-sectional pattern across many assets.

The 25 separate CAPM regressions have different levels of fit. A compact way to inspect them is to compare \(R^2\), residual standard error, and residual autocorrelation diagnostics across portfolios.

Code

portfolio_capm_diagnostics <-glance_factor_model(portfolio_capm) |>select(symbol, r.squared, adj.r.squared, sigma, AIC, BIC) |>arrange(r.squared)portfolio_capm_diagnostics |>slice(c(1:5, (n() -4):n())) |>mutate(across(where(is.numeric), ~round(.x, 4))) |>kable(caption ="Lowest and highest CAPM goodness-of-fit values among the 25 portfolios.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Lowest and highest CAPM goodness-of-fit values among the 25 portfolios.

symbol

r.squared

adj.r.squared

sigma

AIC

BIC

SMALL LoBM

0.5133

0.5128

0.0843

-2375.900

-2360.815

ME1 BM2

0.5930

0.5926

0.0624

-3051.749

-3036.664

SMALL HiBM

0.6413

0.6410

0.0553

-3325.851

-3310.767

ME1 BM4

0.6671

0.6668

0.0484

-3627.258

-3612.173

ME1 BM3

0.6723

0.6720

0.0513

-3494.418

-3479.333

ME4 BM3

0.8723

0.8722

0.0227

-5331.951

-5316.866

ME4 BM1

0.8751

0.8750

0.0220

-5400.756

-5385.671

ME4 BM2

0.9068

0.9068

0.0188

-5762.069

-5746.985

BIG LoBM

0.9193

0.9192

0.0152

-6237.228

-6222.144

ME5 BM2

0.9208

0.9207

0.0149

-6279.753

-6264.668

The goodness-of-fit table shows which portfolios are relatively well described by the market factor and which are less well described. A higher \(R^2\) means that market movements explain a larger fraction of that portfolio’s excess return variation.

Code

augment_factor_model(portfolio_capm) |>group_by(symbol) |>summarise(box_pierce_p_value =Box.test(.resid, lag =10, type ="Box-Pierce", fitdf =2)$p.value,.groups ="drop" ) |>arrange(box_pierce_p_value) |>slice(c(1:5, (n() -4):n())) |>mutate(box_pierce_p_value =round(box_pierce_p_value, 6)) |>kable(caption ="Lowest and highest Box-Pierce p-values for the 25 CAPM residual series.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Lowest and highest Box-Pierce p-values for the 25 CAPM residual series.

symbol

box_pierce_p_value

ME3 BM4

0.000000

ME2 BM4

0.000000

SMALL LoBM

0.000000

ME4 BM5

0.000000

ME4 BM2

0.000000

ME3 BM5

0.003763

ME1 BM3

0.008790

ME4 BM1

0.015569

SMALL HiBM

0.043218

ME5 BM2

0.075859

The residual test table extends the diagnostic logic from FCNTX to the full portfolio set. Portfolios with very small p-values deserve attention because their residuals show stronger serial structure under the CAPM specification.

4.7 Asset pricing errors and factor exposures

The Fama-French three-factor model is the main worked example for the rest of the chapter. It is detailed enough to show the full econometric route: first estimate time-series betas, then estimate cross-sectional prices of risk, then compare the beta-method with SDF-GMM estimates. Momentum and the five-factor model appear later as faster extensions. They are useful for comparison, while the main explanation is developed with FF3.

The Fama-French three-factor model adds size and value exposures:

The fitted expected excess return is obtained by taking the estimated factor loadings and multiplying them by average factor returns. The intercept is reported separately because, in asset pricing, alpha is the pricing error:

This equation is the bridge between the regression table and the asset-pricing plot. The regression estimates betas. The asset-pricing restriction asks whether those betas, without an asset-specific alpha, explain average excess returns. If \(\widehat{\alpha}_i\) is economically important, the factor model is leaving a pricing error for asset \(i\).

The distinction is important for interpretation. A time-series regression with an intercept can always decompose the sample average return into two parts:

The term \(\widehat{\boldsymbol{\beta}}_i^\top\bar{\mathbf{f}}\) is the return explained by factor exposures. The term \(\widehat{\alpha}_i\) is the part that remains asset-specific after those exposures have been used. The asset-pricing question is therefore direct: are the alphas small enough for the factor model to be a credible explanation of average returns?

This decomposition comes from averaging the monthly regression over the sample. Start with the fitted regression,

In an ordinary least-squares regression with an intercept, the sample average of the residuals is zero. That is why the average return can be written as alpha plus the factor-implied component. This algebra also explains why a time-series fitted-average plot can look strong: each asset has its own intercept. The stricter asset-pricing question begins when the chapter asks whether the factor exposures alone can organize average returns across many assets through common prices of risk.

The code mirrors the same decomposition. The function expected_return_from_betas() first computes average factor returns, then multiplies them by the estimated betas, then keeps alpha separately. The column factor_implied_percent is \(100\widehat{\boldsymbol{\beta}}_i^\top\bar{\mathbf{f}}\). The column alpha_percent is \(100\widehat{\alpha}_i\). The observed average excess return is the sum of those two pieces, up to rounding.

This code block prepares the data for the figures that follow. It estimates the three-factor model, stores each portfolio’s factor exposures, computes the factor-implied part of average return, and keeps alpha as the remaining asset-specific component.

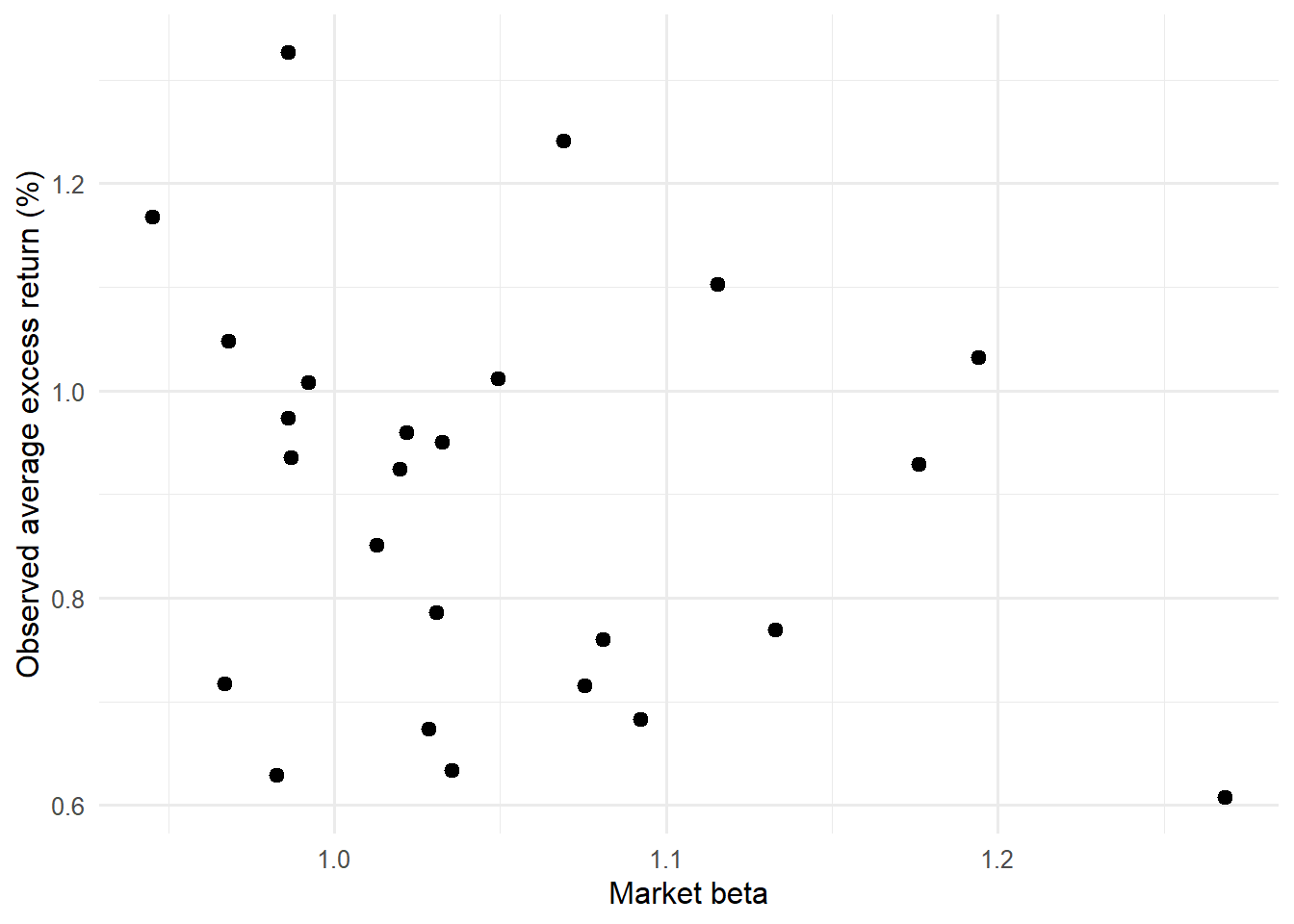

The size and value patterns can be inspected directly by reading average excess returns against market beta by portfolio sort.

The market-beta plots deliberately ignore the fitted-return axis and return to the raw relation between market exposure and average excess returns. If market beta were enough to explain the 25 portfolios, higher beta portfolios would line up with higher average returns in a stable pattern. The size and value groupings show whether portfolios with similar market beta still differ because of their position in the size-value grid.

Code

ff3_betas |>filter(term =="Mkt_RF") |>rename(market_beta = estimate) |>select(symbol, market_beta) |>inner_join(ff3_expected, by ="symbol") |>ggplot(aes(market_beta, ERe_percent)) +geom_point(size =2.2) +labs(x ="Market beta", y ="Observed average excess return (%)") +theme_minimal(base_size =12)

Figure 4.24: Market beta and average excess returns for the 25 portfolios.

The plain market-beta graph is the starting point for the anomaly discussion. If market beta alone organized average returns, the cloud would show a clear upward relation. A scattered pattern motivates the size and value groupings in the next two figures.

Code

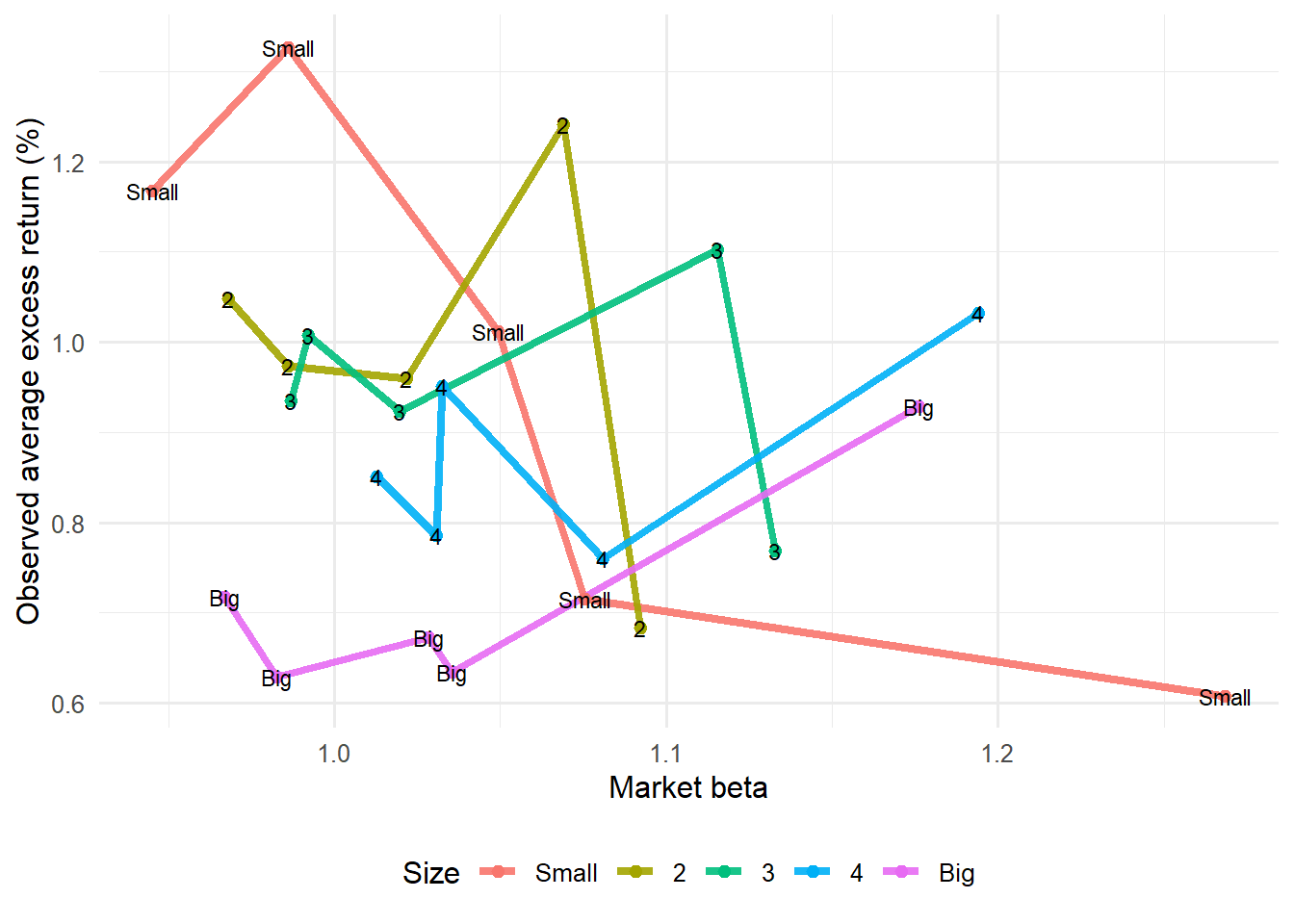

ff3_betas |>filter(term =="Mkt_RF") |>rename(market_beta = estimate) |>select(symbol, market_beta) |>inner_join(ff3_expected, by ="symbol") |>ggplot(aes(market_beta, ERe_percent, color = Size, group = Size)) +geom_line(alpha =0.9, linewidth =1.5) +geom_point(size =2) +geom_text(aes(label = Size), color ="black", size =3, show.legend =FALSE) +labs(x ="Market beta", y ="Observed average excess return (%)", color ="Size") +theme_minimal(base_size =12) +theme(legend.position ="bottom")

Figure 4.25: Market beta and average excess returns by size portfolio.

The size plot connects each point to its size group. Lines that separate by size indicate that portfolios with similar market beta can have different average returns because they belong to different size cells.

Code

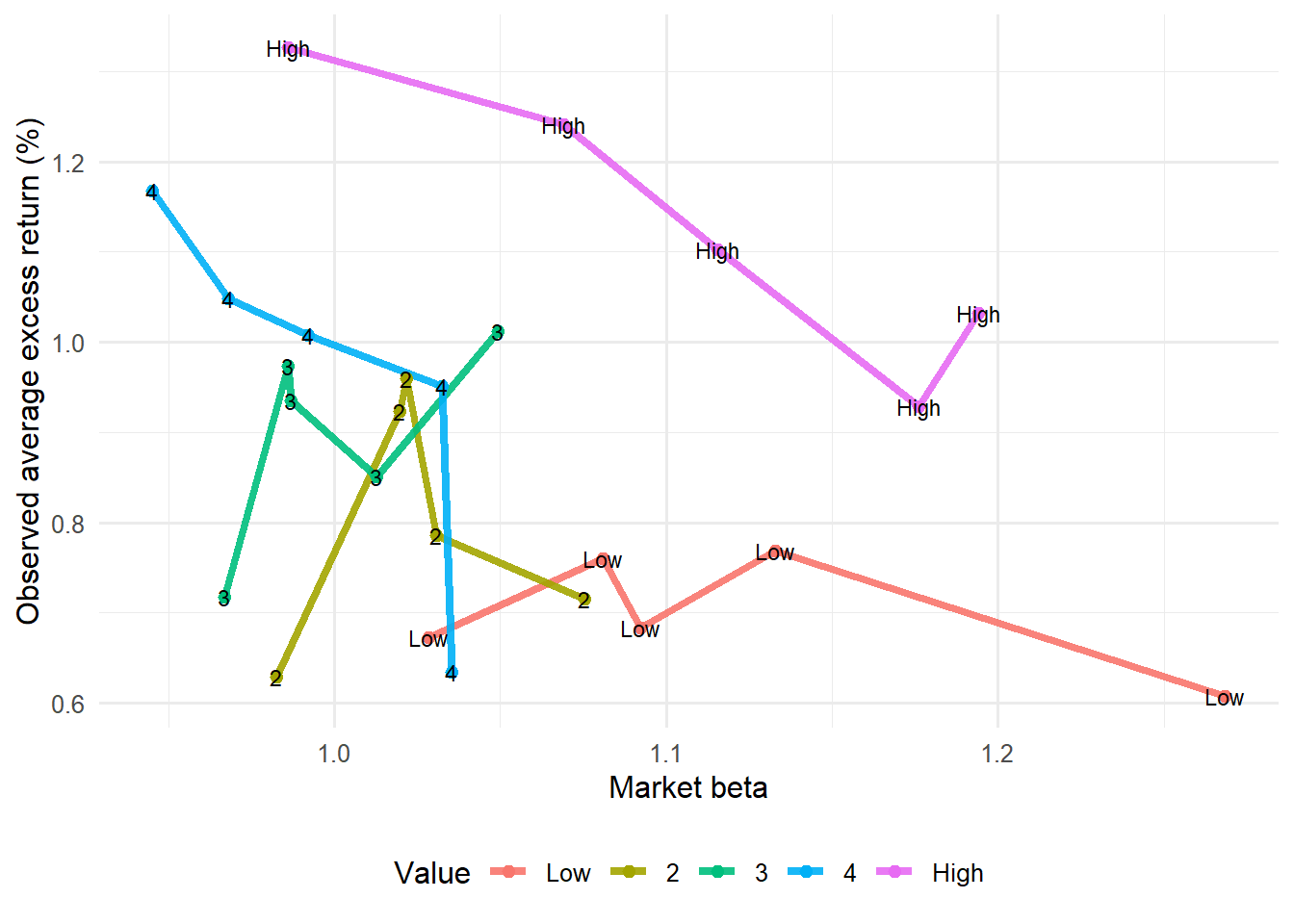

ff3_betas |>filter(term =="Mkt_RF") |>rename(market_beta = estimate) |>select(symbol, market_beta) |>inner_join(ff3_expected, by ="symbol") |>ggplot(aes(market_beta, ERe_percent, color = Value, group = Value)) +geom_line(alpha =0.9, linewidth =1.5) +geom_point(size =2) +geom_text(aes(label = Value), color ="black", size =3, show.legend =FALSE) +labs(x ="Market beta", y ="Observed average excess return (%)", color ="Value") +theme_minimal(base_size =12) +theme(legend.position ="bottom")

Figure 4.26: Market beta and average excess returns by value portfolio.

The value plot reads the same beta-return relation through book-to-market groups. Separation by value group is the visual motivation for adding the HML factor to the model.

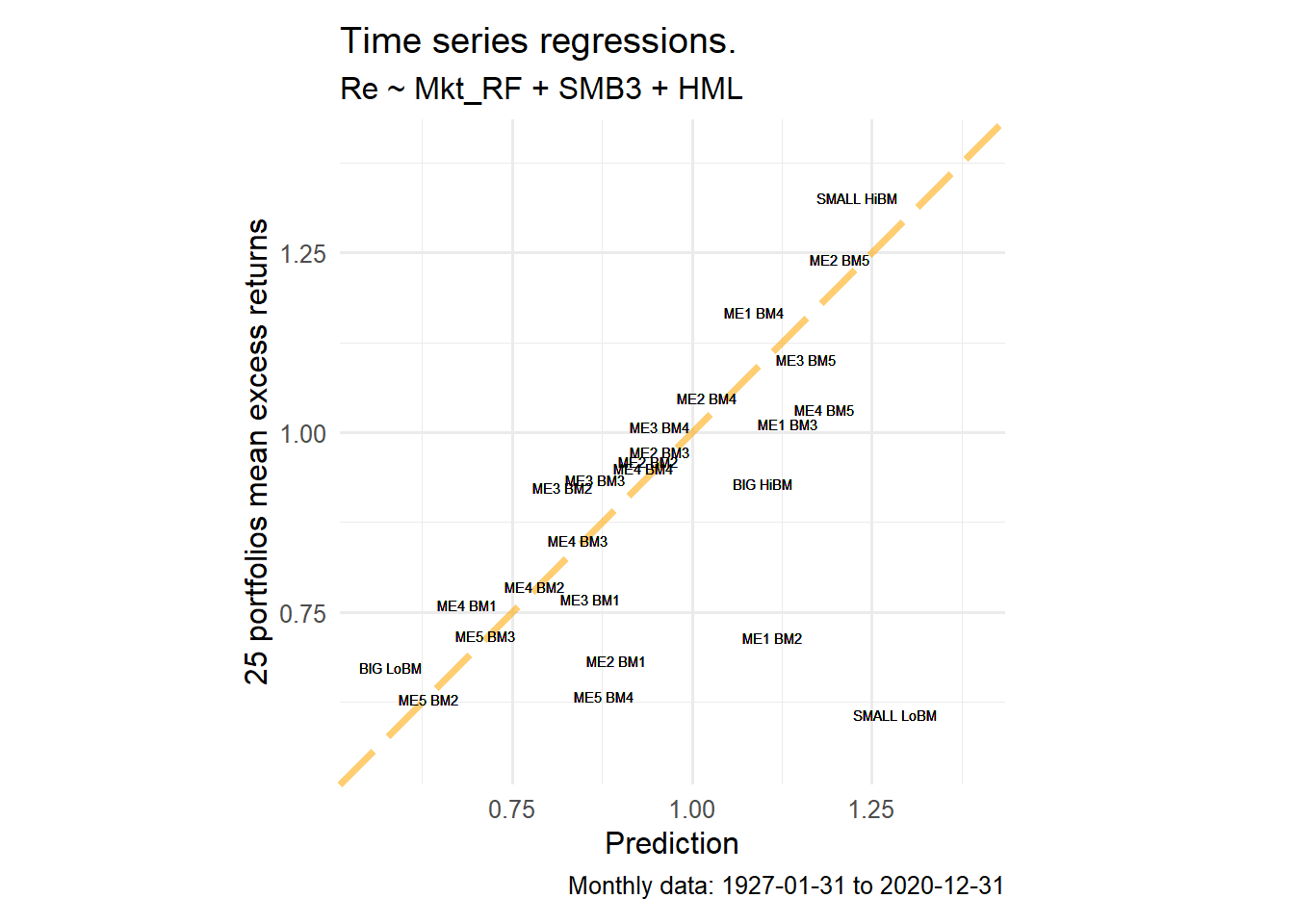

The next diagnostic compares observed average excess returns with predictions assembled from the time-series regression output. This is the last first-pass graph before the chapter moves to cross-sectional pricing. For each portfolio, the regression estimates an intercept and factor loadings. In consistent decimal units, the sample-average decomposition is

These prediction figures should be read as orientation and replication checks. They preserve the display convention of the source FF exercise: average excess returns and factor means are displayed in percent, while the intercept is kept as the coefficient returned by the regression. This convention preserves the numerical values of the FF graphic.

The formal asset-pricing interpretation remains the decimal-unit decomposition above. That equation is the coherent accounting identity: average excess return equals alpha plus the factor-implied component. The figures in this block have a narrower role. They show whether portfolios with high observed average returns also receive high first-pass fitted values before the chapter moves to the stricter cross-sectional pricing test.

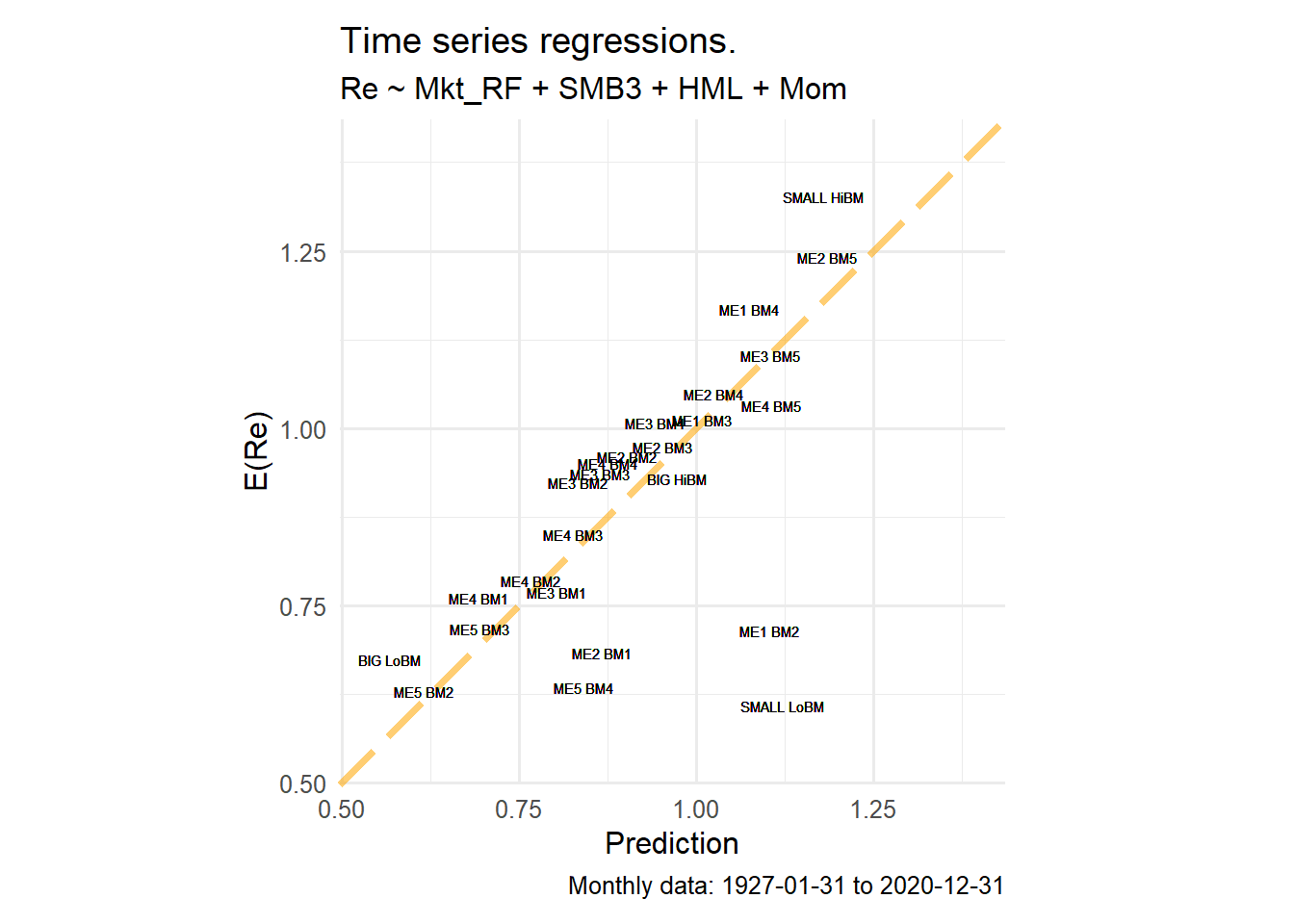

The reading is the same as in the FF3 figure. Adding momentum changes the factor set used to compute the prediction, while the observed average excess return on the vertical axis remains the same portfolio statistic. The figure is a source exercise replication check and a transition to the next section. The cross-sectional test begins after this point, where common prices of risk are estimated across portfolios.

Figure 4.28: Time-series fitted average excess returns under the FF3-plus-momentum model.

The remaining asset-pricing tests use a deliberate division of labor. FF3 is the detailed benchmark. The two extensions are included to show how the results change when the factor set expands.

Code

model_comparison_roadmap <-tibble(model =c("FF3", "FF3 plus momentum", "FF5"),role =c("Detailed benchmark", "Fast comparison", "Fast comparison"),factors =c("Mkt_RF, SMB3, HML","Mkt_RF, SMB3, HML, Mom","Mkt_RF, SMB5, HML, RMW, CMA" ),sample_start =c(min(portfolio_factor_data$date),min(portfolio_factor_data$date),min(portfolio_all_factor_data$date) ),sample_end =c(max(portfolio_factor_data$date),max(portfolio_factor_data$date),max(portfolio_all_factor_data$date) ),months =c(n_distinct(portfolio_factor_data$date),n_distinct(portfolio_factor_data$date),n_distinct(portfolio_all_factor_data$date) ))model_comparison_roadmap |>mutate(across(c(sample_start, sample_end), as.character)) |>kable(caption ="Roadmap for the FF3 benchmark and the comparison models.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Roadmap for the FF3 benchmark and the comparison models.

model

role

factors

sample_start

sample_end

months

FF3

Detailed benchmark

Mkt_RF, SMB3, HML

1927-01-31

2020-12-31

1128

FF3 plus momentum

Fast comparison

Mkt_RF, SMB3, HML, Mom

1927-01-31

2020-12-31

1128

FF5

Fast comparison

Mkt_RF, SMB5, HML, RMW, CMA

1963-07-31

2020-12-31

690

The roadmap prevents repetition. FF3 receives the full mathematical and statistical explanation. The momentum and five-factor rows will be read later as robustness comparisons: the same test assets, a different factor set, and a different sample for FF5 because those factors start later.

4.8 Cross-sectional asset pricing tests

Time-series regressions estimate betas. Cross-sectional regressions ask whether those betas explain average returns across assets. The data shape changes at this point. The regression now has one row for each test portfolio. The dependent variable is the portfolio’s average excess return. The explanatory variables are the betas estimated in the previous time-series step.

The intuition is the same as pricing any characteristic. A beta is a quantity of exposure. A lambda is the price attached to that exposure. The fitted value is the total average excess return assigned by the pricing equation after adding up the priced exposures. For a three-factor model, the fitted value is

This equation should be read portfolio by portfolio. A portfolio with high market beta receives more fitted return when \(\widehat{\lambda}_M\) is positive. A portfolio with high value beta receives more fitted return when \(\widehat{\lambda}_H\) is positive. If a beta is high but its lambda is close to zero, that exposure does little work in the fitted cross-section.

This is the expected-return beta representation emphasized in regression-based asset pricing. Cochrane’s chapter 12 frames this equation as a cross-sectional line fitted through test assets (Cochrane 2005). The betas are the right-hand-side variables, the lambdas are the coefficients of the pricing line, and the residuals are pricing errors. The OLS beta-method chooses the lambdas that minimize the sum of squared pricing errors across the 25 portfolios:

This objective explains the visual role of the fitted-return plot. The 45-degree line represents perfect pricing for every test asset. OLS chooses one common pricing equation that brings the points as close as possible to that line in a least-squares sense.

This is a static two-pass cross-sectional regression. It is related to the Fama-MacBeth logic used in asset pricing (Fama and MacBeth 1973), because both approaches first estimate exposures and then price those exposures in a cross-section. A formal Fama-MacBeth procedure would repeat the cross-sectional regression period by period and estimate inference from the time series of price-of-risk estimates. The chapter uses the simpler static version to keep the bridge between betas, prices of risk, fitted returns, and pricing errors transparent. In this chapter, the cross-section is the set of 25 size-value portfolios.

The equation has a clear economic reading. The left-hand side, \(\bar{R}_i^e\), is the average excess return of portfolio \(i\). The regressors are estimated exposures from the first-pass time-series regressions. The coefficients \(\lambda_M\), \(\lambda_S\), and \(\lambda_H\) are prices of risk in the cross-section. A positive \(\lambda_H\) means that, holding market and size exposure fixed, portfolios with higher value exposure have higher average excess returns in this sample. A low fitted value for a portfolio means that its estimated betas explain less than its observed average return under this second-pass equation.

The units are also important. The response variable is measured as average monthly excess return in percent. Therefore a \(\lambda\) coefficient is the change in average monthly excess return, in percentage points, associated with one additional unit of the corresponding beta, holding the other betas fixed. A positive price of risk rewards exposure to that factor in this cross-section. A negative price of risk penalizes that exposure in this sample. A coefficient near zero says that the estimated beta does little to organize average returns once the other betas are included.

The residual \(\eta_i\) is the cross-sectional pricing error. It is the vertical gap between the portfolio’s observed average excess return and the fitted value assigned by the common pricing equation. This gap is different from the time-series residual \(\varepsilon_{i,t}\): \(\varepsilon_{i,t}\) is a month-level error, while \(\eta_i\) is an average-return error for one portfolio.

Cochrane often writes the cross-sectional residual as an alpha. This chapter uses \(\eta_i\) in the cross-sectional equation to keep two objects separate: \(\alpha_i\) is the time-series intercept for asset \(i\), and \(\eta_i\) is the cross-sectional pricing error after the common lambda estimates are applied. Both objects diagnose model fit, but they come from different regressions.

There are therefore two layers of estimation:

Layer

Object estimated

Data orientation

Economic role

Time-series regression

\(\alpha_i\) and \(\boldsymbol{\beta}_i\) for each asset

One asset across many months

Measures exposure to factors

Cross-sectional regression

\(\lambda\) coefficients

Many assets in one average-return cross-section

Prices those exposures

The first layer asks how each portfolio moves with the factors. The second layer asks whether those exposures explain why some portfolios earn higher average excess returns than others.

The important change is the source of the fitted value. In the time-series figures, each portfolio has its own intercept, so each regression can match its own sample average closely. In the cross-sectional regression, the fitted value comes from one common pricing equation shared by the 25 portfolios. A portfolio receives a high fitted average return only if its estimated exposures combine with the estimated prices of risk to justify that return. This is the economic content of the second pass: betas become explanatory variables for average returns.

broom::glance(cross_section_fit) |>mutate(across(where(is.numeric), ~round(.x, 6))) |>kable(caption ="Goodness-of-fit summary for the beta-method cross-sectional regression.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Goodness-of-fit summary for the beta-method cross-sectional regression.

r.squared

adj.r.squared

sigma

statistic

p.value

df

logLik

AIC

BIC

deviance

df.residual

nobs

0.654312

0.604928

0.12413

13.24945

4.5e-05

3

18.86654

-27.73308

-21.6387

0.323575

21

25

The cross-sectional block should be read as a second pass. The first table is the data matrix: one row per portfolio, average excess return as the outcome, and estimated betas as regressors. The coefficient table estimates the prices attached to those betas. The goodness-of-fit table summarizes how much of the 25-portfolio average-return pattern is captured by this beta-pricing equation. Reading these tables in order prevents a common confusion. The beta table by itself only reports exposures. The coefficient table tells how the cross-section prices those exposures. The fitted-value plot then translates the estimated pricing equation back into portfolio-level average returns.

The coefficient table should be read in three passes. First, inspect the sign of each \(\lambda\): it tells whether the exposure is rewarded or penalized in this sample. Second, inspect the magnitude: it tells how much the fitted average return changes when the beta changes by one unit. Third, inspect the standard errors and p-values with caution: the betas were estimated in a first pass, so the usual OLS table is an orientation device for inference. This is why the chapter later separates estimation logic from formal inference limits.

In this sample, the beta-method gives a concrete result. The cross-sectional \(R^2\) is 0.65, so the estimated betas capture a substantial part of the 25-portfolio average-return pattern while leaving visible pricing errors. The estimated market price of risk is -0.92 monthly percentage points, the size price is 0.13, and the value price is 0.34. The signs say that, conditional on the other estimated betas, size and value exposure raise fitted average excess returns in this cross-section, while market beta lowers the fitted average return over this sample. The positive value coefficient is especially important for the narrative because the size-value portfolios were built precisely to make value-related return patterns visible.

Figure 4.29: Cross-sectional fitted returns using estimated betas.

The fitted-return figure is the visual version of the second-pass regression. Each label is one portfolio. Points close to the 45-degree line are portfolios whose average returns are close to what the estimated beta prices predict. Points above the line have observed average returns larger than the fitted value; points below the line have observed average returns smaller than the fitted value.

Code

cross_section_aug |>select(symbol, ERe_percent, fitted_return_percent = .fitted) |>arrange(symbol) |>mutate(across(where(is.numeric), ~round(.x, 4))) |>kable(caption ="Observed and fitted average excess returns from the beta method.",row.names =FALSE ) |>kable_styling(latex_options ="HOLD_position")

Observed and fitted average excess returns from the beta method.

symbol

ERe_percent

fitted_return_percent

BIG HiBM

0.9289

0.9012

BIG LoBM

0.6733

0.6102

ME1 BM2

0.7150

0.9455

ME1 BM3

1.0120

1.0306

ME1 BM4

1.1674

1.1483

ME2 BM1

0.6830

0.7269

ME2 BM2

0.9597

0.8947

ME2 BM3

0.9735

0.9821

ME2 BM4

1.0482

1.0778

ME2 BM5

1.2414

1.0959

ME3 BM1

0.7691

0.6497

ME3 BM2

0.9239

0.8102

ME3 BM3

0.9351

0.9196

ME3 BM4

1.0079

1.0000

ME3 BM5

1.1023

1.0002

ME4 BM1

0.7602

0.5946

ME4 BM2

0.7856

0.7794

ME4 BM3

0.8506

0.8721

ME4 BM4

0.9506

0.9332

ME4 BM5

1.0322

0.9223

ME5 BM2

0.6291

0.7415

ME5 BM3

0.7176

0.8520

ME5 BM4

0.6341

0.9060

SMALL HiBM

1.3264

1.2245

SMALL LoBM

0.6080

0.8166

The fitted-value table gives the same comparison portfolio by portfolio. It is useful when labels overlap in the figure or when the reader wants to inspect a particular size-value cell directly.

The coefficients \(\lambda_M\), \(\lambda_S\), and \(\lambda_H\) are estimated prices of risk. A positive \(\lambda_H\), for example, means that portfolios with higher value exposure have higher average excess returns in this cross-section, conditional on the other beta estimates.

The fitted-return graph and fitted-value table should be read together. The graph shows the overall geometry: points close to the 45-degree line are well-explained by the beta-pricing equation. The table makes the individual portfolio comparison auditable. Large vertical gaps indicate portfolios whose average returns remain far from the fitted values implied by the estimated prices of market, size, and value exposure.

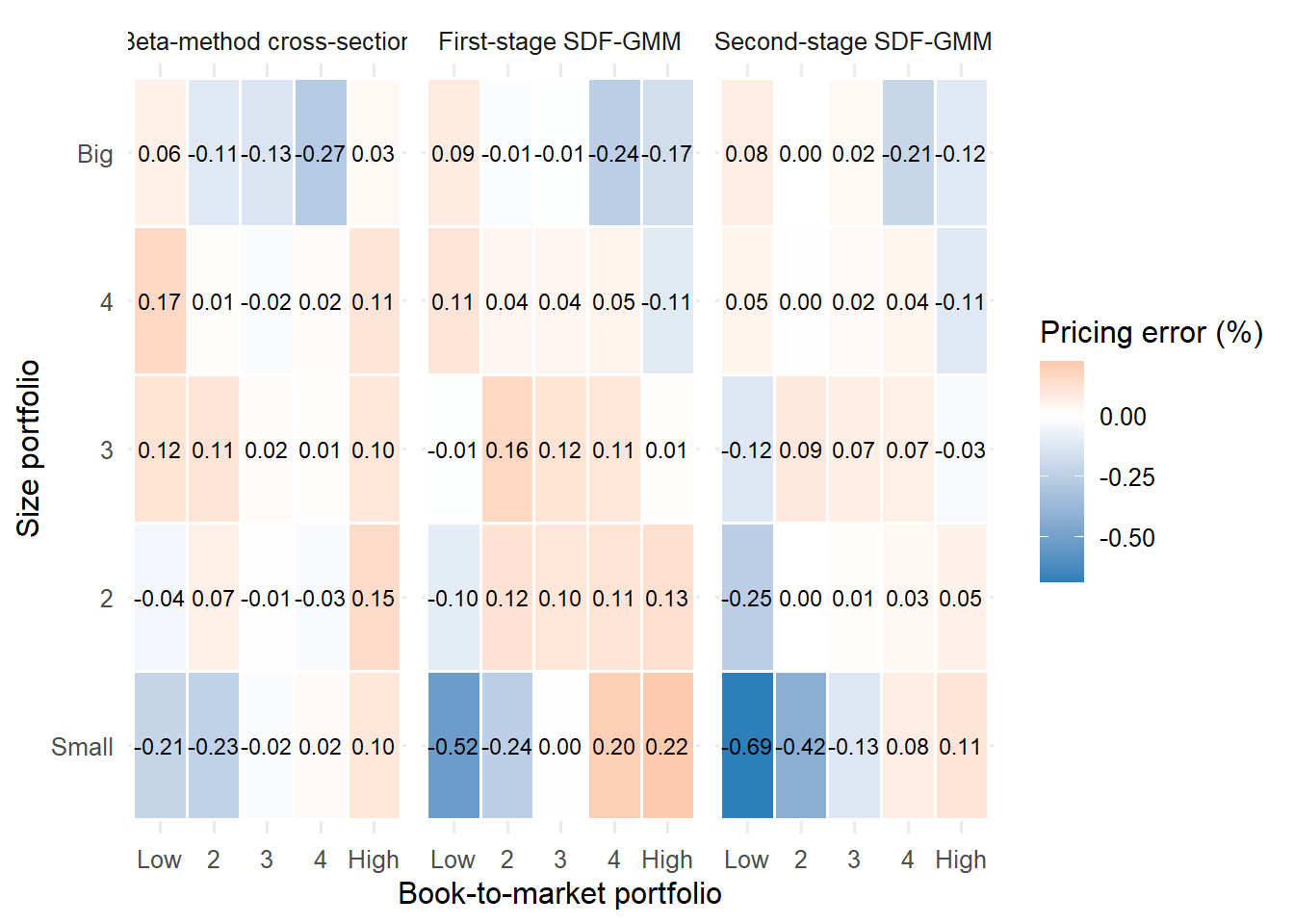

The reason for doing this second pass is conceptual. A time-series regression gives each portfolio’s market beta, size beta, and value beta. The next question is whether those betas carry enough information to account for the portfolio’s average return. The second pass asks that question directly. It treats the estimated betas as the characteristics to be priced and asks whether a common set of lambdas can assign reasonable average returns to all 25 portfolios at once.

The equation also clarifies the division of responsibility between data, estimation, and interpretation:

This table is also a guide to the code. cross_section_data contains the first two rows of the table: average excess returns and estimated betas. cross_section_fit estimates the lambdas. cross_section_aug adds fitted values and pricing errors. The code therefore follows the same sequence as the econometric argument: construct the cross-section, estimate prices of risk, then inspect the errors.

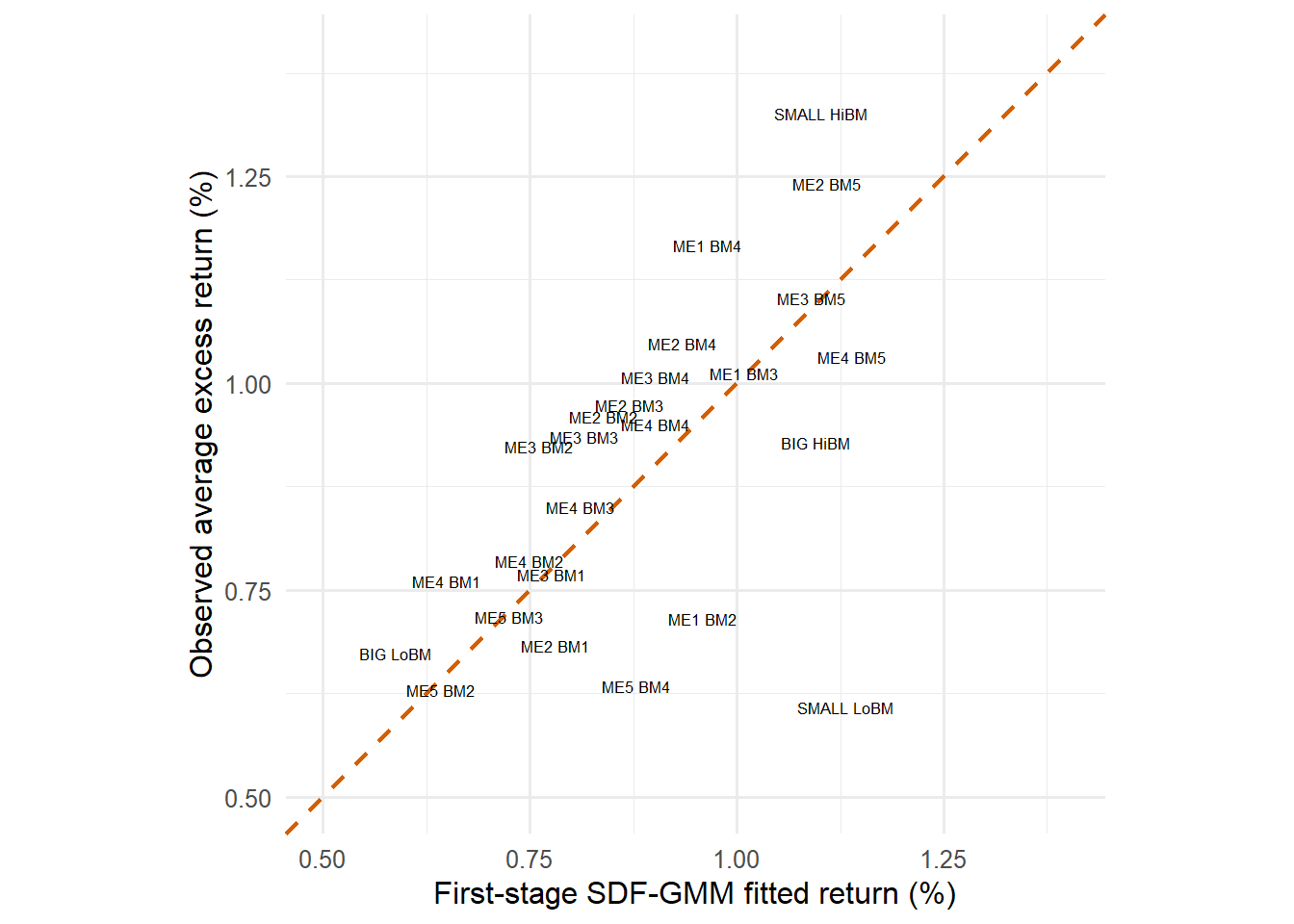

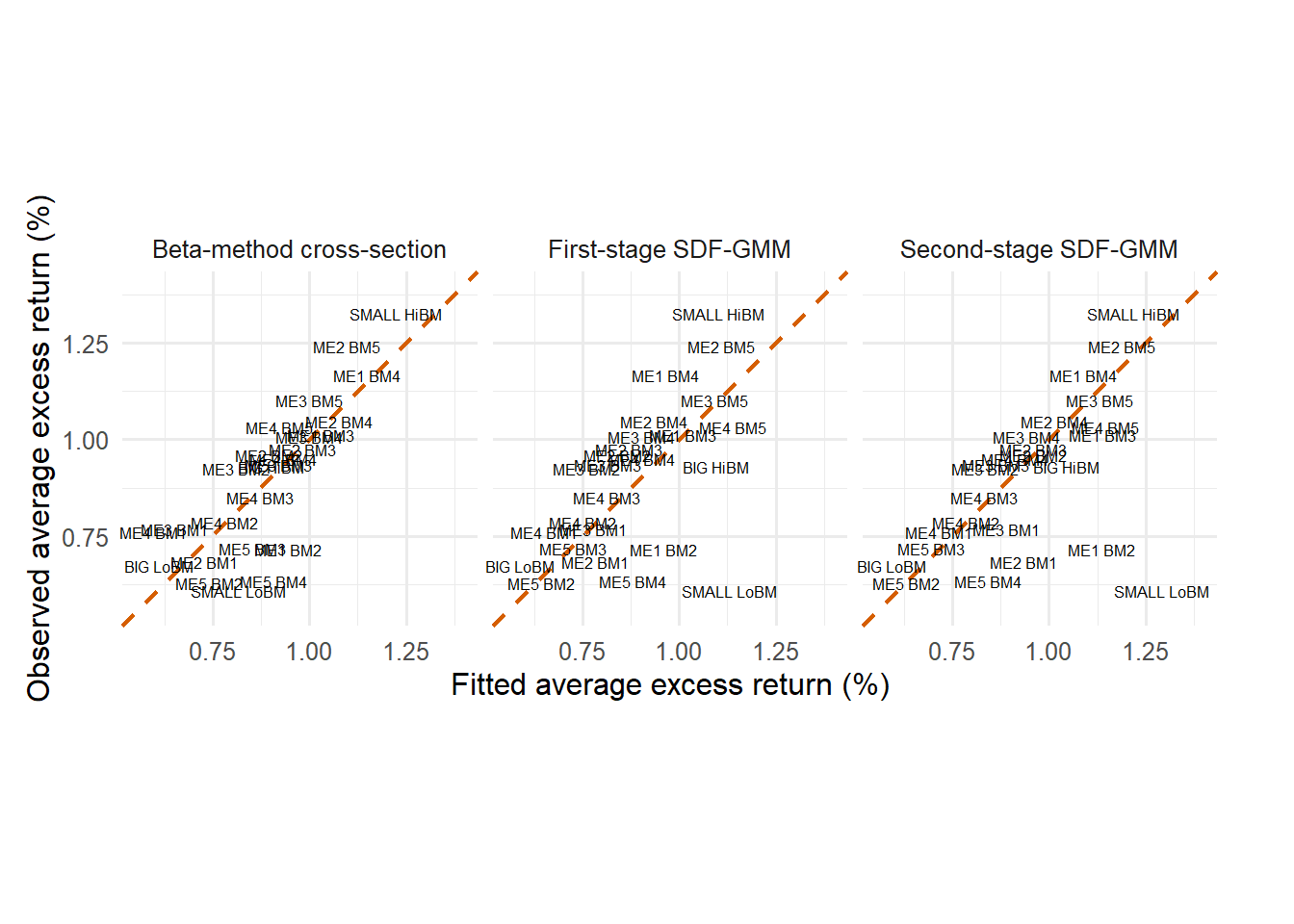

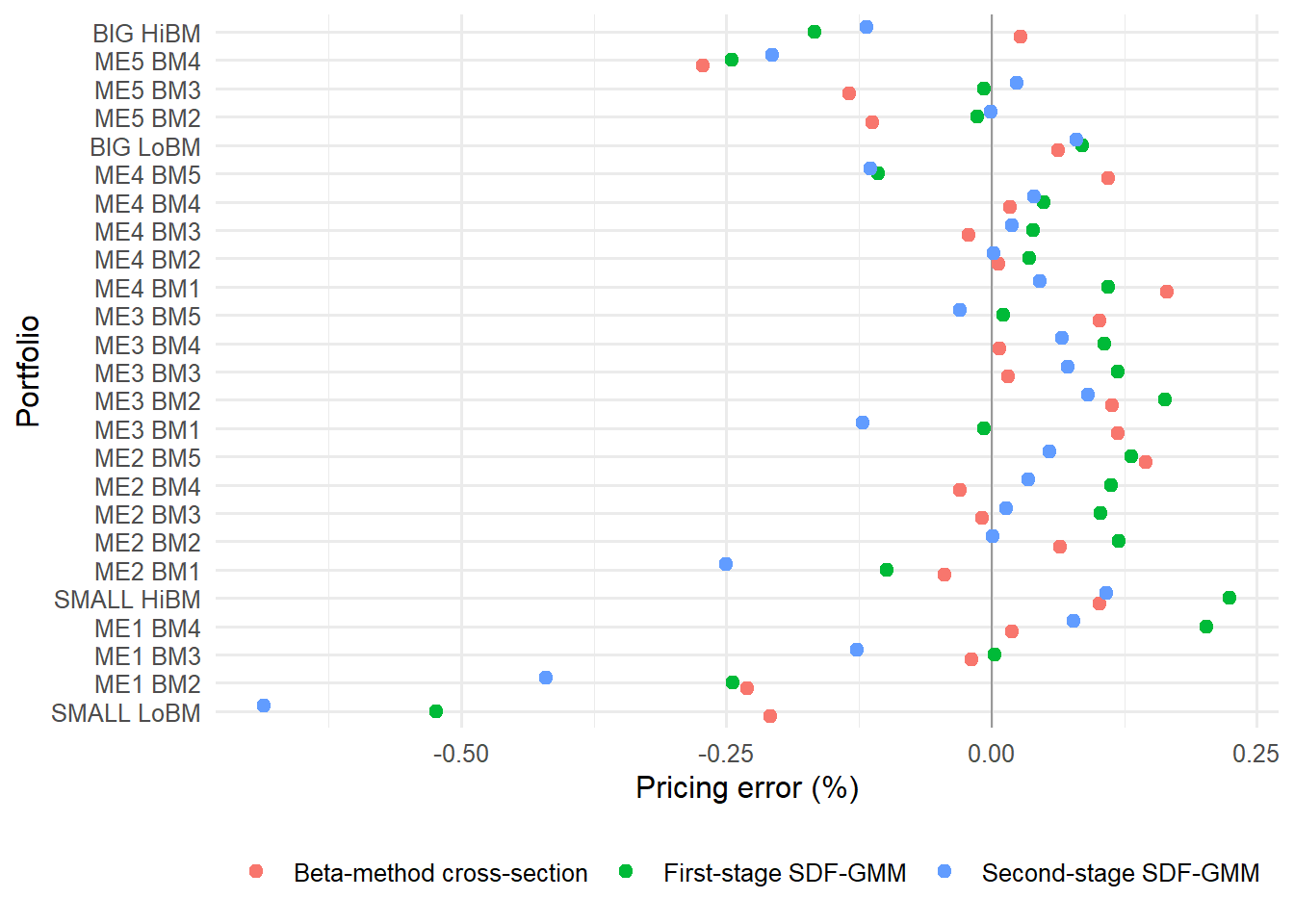

4.9 SDF-GMM and pricing logic

The beta-method prices exposures. The SDF-GMM method prices payoffs through moments. Both approaches ask whether the factor model can explain average excess returns, but they organize the evidence differently. The beta-method starts with estimated betas. SDF-GMM starts with a pricing condition and turns that condition into sample moments.

The purpose of this section is to make Cochrane’s chapter 13 operational. The logic is:

Step

Question

Object

Pricing condition

What should be true if the model prices excess returns?

\(E(m_tR_{i,t}^e)=0\)

Linear SDF

How does the discount factor depend on factors?

\(m_t=1-\mathbf{b}^{\top}\mathbf{f}_t\)

Sample moments

What does the model leave unexplained in the data?

What SDF loadings minimize unweighted pricing errors?

\(W=I\)

Second-stage GMM

What changes when errors are weighted by their covariance?

\(W=\widehat{\mathbf{S}}^{-1}\)

J-test

Are the remaining pricing errors jointly large?

\(J=T\mathbf{g}'W\mathbf{g}\)

This sequence answers a question beyond the regression table: after choosing the SDF loadings, are the leftover pricing errors small enough to be consistent with the model?

The stochastic discount factor view starts from the pricing condition

\[

E(m_t R_{i,t}^e)=0.

\]

This notation is standard in modern asset pricing (Cochrane 2005). The object \(m_t\) is a stochastic discount factor. It assigns value today to future payoffs. For an excess return, the initial cost is zero after financing at the risk-free rate. The model therefore asks for the discounted excess return to average to zero. The equation says that, after the model applies its discount factor, each test asset should have zero remaining average payoff.

Read the equation literally from inside to outside. Start with the excess return of asset \(i\) in month \(t\), \(R_{i,t}^e\). Multiply that payoff by the discount factor in the same month, \(m_t\). Then take the average implied by \(E(\cdot)\). If the model prices the asset, that average is zero because an excess return has zero initial cost. In the data, the sample version of this average is the pricing error. A model with small pricing errors is a model whose discount factor makes the test assets close to zero-cost payoffs in present-value terms.

The equation can be read in three layers. First, \(R_{i,t}^e\) is the payoff to be priced. Second, \(m_t\) is the risk adjustment applied to that payoff. Third, the expectation averages the risk-adjusted payoff over time or across states. If the model is correct, positive and negative risk-adjusted payoffs balance out for every test asset. The empirical version checks whether that balance is close enough in the sample.

The condition is easier to read through states of the world. If \(m_t\) is high in bad states, then payoffs received in those states are especially valuable. An asset that performs poorly when \(m_t\) is high must compensate investors with a higher average excess return. This is the same economic idea behind factor betas, written in pricing-condition form.

The condition also explains why covariance is central. The expectation \(E(m_tR_{i,t}^e)\) is an average product. It is affected by the average excess return of the asset and by the way that return co-moves with the discount factor. A high average excess return can be consistent with the model when the asset pays off in states where the discount factor is low. The asset is then less valuable as insurance, so investors require compensation through a higher average return.

A linear SDF can be normalized as

\[

m_t

=

1

-

\mathbf{b}^{\top}\mathbf{f}_t.

\]

This is the normalization used for the GMM calculation below. The constant is fixed at one, and the vector \(\mathbf{b}\) controls how strongly each factor enters the discount factor. If a factor captures bad times for investors, assets that pay poorly when that factor is adverse should require higher average excess returns. The SDF formulation and the beta-pricing formulation organize the same economic idea: systematic covariance with factors drives average returns.